Object that gets notified when a given observable changes. More...

#include <observable.hpp>

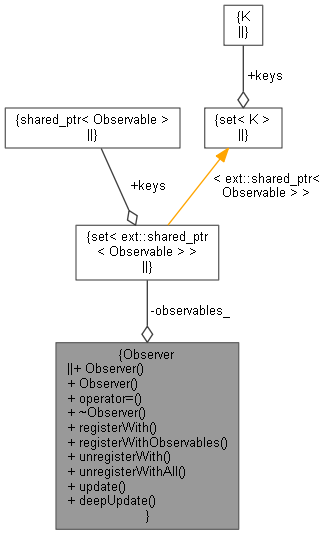

Inheritance diagram for Observer:

Inheritance diagram for Observer: Collaboration diagram for Observer:

Collaboration diagram for Observer:

Public Types | |

| typedef set_type::iterator | iterator |

Public Member Functions | |

| Observer ()=default | |

| Observer (const Observer &) | |

| Observer & | operator= (const Observer &) |

| virtual | ~Observer () |

| std::pair< iterator, bool > | registerWith (const ext::shared_ptr< Observable > &) |

| void | registerWithObservables (const ext::shared_ptr< Observer > &) |

| Size | unregisterWith (const ext::shared_ptr< Observable > &) |

| void | unregisterWithAll () |

| virtual void | update ()=0 |

| virtual void | deepUpdate () |

Private Types | |

| typedef std::set< ext::shared_ptr< Observable > > | set_type |

Private Attributes | |

| set_type | observables_ |

Detailed Description

Object that gets notified when a given observable changes.

Definition at line 116 of file observable.hpp.

Member Typedef Documentation

◆ set_type

|

private |

Definition at line 118 of file observable.hpp.

◆ iterator

| typedef set_type::iterator iterator |

Definition at line 120 of file observable.hpp.

Constructor & Destructor Documentation

◆ Observer() [1/2]

|

default |

◆ Observer() [2/2]

Definition at line 205 of file observable.hpp.

◆ ~Observer()

|

virtual |

Definition at line 220 of file observable.hpp.

Member Function Documentation

◆ operator=()

Definition at line 211 of file observable.hpp.

◆ registerWith()

| std::pair< Observer::iterator, bool > registerWith | ( | const ext::shared_ptr< Observable > & | h | ) |

◆ registerWithObservables()

| void registerWithObservables | ( | const ext::shared_ptr< Observer > & | o | ) |

register with all observables of a given observer. Note that this does not include registering with the observer itself.

Definition at line 235 of file observable.hpp.

Here is the call graph for this function: Here is the caller graph for this function:

Here is the caller graph for this function:

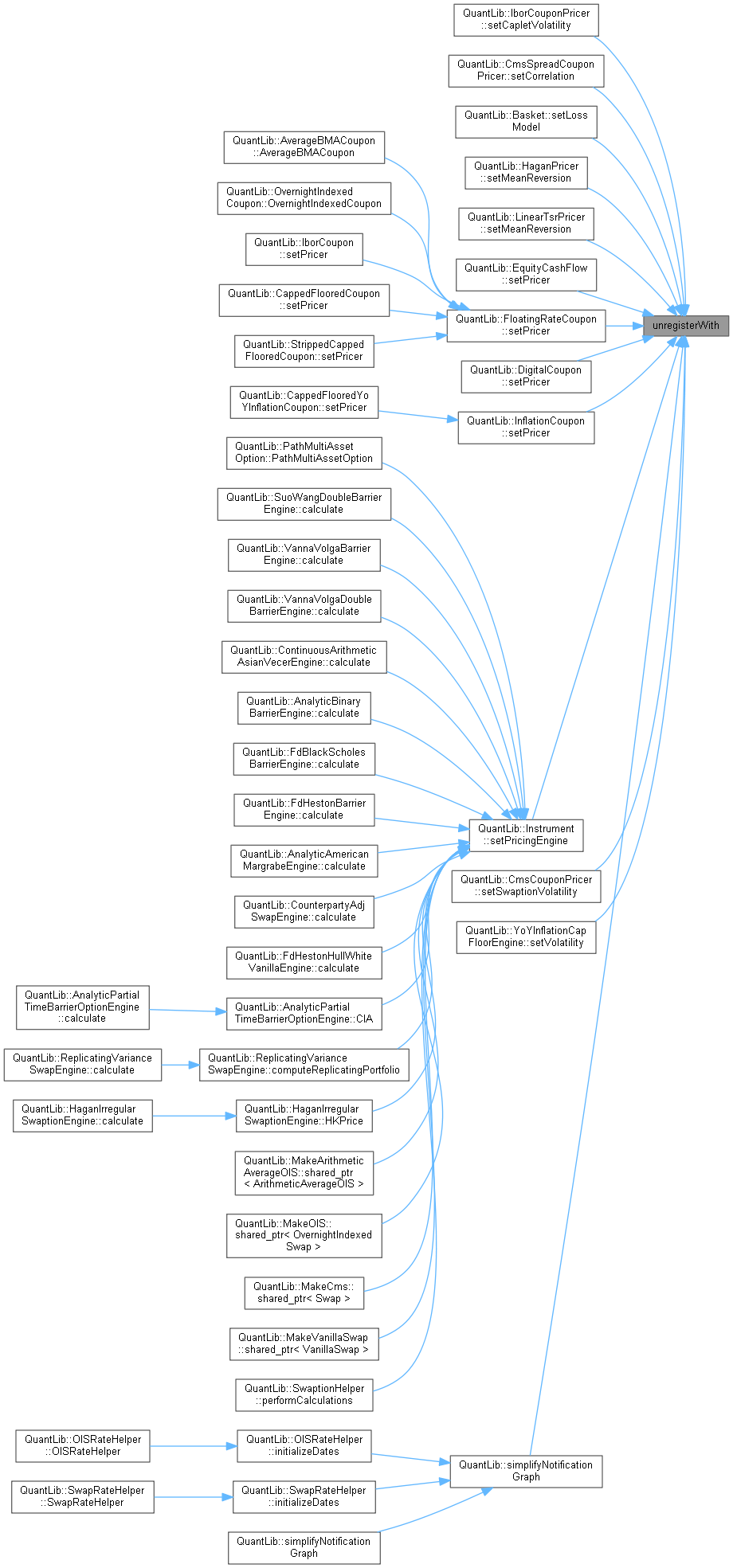

◆ unregisterWith()

| Size unregisterWith | ( | const ext::shared_ptr< Observable > & | h | ) |

◆ unregisterWithAll()

| void unregisterWithAll | ( | ) |

Definition at line 249 of file observable.hpp.

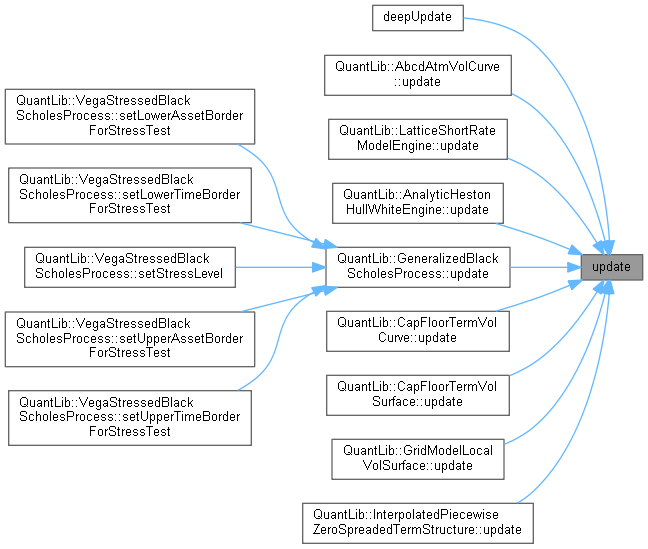

◆ update()

|

pure virtual |

This method must be implemented in derived classes. An instance of Observer does not call this method directly: instead, it will be called by the observables the instance registered with when they need to notify any changes.

