#include <randomdefaultlatentmodel.hpp>

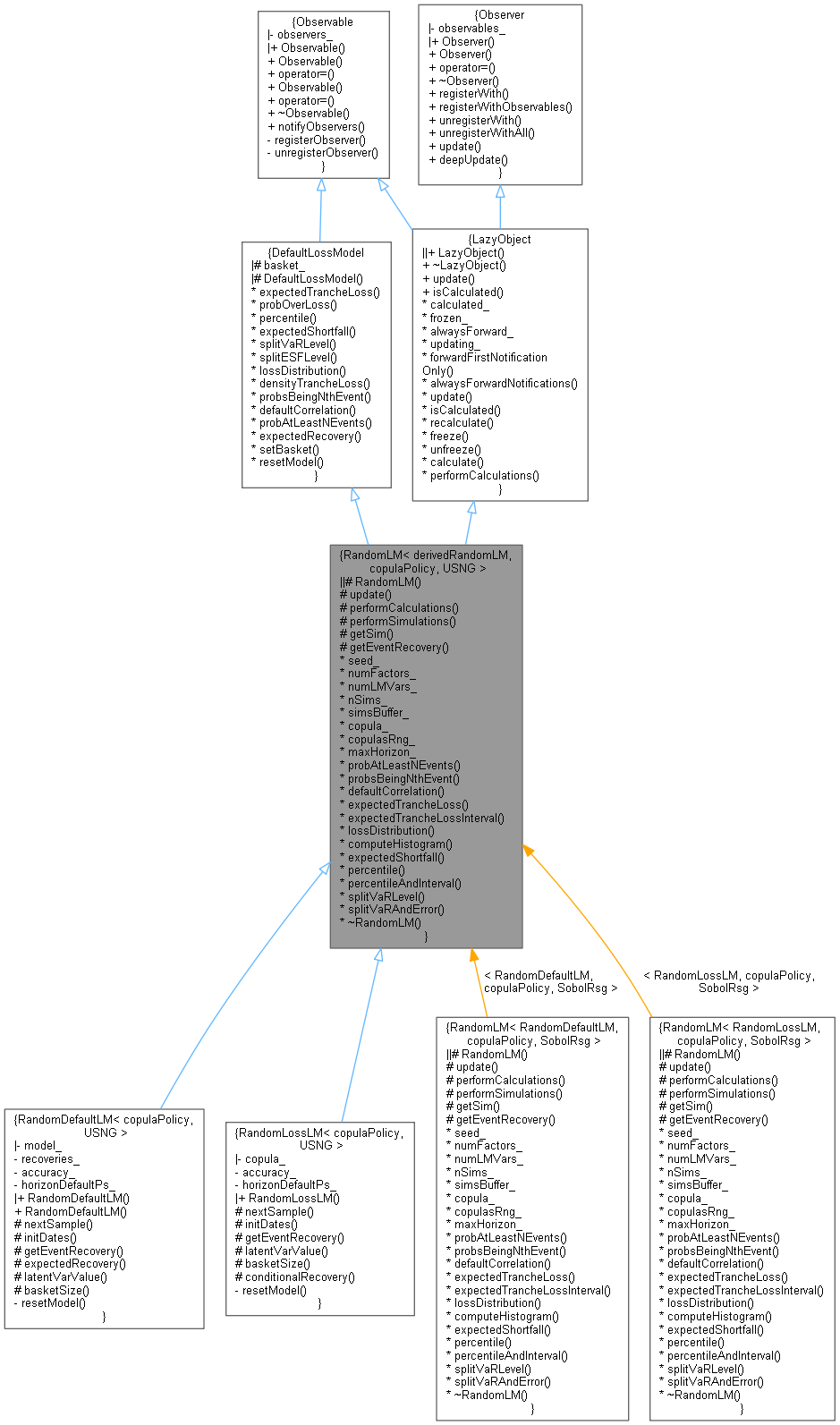

Inheritance diagram for RandomLM< derivedRandomLM, copulaPolicy, USNG >:

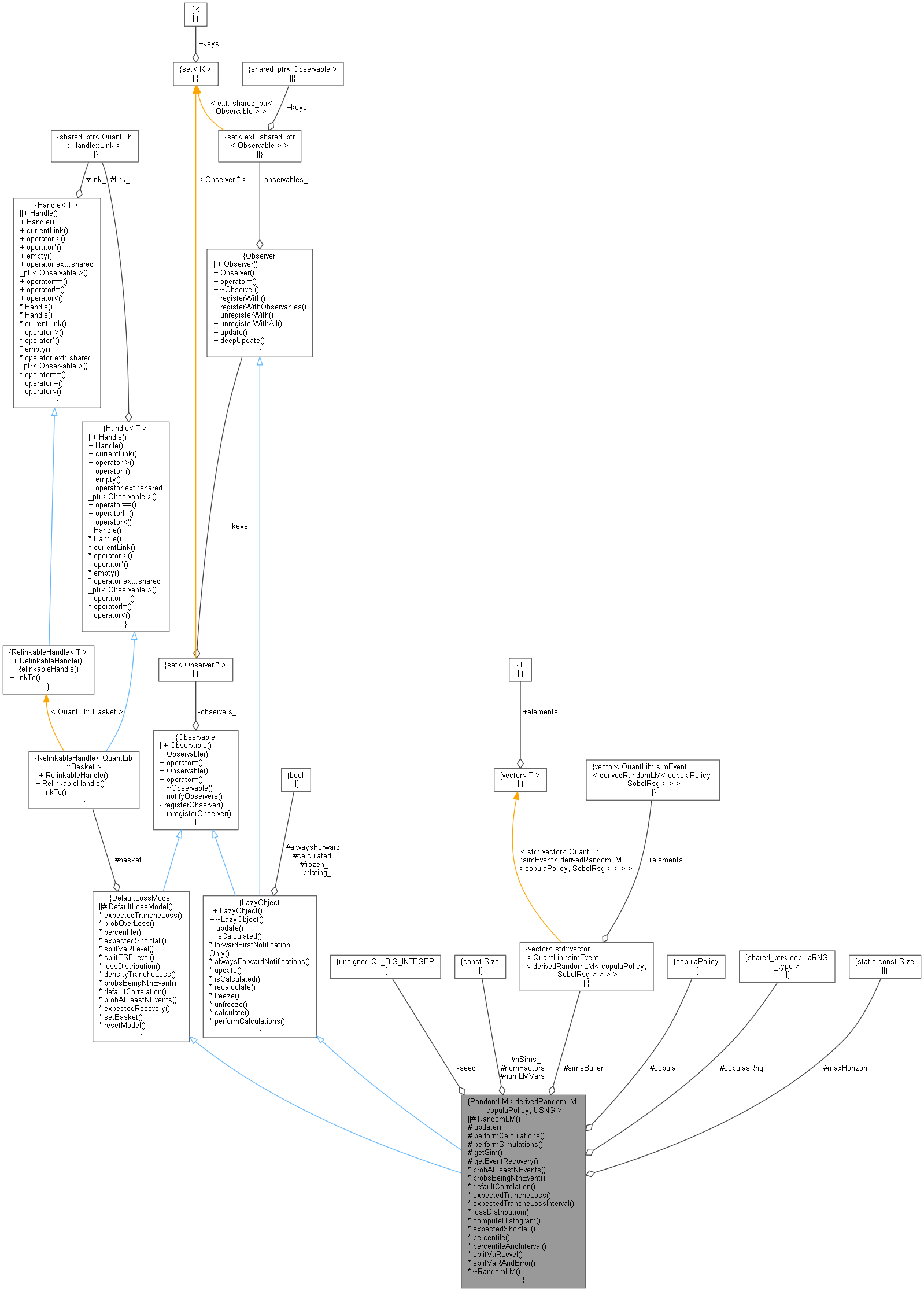

Inheritance diagram for RandomLM< derivedRandomLM, copulaPolicy, USNG >: Collaboration diagram for RandomLM< derivedRandomLM, copulaPolicy, USNG >:

Collaboration diagram for RandomLM< derivedRandomLM, copulaPolicy, USNG >:

Protected Member Functions | |

| RandomLM (Size numFactors, Size numLMVars, copulaPolicy copula, Size nSims, BigNatural seed) | |

| void | update () override |

| void | performCalculations () const override |

| void | performSimulations () const |

| const std::vector< simEvent< derivedRandomLM< copulaPolicy, USNG > > > & | getSim (const Size iSim) const |

| Real | getEventRecovery (const simEvent< derivedRandomLM< copulaPolicy, USNG > > &evt) const |

| Protected Member Functions inherited from LazyObject | |

| virtual void | calculate () const |

| Protected Member Functions inherited from DefaultLossModel | |

| DefaultLossModel ()=default | |

| virtual Probability | probOverLoss (const Date &d, Real lossFraction) const |

| virtual std::vector< Real > | splitESFLevel (const Date &d, Real loss) const |

| Associated ESF fraction to each counterparty. More... | |

| virtual Real | densityTrancheLoss (const Date &d, Real lossFraction) const |

| Probability density of a given loss fraction of the basket notional. More... | |

| virtual Real | expectedRecovery (const Date &, Size iName, const DefaultProbKey &) const |

Private Types | |

| typedef LatentModel< copulaPolicy >::template FactorSampler< USNG > | copulaRNG_type |

Statistics, DefaultLossModel interface. | |

| BigNatural | seed_ |

| const Size | numFactors_ |

| const Size | numLMVars_ |

| const Size | nSims_ |

| std::vector< std::vector< simEvent< derivedRandomLM< copulaPolicy, USNG > > > > | simsBuffer_ |

| copulaPolicy | copula_ |

| ext::shared_ptr< copulaRNG_type > | copulasRng_ |

| static const Size | maxHorizon_ = 4050 |

| Probability | probAtLeastNEvents (Size n, const Date &d) const override |

| std::vector< Probability > | probsBeingNthEvent (Size n, const Date &d) const override |

| Real | defaultCorrelation (const Date &d, Size iName, Size jName) const override |

| Pearsons' default probability correlation. More... | |

| Real | expectedTrancheLoss (const Date &d) const override |

| virtual std::pair< Real, Real > | expectedTrancheLossInterval (const Date &d, Probability confidencePerc) const |

| std::map< Real, Probability > | lossDistribution (const Date &d) const override |

| Full loss distribution. More... | |

| virtual Histogram | computeHistogram (const Date &d) const |

| Real | expectedShortfall (const Date &d, Real percent) const override |

| Expected shortfall given a default loss percentile. More... | |

| Real | percentile (const Date &d, Real percentile) const override |

| Value at Risk given a default loss percentile. More... | |

| virtual std::tuple< Real, Real, Real > | percentileAndInterval (const Date &d, Real percentile) const |

| std::vector< Real > | splitVaRLevel (const Date &date, Real loss) const override |

| virtual std::vector< std::vector< Real > > | splitVaRAndError (const Date &date, Real loss, Probability confInterval) const |

| ~RandomLM () override=default | |

Additional Inherited Members | |

| Public Types inherited from Observer | |

| typedef set_type::iterator | iterator |

| Public Member Functions inherited from LazyObject | |

| LazyObject () | |

| ~LazyObject () override=default | |

| void | update () override |

| bool | isCalculated () const |

| void | forwardFirstNotificationOnly () |

| void | alwaysForwardNotifications () |

| void | recalculate () |

| void | freeze () |

| void | unfreeze () |

| Public Member Functions inherited from Observable | |

| Observable ()=default | |

| Observable (const Observable &) | |

| Observable & | operator= (const Observable &) |

| Observable (Observable &&)=delete | |

| Observable & | operator= (Observable &&)=delete |

| virtual | ~Observable ()=default |

| void | notifyObservers () |

| Public Member Functions inherited from Observer | |

| Observer ()=default | |

| Observer (const Observer &) | |

| Observer & | operator= (const Observer &) |

| virtual | ~Observer () |

| std::pair< iterator, bool > | registerWith (const ext::shared_ptr< Observable > &) |

| void | registerWithObservables (const ext::shared_ptr< Observer > &) |

| Size | unregisterWith (const ext::shared_ptr< Observable > &) |

| void | unregisterWithAll () |

| virtual void | update ()=0 |

| virtual void | deepUpdate () |

| Protected Attributes inherited from LazyObject | |

| bool | calculated_ = false |

| bool | frozen_ = false |

| bool | alwaysForward_ |

| Protected Attributes inherited from DefaultLossModel | |

| RelinkableHandle< Basket > | basket_ |

Detailed Description

class QuantLib::RandomLM< derivedRandomLM, copulaPolicy, USNG >

Base class for latent model monte carlo simulation. Independent of the copula type and the generator. Generates the factors and variable samples and determines event threshold but it is not responsible for actual event specification; thats the derived classes responsibility according to what they model. Derived classes need mainly to implement nextSample (Worker::nextSample in the multithreaded version) to compute the simulation event generated, if any, from the latent variables sample. They also have the accompanying event trait to specify.

Definition at line 96 of file randomdefaultlatentmodel.hpp.

Member Typedef Documentation

◆ copulaRNG_type

|

private |

Definition at line 102 of file randomdefaultlatentmodel.hpp.

Constructor & Destructor Documentation

◆ RandomLM()

|

protected |

Definition at line 104 of file randomdefaultlatentmodel.hpp.

◆ ~RandomLM()

|

overridedefault |

Member Function Documentation

◆ update()

|

overrideprotectedvirtual |

This method must be implemented in derived classes. An instance of Observer does not call this method directly: instead, it will be called by the observables the instance registered with when they need to notify any changes.

Implements Observer.

Definition at line 108 of file randomdefaultlatentmodel.hpp.

Here is the call graph for this function:

◆ performCalculations()

|

overrideprotectedvirtual |

This method must implement any calculations which must be (re)done in order to calculate the desired results.

Implements LazyObject.

Definition at line 116 of file randomdefaultlatentmodel.hpp.

Here is the call graph for this function:

◆ performSimulations()

|

protected |

Definition at line 123 of file randomdefaultlatentmodel.hpp.

Here is the caller graph for this function:

◆ getSim()

|

protected |

Definition at line 141 of file randomdefaultlatentmodel.hpp.

◆ getEventRecovery()

|

protected |

Definition at line 145 of file randomdefaultlatentmodel.hpp.

Here is the call graph for this function: Here is the caller graph for this function:

Here is the caller graph for this function:

◆ probAtLeastNEvents()

|

overrideprotectedvirtual |

Returns the probaility of having a given or larger number of defaults in the basket portfolio at a given time.

Reimplemented from DefaultLossModel.

Definition at line 227 of file randomdefaultlatentmodel.hpp.

Here is the call graph for this function:

◆ probsBeingNthEvent()

|

overrideprotectedvirtual |

Order of results refers to the simulated (super)pool not the basket's pool. Notice that this statistic suffers from heavy dispersion. To see techniques to improve it (not implemented here) see: Joshi, M., D. Kainth. 2004. Rapid and accurate development of prices and Greeks for nth to default credit swaps in the Li model. Quantitative Finance, Vol. 4. Institute of Physics Publishing, London, UK, 266-275 and: Chen, Z., Glasserman, P. 'Fast pricing of basket default swaps' in Operations Research Vol. 56, No. 2, March/April 2008, pp. 286-303

Reimplemented from DefaultLossModel.

Definition at line 254 of file randomdefaultlatentmodel.hpp.

Here is the call graph for this function:

◆ defaultCorrelation()

Pearsons' default probability correlation.

Reimplemented from DefaultLossModel.

Definition at line 297 of file randomdefaultlatentmodel.hpp.

Here is the call graph for this function:

◆ expectedTrancheLoss()

Reimplemented from DefaultLossModel.

Definition at line 338 of file randomdefaultlatentmodel.hpp.

◆ expectedTrancheLossInterval()

|

protectedvirtual |

Definition at line 345 of file randomdefaultlatentmodel.hpp.

Here is the call graph for this function:

◆ lossDistribution()

|

overrideprotectedvirtual |

Full loss distribution.

Reimplemented from DefaultLossModel.

Definition at line 384 of file randomdefaultlatentmodel.hpp.

Here is the call graph for this function:

◆ computeHistogram()

Definition at line 401 of file randomdefaultlatentmodel.hpp.

Here is the call graph for this function:

◆ expectedShortfall()

Expected shortfall given a default loss percentile.

Reimplemented from DefaultLossModel.

Definition at line 443 of file randomdefaultlatentmodel.hpp.

Here is the call graph for this function:

◆ percentile()

Value at Risk given a default loss percentile.

Reimplemented from DefaultLossModel.

Definition at line 525 of file randomdefaultlatentmodel.hpp.

◆ percentileAndInterval()

|

protectedvirtual |

Returns the VaR value for a given percentile and the 95 confidence interval of that value.

Definition at line 538 of file randomdefaultlatentmodel.hpp.

Here is the call graph for this function:

◆ splitVaRLevel()

Distributes the total VaR amount along the portfolio counterparties. The passed loss amount is in loss units.

Reimplemented from DefaultLossModel.

Definition at line 621 of file randomdefaultlatentmodel.hpp.

◆ splitVaRAndError()

|

protectedvirtual |

Distributes the total VaR amount along the portfolio counterparties.

Provides confidence interval for split so that portfolio optimization can be performed outside those limits.

The passed loss amount is in loss units.

Definition at line 636 of file randomdefaultlatentmodel.hpp.

Here is the call graph for this function:

Member Data Documentation

◆ seed_

|

private |

Definition at line 205 of file randomdefaultlatentmodel.hpp.

◆ numFactors_

|

protected |

Definition at line 207 of file randomdefaultlatentmodel.hpp.

◆ numLMVars_

|

protected |

Definition at line 208 of file randomdefaultlatentmodel.hpp.

◆ nSims_

|

protected |

Definition at line 210 of file randomdefaultlatentmodel.hpp.

◆ simsBuffer_

|

mutableprotected |

Definition at line 213 of file randomdefaultlatentmodel.hpp.

◆ copula_

|

mutableprotected |

Definition at line 215 of file randomdefaultlatentmodel.hpp.

◆ copulasRng_

|

mutableprotected |

Definition at line 216 of file randomdefaultlatentmodel.hpp.

◆ maxHorizon_

|

staticprotected |

Definition at line 219 of file randomdefaultlatentmodel.hpp.