Generic multifactor latent variable model. More...

#include <latentmodel.hpp>

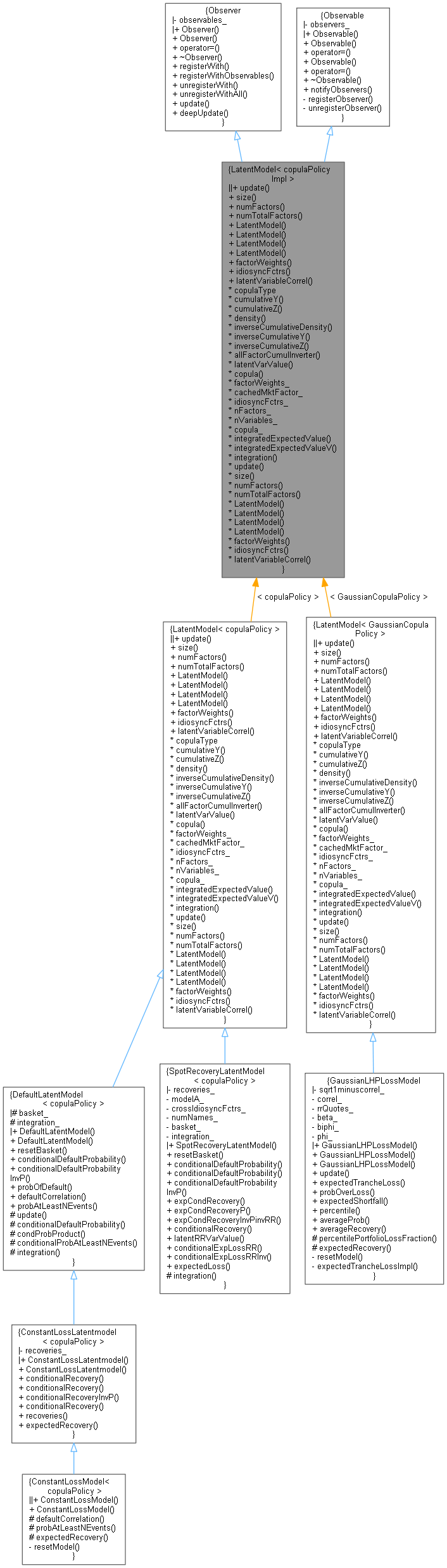

Inheritance diagram for LatentModel< copulaPolicyImpl >:

Inheritance diagram for LatentModel< copulaPolicyImpl >: Collaboration diagram for LatentModel< copulaPolicyImpl >:

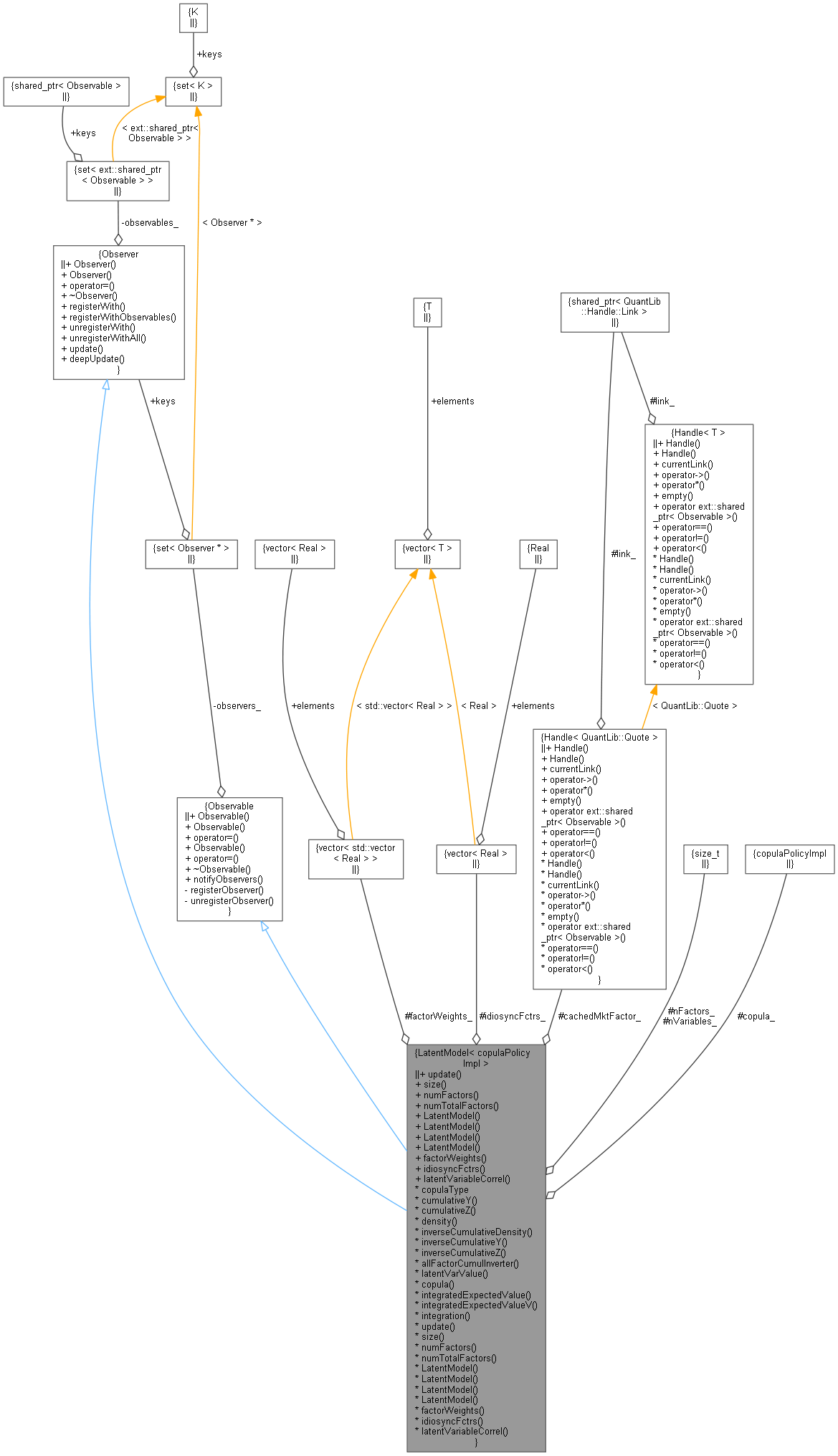

Collaboration diagram for LatentModel< copulaPolicyImpl >:

Classes | |

| class | FactorSampler |

| class | IntegrationFactory |

Public Member Functions | |

Latent model direct integration facility. | |

| void | update () override |

Latent model random factor number generator facility. | |

| Size | size () const |

| Size | numFactors () const |

| Number of systemic factors. More... | |

| Size | numTotalFactors () const |

| Number of total free random factors; systemic and idiosyncratic. More... | |

| LatentModel (const std::vector< std::vector< Real > > &factorsWeights, const typename copulaType::initTraits &ini=typename copulaType::initTraits()) | |

| LatentModel (const std::vector< Real > &factorsWeight, const typename copulaType::initTraits &ini=typename copulaType::initTraits()) | |

| LatentModel (Real correlSqr, Size nVariables, const typename copulaType::initTraits &ini=typename copulaType::initTraits()) | |

| LatentModel (const Handle< Quote > &singleFactorCorrel, Size nVariables, const typename copulaType::initTraits &ini=typename copulaType::initTraits()) | |

| const std::vector< std::vector< Real > > & | factorWeights () const |

| Provides values of the factors \( a_{i,k} \). More... | |

| const std::vector< Real > & | idiosyncFctrs () const |

| Provides values of the normalized idiosyncratic factors \( Z_i \). More... | |

| Real | latentVariableCorrel (Size iVar1, Size iVar2) const |

| Latent variable correlations: More... | |

| Public Member Functions inherited from Observer | |

| Observer ()=default | |

| Observer (const Observer &) | |

| Observer & | operator= (const Observer &) |

| virtual | ~Observer () |

| std::pair< iterator, bool > | registerWith (const ext::shared_ptr< Observable > &) |

| void | registerWithObservables (const ext::shared_ptr< Observer > &) |

| Size | unregisterWith (const ext::shared_ptr< Observable > &) |

| void | unregisterWithAll () |

| virtual void | update ()=0 |

| virtual void | deepUpdate () |

| Public Member Functions inherited from Observable | |

| Observable ()=default | |

| Observable (const Observable &) | |

| Observable & | operator= (const Observable &) |

| Observable (Observable &&)=delete | |

| Observable & | operator= (Observable &&)=delete |

| virtual | ~Observable ()=default |

| void | notifyObservers () |

Copula interface. | |

| typedef copulaPolicyImpl | copulaType |

| Probability | cumulativeY (Real val, Size iVariable) const |

| Probability | cumulativeZ (Real z) const |

| Cumulative distribution of Z, the idiosyncratic/error factors. More... | |

| Probability | density (const std::vector< Real > &m) const |

| Density function of M, the market/systemic factors. More... | |

| Real | inverseCumulativeDensity (Probability p, Size iFactor) const |

| Inverse cumulative distribution of the systemic factor iFactor. More... | |

| