#include <basket.hpp>

Inheritance diagram for Basket:

Inheritance diagram for Basket: Collaboration diagram for Basket:

Collaboration diagram for Basket:

Public Member Functions | |

| Basket ()=default | |

| Basket (const Date &refDate, const std::vector< std::string > &names, std::vector< Real > notionals, ext::shared_ptr< Pool > pool, Real attachmentRatio=0.0, Real detachmentRatio=1.0, ext::shared_ptr< Claim > claim=ext::shared_ptr< Claim >(new FaceValueClaim())) | |

| void | update () override |

| void | computeBasket () const |

| Size | size () const |

| Basket inception number of counterparties. More... | |

| const std::vector< std::string > & | names () const |

| Basket counterparties names at inception. More... | |

| const std::vector< Real > & | notionals () const |

| Basket counterparties notionals at inception. More... | |

| Real | notional () const |

| Basket total notional at inception. More... | |

| Real | exposure (const std::string &name, const Date &=Date()) const |

| Returns the total expected exposures for that name. More... | |

| const ext::shared_ptr< Pool > & | pool () const |

| Underlying pool. More... | |

| std::vector< DefaultProbKey > | defaultKeys () const |

| The keys each counterparty enters the basket with (sensitive to) More... | |

| const Date & | refDate () const |

| Basket inception date. More... | |

| Real | attachmentRatio () const |

| Real | detachmentRatio () const |

| Detachment point expressed as a fraction of the total pool notional. More... | |

| Real | basketNotional () const |

| Original basket notional ignoring any losses. More... | |

| Real | trancheNotional () const |

| Original tranche notional ignoring any realized losses. More... | |

| Real | attachmentAmount () const |

| Attachment amount = attachmentRatio() * basketNotional() More... | |

| Real | detachmentAmount () const |

| Detachment amount = detachmentRatio() * basketNotional() More... | |

| ext::shared_ptr< Claim > | claim () const |

| default claim, same for all positions and counterparties More... | |

| std::vector< Probability > | probabilities (const Date &d) const |

| Real | settledLoss () const |

| Real | settledLoss (const Date &) const |

| Real | cumulatedLoss () const |

| Real | cumulatedLoss (const Date &) const |

| Real | remainingNotional () const |

| Real | remainingNotional (const Date &) const |

| const std::vector< Real > & | remainingNotionals () const |

| std::vector< Real > | remainingNotionals (const Date &) const |

| const std::vector< std::string > & | remainingNames () const |

| std::vector< std::string > | remainingNames (const Date &) const |

| const std::vector< DefaultProbKey > & | remainingDefaultKeys () const |

| std::vector< DefaultProbKey > | remainingDefaultKeys (const Date &) const |

| Size | remainingSize () const |

| Number of counterparties alive on the requested date. More... | |

| Size | remainingSize (const Date &) const |

| std::vector< Probability > | remainingProbabilities (const Date &d) const |

| Real | remainingAttachmentAmount () const |

| Real | remainingAttachmentAmount (const Date &endDate) const |

| Real | remainingDetachmentAmount () const |

| Real | remainingDetachmentAmount (const Date &endDate) const |

| Real | remainingTrancheNotional () const |

| Remaining basket tranched notional on calculation date. More... | |

| Real | remainingTrancheNotional (const Date &endDate) const |

| const std::vector< Size > & | liveList () const |

| Indexes of remaining names. Notice these are names and not positions. More... | |

| std::vector< Size > | liveList (const Date &) const |

| void | setLossModel (const ext::shared_ptr< DefaultLossModel > &lossModel) |

| Assigns the default loss model to this basket. Resets calculations. More... | |

| Public Member Functions inherited from LazyObject | |

| LazyObject () | |

| ~LazyObject () override=default | |

| void | update () override |

| bool | isCalculated () const |

| void | forwardFirstNotificationOnly () |

| void | alwaysForwardNotifications () |

| void | recalculate () |

| void | freeze () |

| void | unfreeze () |

| Public Member Functions inherited from Observable | |

| Observable ()=default | |

| Observable (const Observable &) | |

| Observable & | operator= (const Observable &) |

| Observable (Observable &&)=delete | |

| Observable & | operator= (Observable &&)=delete |

| virtual | ~Observable ()=default |

| void | notifyObservers () |

| Public Member Functions inherited from Observer | |

| Observer ()=default | |

| Observer (const Observer &) | |

| Observer & | operator= (const Observer &) |

| virtual | ~Observer () |

| std::pair< iterator, bool > | registerWith (const ext::shared_ptr< Observable > &) |

| void | registerWithObservables (const ext::shared_ptr< Observer > &) |

| Size | unregisterWith (const ext::shared_ptr< Observable > &) |

| void | unregisterWithAll () |

| virtual void | update ()=0 |

| virtual void | deepUpdate () |

Basket Loss Statistics | |

Methods providing statistical metrics on the loss or value distribution of the basket. Most calculations rely on the pressence of a model assigned to the basket. | |

| std::vector< Real > | notionals_ |

| ext::shared_ptr< Pool > | pool_ |

| const ext::shared_ptr< Claim > | claim_ |

| The claim is the same for all names. More... | |

| Real | attachmentRatio_ |

| Real | detachmentRatio_ |

| Real | basketNotional_ |

| Real | attachmentAmount_ |

| basket tranched inception attachment amount: More... | |

| Real | detachmentAmount_ |

| basket tranched inception detachment amount: More... | |

| Real | trancheNotional_ |

| basket tranched notional amount: More... | |

| Real | evalDateSettledLoss_ |

| Real | evalDateRemainingNot_ |

| Real | evalDateAttachAmount_ |

| Real | evalDateDetachAmmount_ |

| std::vector< Size > | evalDateLiveList_ |

| std::vector< Real > | evalDateLiveNotionals_ |

| std::vector< std::string > | evalDateLiveNames_ |

| std::vector< DefaultProbKey > | evalDateLiveKeys_ |

| const Date | refDate_ |

| Basket inception date. More... | |

| ext::shared_ptr< DefaultLossModel > | lossModel_ |

| Real | expectedTrancheLoss (const Date &d) const |

| Probability | probOverLoss (const Date &d, Real lossFraction) const |

| Real | percentile (const Date &d, Probability prob) const |

| Real | expectedShortfall (const Date &d, Probability prob) const |

| std::vector< Real > | splitVaRLevel (const Date &date, Real loss) const |

| std::map< Real, Probability > | lossDistribution (const Date &) const |

| Real | densityTrancheLoss (const Date &d, Real lossFraction) const |

| Real | defaultCorrelation (const Date &d, Size iName, Size jName) const |

| std::vector< Probability > | probsBeingNthEvent (Size n, const Date &d) const |

| Probability | probAtLeastNEvents (Size n, const Date &d) const |

| Real | recoveryRate (const Date &d, Size iName) const |

| void | performCalculations () const override |

Additional Inherited Members | |

| Public Types inherited from Observer | |

| typedef set_type::iterator | iterator |

| Protected Member Functions inherited from LazyObject | |

| virtual void | calculate () const |

| Protected Attributes inherited from LazyObject | |

| bool | calculated_ = false |

| bool | frozen_ = false |

| bool | alwaysForward_ |

Detailed Description

Credit Basket.

- A basket is a collection of credit names, represented by a unique identifier (a text string), associated notional amounts, a pool and tranche information. The pool is a map of "names" to issuers. The Basket structure is motivated by CDO squared instruments containing various underlying inner CDOs which can be represented by respective baskets including their tranche structure. The role of the Pool is providing a unique list of relevant issuers while names may appear multiple times across different baskets (overlap).

Definition at line 52 of file basket.hpp.

Constructor & Destructor Documentation

◆ Basket() [1/2]

|

default |

◆ Basket() [2/2]

| Basket | ( | const Date & | refDate, |

| const std::vector< std::string > & | names, | ||

| std::vector< Real > | notionals, | ||

| ext::shared_ptr< Pool > | pool, | ||

| Real | attachmentRatio = 0.0, |

||

| Real | detachmentRatio = 1.0, |

||

| ext::shared_ptr< Claim > | claim = ext::shared_ptr<Claim>(new FaceValueClaim()) |

||

| ) |

Constructs a basket of simple collection of constant notional positions subject to default risk only.

The refDate parameter is the basket inception date, that is, the date at which defaultable events are relevant. (There are no constraints on forward baskets but models assigned should be consistent.)

Definition at line 33 of file basket.cpp.

Here is the call graph for this function:

Member Function Documentation

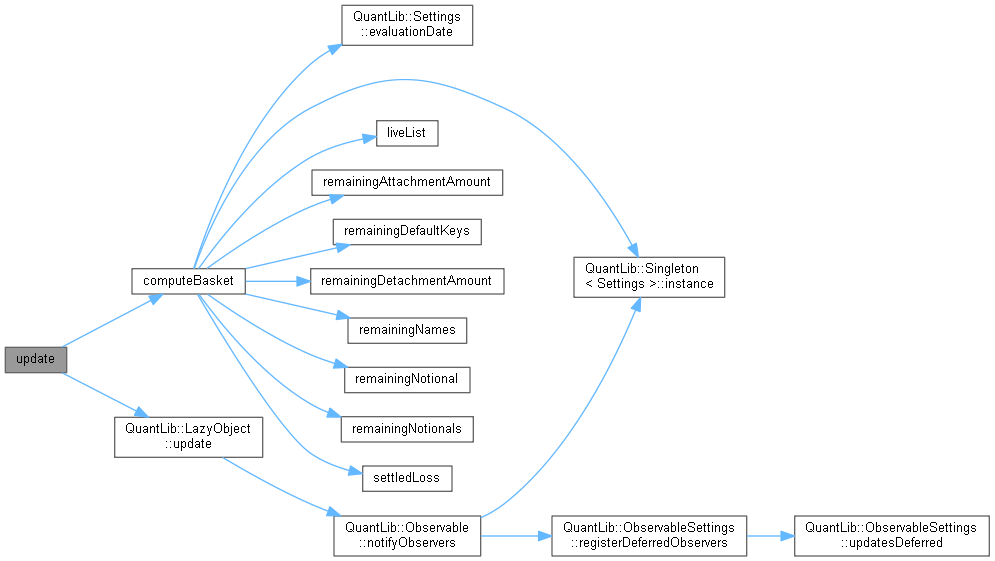

◆ update()

|

overridevirtual |

This method must be implemented in derived classes. An instance of Observer does not call this method directly: instead, it will be called by the observables the instance registered with when they need to notify any changes.

Implements Observer.

Definition at line 70 of file basket.hpp.

Here is the call graph for this function:

◆ computeBasket()

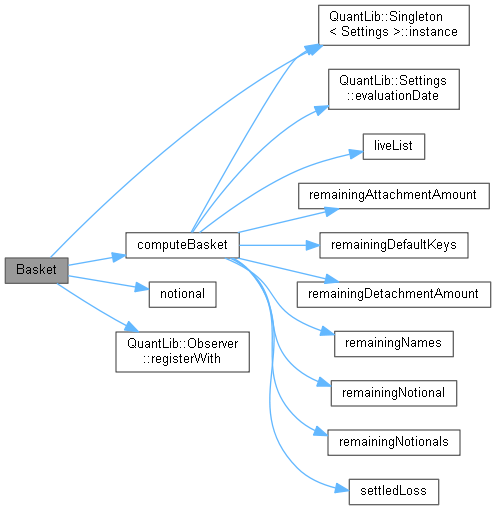

| void computeBasket | ( | ) | const |

Definition at line 74 of file basket.hpp.

Here is the call graph for this function: Here is the caller graph for this function:

Here is the caller graph for this function:

◆ size()

| Size size | ( | ) | const |

Basket inception number of counterparties.

Definition at line 317 of file basket.hpp.

Here is the caller graph for this function:

◆ names()

| const std::vector< std::string > & names | ( | ) | const |

Basket counterparties names at inception.

Definition at line 95 of file basket.hpp.

◆ notionals()

| const std::vector< Real > & notionals | ( | ) | const |

Basket counterparties notionals at inception.

Definition at line 321 of file basket.hpp.

◆ notional()

| Real notional | ( | ) | const |

Basket total notional at inception.

Definition at line 106 of file basket.cpp.

Here is the caller graph for this function:

◆ exposure()

Returns the total expected exposures for that name.

Definition at line 226 of file basket.cpp.

Here is the caller graph for this function:

◆ pool()

| const ext::shared_ptr< Pool > & pool | ( | ) | const |

Underlying pool.

Definition at line 329 of file basket.hpp.

◆ defaultKeys()

| std::vector< DefaultProbKey > defaultKeys | ( | ) | const |

The keys each counterparty enters the basket with (sensitive to)

Definition at line 325 of file basket.hpp.

Here is the caller graph for this function:

◆ refDate()

| const Date & refDate | ( | ) | const |

Basket inception date.

Loss Given Default for all issuers/notionals based on expected recovery rates for the respective issuers.

Definition at line 110 of file basket.hpp.

◆ attachmentRatio()

| Real attachmentRatio | ( | ) | const |

Attachment point expressed as a fraction of the total inception notional.

Definition at line 114 of file basket.hpp.

◆ detachmentRatio()

| Real detachmentRatio | ( | ) | const |

Detachment point expressed as a fraction of the total pool notional.

Definition at line 116 of file basket.hpp.

◆ basketNotional()

| Real basketNotional | ( | ) | const |

Original basket notional ignoring any losses.

Definition at line 118 of file basket.hpp.

◆ trancheNotional()

| Real trancheNotional | ( | ) | const |

Original tranche notional ignoring any realized losses.

Definition at line 120 of file basket.hpp.

◆ attachmentAmount()

| Real attachmentAmount | ( | ) | const |

Attachment amount = attachmentRatio() * basketNotional()

Definition at line 122 of file basket.hpp.

◆ detachmentAmount()

| Real detachmentAmount | ( | ) | const |

Detachment amount = detachmentRatio() * basketNotional()

Definition at line 124 of file basket.hpp.

◆ claim()

| ext::shared_ptr< Claim > claim | ( | ) | const |

default claim, same for all positions and counterparties

Definition at line 126 of file basket.hpp.

◆ probabilities()

Vector of cumulative default probability to date d for all issuers in the basket.

Definition at line 110 of file basket.cpp.

Here is the call graph for this function:

◆ settledLoss() [1/2]

| Real settledLoss | ( | ) | const |

Realized basket losses between the reference date and the calculation date, taking the actual recovery rates of loss events into account. Only default events that have settled (have a realized RR) are accounted for. For contingent losses after a default you need to compute the losses through a DefaultLossModel

Optionally one can pass a date in the future and that will collect events stored in the issuers list. This shows the effect of 'programmed' (after today's) events on top of past ones. The intention is to be used in risk analysis (jump to default, etc).

Definition at line 357 of file basket.hpp.

Here is the caller graph for this function:

◆ settledLoss() [2/2]

◆ cumulatedLoss() [1/2]

| Real cumulatedLoss | ( | ) | const |

Actual basket losses between the reference date and the calculation date, taking the actual recovery rates of loss events into account. If the event has not settled yet a model driven recovery is used.

Returns the realized losses in this portfolio since the portfolio default reference date. This method relies on an implementation of the loss given default since the events have not necessarily settled.

Definition at line 353 of file basket.hpp.

Here is the caller graph for this function:

◆ cumulatedLoss() [2/2]

◆ remainingNotional() [1/2]

| Real remainingNotional | ( | ) | const |

Remaining full basket (untranched) notional after settled losses between the reference date and the given date. The full notional for defaulted names is subracted, recovery ignored.

Definition at line 168 of file basket.cpp.

Here is the caller graph for this function:

◆ remainingNotional() [2/2]

◆ remainingNotionals() [1/2]

| const std::vector< Real > & remainingNotionals | ( | ) | const |

Vector of surviving notionals after settled losses between the reference date and the given date, recovery ignored.

Definition at line 349 of file basket.hpp.

Here is the caller graph for this function:

◆ remainingNotionals() [2/2]

◆ remainingNames() [1/2]

| const std::vector< std::string > & remainingNames | ( | ) | const |

Vector of surviving issuers after defaults between the reference basket date and the given (or evaluation) date.

Definition at line 345 of file basket.hpp.

Here is the caller graph for this function:

◆ remainingNames() [2/2]

| std::vector< std::string > remainingNames | ( | const Date & | endDate | ) | const |

◆ remainingDefaultKeys() [1/2]

| const std::vector< DefaultProbKey > & remainingDefaultKeys | ( | ) | const |

Default keys of non defaulted counterparties

Definition at line 362 of file basket.hpp.

Here is the caller graph for this function:

◆ remainingDefaultKeys() [2/2]

| vector< DefaultProbKey > remainingDefaultKeys | ( | const Date & | endDate | ) | const |

◆ remainingSize() [1/2]

| Size remainingSize | ( | ) | const |

Number of counterparties alive on the requested date.

Definition at line 275 of file basket.cpp.

◆ remainingSize() [2/2]

◆ remainingProbabilities()

| std::vector< Probability > remainingProbabilities | ( | const Date & | d | ) | const |

Vector of cumulative default probability to date d for all issuers still (at the evaluation date) alive in the basket.

Definition at line 211 of file basket.cpp.

Here is the call graph for this function:

◆ remainingAttachmentAmount() [1/2]

| Real remainingAttachmentAmount | ( | ) | const |

Attachment amount of the equivalent (after defaults) remaining basket The remaining attachment amount is RAA = max (0, attachmentAmount - cumulatedLoss())

The remaining attachment ratio is then RAR = RAA / remainingNotional()

Definition at line 341 of file basket.hpp.

Here is the caller graph for this function:

◆ remainingAttachmentAmount() [2/2]

◆ remainingDetachmentAmount() [1/2]

| Real remainingDetachmentAmount | ( | ) | const |

Detachment amount of the equivalent remaining basket. The remaining detachment amount is RDA = max (0, detachmentAmount - cumulatedLoss())

The remaining detachment ratio is then RDR = RDA / remainingNotional()

Definition at line 337 of file basket.hpp.

Here is the caller graph for this function:

◆ remainingDetachmentAmount() [2/2]

Definition at line 286 of file basket.cpp.

◆ remainingTrancheNotional() [1/2]

| Real remainingTrancheNotional | ( | ) | const |

Remaining basket tranched notional on calculation date.

Definition at line 206 of file basket.hpp.

Here is the call graph for this function:

◆ remainingTrancheNotional() [2/2]

Expected basket tranched notional on the requested date according to the basket model. Model should have been assigned.

Definition at line 213 of file basket.hpp.

Here is the call graph for this function:

◆ liveList() [1/2]

| const std::vector< Size > & liveList | ( | ) | const |

Indexes of remaining names. Notice these are names and not positions.

Definition at line 333 of file basket.hpp.

Here is the caller graph for this function:

◆ liveList() [2/2]

◆ setLossModel()

| void setLossModel | ( | const ext::shared_ptr< DefaultLossModel > & | lossModel | ) |

Assigns the default loss model to this basket. Resets calculations.

Definition at line 74 of file basket.cpp.

Here is the call graph for this function:

◆ expectedTrancheLoss()

◆ probOverLoss()

| Probability probOverLoss | ( | const Date & | d, |

| Real | lossFraction | ||

| ) | const |

The lossFraction is the fraction of losses expressed in inception (no losses) tranche units (e.g. 'attach level'=0%, 'detach level'=100%)

Definition at line 301 of file basket.cpp.

Here is the call graph for this function:

◆ percentile()

| Real percentile | ( | const Date & | d, |

| Probability | prob | ||

| ) | const |

◆ expectedShortfall()

| Real expectedShortfall | ( | const Date & | d, |

| Probability | prob | ||

| ) | const |

◆ splitVaRLevel()

◆ lossDistribution()

| std::map< Real, Probability > lossDistribution | ( | const Date & | d | ) | const |

Full loss distribution

Definition at line 340 of file basket.cpp.

Here is the call graph for this function:

◆ densityTrancheLoss()

◆ defaultCorrelation()

◆ probsBeingNthEvent()

| std::vector< Probability > probsBeingNthEvent | ( | Size | n, |

| const Date & | d | ||

| ) | const |

Probability vector that each of the remaining live names (at eval date) is the n-th default by date d.

The n parameter is the internal index to the name; it should be alive at the evaluation date.

------—TO DO: Implement with a string passed-------------------— ------—TO DO: Perform check the name is alive------------------—

Definition at line 346 of file basket.cpp.

Here is the call graph for this function:

◆ probAtLeastNEvents()

| Probability probAtLeastNEvents | ( | Size | n, |

| const Date & | d | ||

| ) | const |

Returns the probaility of having a given or larger number of defaults in the basket portfolio at a given time.

Definition at line 365 of file basket.cpp.

Here is the call graph for this function:

◆ recoveryRate()

Expected recovery rate of the underlying position as a fraction of its exposure value at date d given it has defaulted on that date. NOTICE THE ARG IS THE CTPTY....SHOULDNT IT BE THE POSITION/INSTRUMENT?????<<<<<<<<<<<<<<<<<<<<<<<

Definition at line 371 of file basket.cpp.

Here is the call graph for this function:

◆ performCalculations()

|

overrideprivatevirtual |

This method must implement any calculations which must be (re)done in order to calculate the desired results.

Implements LazyObject.

Definition at line 88 of file basket.cpp.

Here is the call graph for this function:

Member Data Documentation

◆ notionals_

|

private |

Definition at line 275 of file basket.hpp.

◆ pool_

|

private |

Definition at line 276 of file basket.hpp.

◆ claim_

|

private |

The claim is the same for all names.

Definition at line 278 of file basket.hpp.

◆ attachmentRatio_

|

private |

Definition at line 280 of file basket.hpp.

◆ detachmentRatio_

|

private |

Definition at line 281 of file basket.hpp.

◆ basketNotional_

|

private |

Definition at line 282 of file basket.hpp.

◆ attachmentAmount_

|

mutableprivate |

basket tranched inception attachment amount:

Definition at line 284 of file basket.hpp.

◆ detachmentAmount_

|

mutableprivate |

basket tranched inception detachment amount:

Definition at line 286 of file basket.hpp.

◆ trancheNotional_

|

mutableprivate |

basket tranched notional amount:

Definition at line 288 of file basket.hpp.

◆ evalDateSettledLoss_

|

mutableprivate |

Definition at line 294 of file basket.hpp.

◆ evalDateRemainingNot_

|

private |

Definition at line 295 of file basket.hpp.

◆ evalDateAttachAmount_

|

private |

Definition at line 296 of file basket.hpp.

◆ evalDateDetachAmmount_

|

private |

Definition at line 297 of file basket.hpp.

◆ evalDateLiveList_

|

mutableprivate |

Definition at line 298 of file basket.hpp.

◆ evalDateLiveNotionals_

|

mutableprivate |

Definition at line 299 of file basket.hpp.

◆ evalDateLiveNames_

|

mutableprivate |

Definition at line 300 of file basket.hpp.

◆ evalDateLiveKeys_

|

mutableprivate |

Definition at line 301 of file basket.hpp.

◆ refDate_

|

private |

Basket inception date.

Definition at line 303 of file basket.hpp.

◆ lossModel_

|

private |

Definition at line 312 of file basket.hpp.