Implemented in CappedFlooredYoYInflationCoupon, FloatingRateCouponPricer, EquityCashFlowPricer, InflationCouponPricer, CommodityIndex, BaseCorrelationLossModel< BaseModel_T, Corr2DInt_T >, BaseCorrelationTermStructure< Interpolator2D_T >, Basket, DefaultLatentModel< copulaPolicy >, GaussianLHPLossModel, RandomLM< derivedRandomLM, copulaPolicy, USNG >, RandomLM< RandomDefaultLM, copulaPolicy, SobolRsg >, RandomLM< RandomLossLM, copulaPolicy, SobolRsg >, RandomDefaultModel, ConstantRecoveryModel, AssetSwapHelper, DeltaVolQuote, PiecewiseYoYOptionletVolatilityCurve< Interpolator, Bootstrap, Traits >, InterpolatedYoYCapFloorTermPriceSurface< Interpolator2D, Interpolator1D >, LatentModel< copulaPolicyImpl >, LatentModel< copulaPolicy >, LatentModel< GaussianCopulaPolicy >, AbcdAtmVolCurve, ExtendedBlackVarianceCurve, ExtendedBlackVarianceSurface, NoArbSabrInterpolatedSmileSection, SabrVolSurface, SviInterpolatedSmileSection, ZabrInterpolatedSmileSection< Evaluation >, Handle< T >::Link, Index, RendistatoBasket, Claim, CotSwapToFwdAdapterFactory, FlatVolFactory, FwdToCotSwapAdapterFactory, CalibratedModel, Gsr, Gsr::VolatilityObserver, Gsr::ReversionObserver, MarkovFunctional, LazyObject, GenericEngine< ArgumentsType, ResultsType >, GenericEngine< VanillaOption::arguments, VanillaOption::results >, GenericEngine< CapFloor::arguments, CapFloor::results >, GenericEngine< ForwardOptionArguments< VanillaOption::arguments >, VanillaOption::results >, GenericEngine< BarrierOption::arguments, BarrierOption::results >, GenericEngine< BasketOption::arguments, BasketOption::results >, GenericEngine< Bond::arguments, Bond::results >, GenericEngine< CPICapFloor::arguments, CPICapFloor::results >, GenericEngine< CPISwap::arguments, CPISwap::results >, GenericEngine< CallableBond::arguments, CallableBond::results >, GenericEngine< CatBond::arguments, CatBond::results >, GenericEngine< CdsOption::arguments, CdsOption::results >, GenericEngine< CliquetOption::arguments, CliquetOption::results >, GenericEngine< ComplexChooserOption::arguments, ComplexChooserOption::results >, GenericEngine< CompoundOption::arguments, CompoundOption::results >, GenericEngine< ContinuousAveragingAsianOption::arguments, ContinuousAveragingAsianOption::results >, GenericEngine< ContinuousFixedLookbackOption::arguments, ContinuousFixedLookbackOption::results >, GenericEngine< ContinuousFloatingLookbackOption::arguments, ContinuousFloatingLookbackOption::results >, GenericEngine< ContinuousPartialFixedLookbackOption::arguments, ContinuousPartialFixedLookbackOption::results >, GenericEngine< ContinuousPartialFloatingLookbackOption::arguments, ContinuousPartialFloatingLookbackOption::results >, GenericEngine< ConvertibleBond::arguments, ConvertibleBond::results >, GenericEngine< CreditDefaultSwap::arguments, CreditDefaultSwap::results >, GenericEngine< DiscreteAveragingAsianOption::arguments, DiscreteAveragingAsianOption::results >, GenericEngine< DoubleBarrierOption::arguments, DoubleBarrierOption::results >, GenericEngine< VanillaVPPOption::arguments, VanillaVPPOption::results >, GenericEngine< EnergyCommodity::arguments, EnergyCommodity::results >, GenericEngine< EverestOption::arguments, EverestOption::results >, GenericEngine< Swaption::arguments, Swaption::results >, GenericEngine< VanillaSwingOption::arguments, VanillaSwingOption::results >, GenericEngine< VanillaStorageOption::arguments, VanillaStorageOption::results >, GenericEngine< FixedVsFloatingSwap::arguments, FixedVsFloatingSwap::results >, GenericEngine< FloatFloatSwap::arguments, FloatFloatSwap::results >, GenericEngine< FloatFloatSwaption::arguments, FloatFloatSwaption::results >, GenericEngine< NonstandardSwaption::arguments, NonstandardSwaption::results >, GenericEngine< IrregularSwaption::arguments, IrregularSwaption::results >, GenericEngine< HimalayaOption::arguments, HimalayaOption::results >, GenericEngine< HolderExtensibleOption::arguments, HolderExtensibleOption::results >, GenericEngine< IrregularSwap::arguments, IrregularSwap::results >, GenericEngine< Arguments, Results >, GenericEngine< MargrabeOption::arguments, MargrabeOption::results >, GenericEngine< MultiAssetOption::arguments, MultiAssetOption::results >, GenericEngine< NonstandardSwap::arguments, NonstandardSwap::results >, GenericEngine< NthToDefault::arguments, NthToDefault::results >, GenericEngine< OneAssetOption::arguments, OneAssetOption::results >, GenericEngine< PagodaOption::arguments, PagodaOption::results >, GenericEngine< PartialTimeBarrierOption::arguments, PartialTimeBarrierOption::results >, GenericEngine< PathMultiAssetOption::arguments, PathMultiAssetOption::results >, GenericEngine< Instr::arguments, QuantoOptionResults< Instr::results > >, GenericEngine< SimpleChooserOption::arguments, SimpleChooserOption::results >, GenericEngine< SpreadOption::arguments, SpreadOption::results >, GenericEngine< Swap::arguments, Swap::results >, GenericEngine< SyntheticCDO::arguments, SyntheticCDO::results >, GenericEngine< VanillaSwap::arguments, VanillaSwap::results >, GenericEngine< TwoAssetBarrierOption::arguments, TwoAssetBarrierOption::results >, GenericEngine< TwoAssetCorrelationOption::arguments, TwoAssetCorrelationOption::results >, GenericEngine< VarianceOption::arguments, VarianceOption::results >, GenericEngine< VarianceSwap::arguments, VarianceSwap::results >, GenericEngine< WriterExtensibleOption::arguments, WriterExtensibleOption::results >, GenericEngine< YearOnYearInflationSwap::arguments, YearOnYearInflationSwap::results >, GenericEngine< YoYInflationCapFloor::arguments, YoYInflationCapFloor::results >, GenericEngine< ZeroCouponInflationSwap::arguments, ZeroCouponInflationSwap::results >, LatticeShortRateModelEngine< Arguments, Results >, LatticeShortRateModelEngine< CallableBond::arguments, CallableBond::results >, LatticeShortRateModelEngine< CapFloor::arguments, CapFloor::results >, LatticeShortRateModelEngine< Swaption::arguments, Swaption::results >, LatticeShortRateModelEngine< VanillaSwap::arguments, VanillaSwap::results >, AnalyticHestonHullWhiteEngine, COSHestonEngine, FdHestonHullWhiteVanillaEngine, FdHestonVanillaEngine, GeneralizedBlackScholesProcess, HestonSLVProcess, HybridHestonHullWhiteProcess, JointStochasticProcess, CompositeQuote< BinaryFunction >, DerivedQuote< UnaryFunction >, ForwardSwapQuote, ForwardValueQuote, FuturesConvAdjustmentQuote, LastFixingQuote, StochasticProcess, TermStructure, BootstrapHelper< TS >, BootstrapHelper< YoYInflationTermStructure >, BootstrapHelper< YoYOptionletVolatilitySurface >, BootstrapHelper< ZeroInflationTermStructure >, RelativeDateBootstrapHelper< TS >, CdsHelper, PiecewiseDefaultCurve< Traits, Interpolator, Bootstrap >, DefaultProbabilityTermStructure, PiecewiseYoYInflationCurve< Interpolator, Bootstrap, Traits >, PiecewiseZeroInflationCurve< Interpolator, Bootstrap, Traits >, CapFloorTermVolCurve, CapFloorTermVolSurface, GridModelLocalVolSurface, InterpolatedSmileSection< Interpolator >, StrippedOptionletAdapter, SabrInterpolatedSmileSection, SmileSection, SpreadedSmileSection, CmsMarket, XabrSwaptionVolatilityCube< Model >::PrivateObserver, SwaptionVolatilityDiscrete, CompositeZeroYieldStructure< BinaryFunction >, FittedBondDiscountCurve, FlatForward, ForwardSpreadedTermStructure, InterpolatedPiecewiseForwardSpreadedTermStructure< Interpolator >, PiecewiseYieldCurve< Traits, Interpolator, Bootstrap >, InterpolatedPiecewiseZeroSpreadedTermStructure< Interpolator >, UltimateForwardTermStructure, ZeroSpreadedTermStructure, and YieldTermStructure.

Here is the caller graph for this function:

◆ deepUpdate()

|

virtual |

This method allows to explicitly update the instance itself and nested observers. If notifications are disabled a call to this method ensures an update of such nested observers. It should be implemented in derived classes whenever applicable

Reimplemented in CappedFlooredCoupon, DigitalCoupon, StrippedCappedFlooredCoupon, Bond, CapFloor, CompositeInstrument, Swap, Swaption, and StrippedOptionletAdapter.

Definition at line 255 of file observable.hpp.

Here is the call graph for this function:

Member Data Documentation

◆ observables_

|

private |

Definition at line 155 of file observable.hpp.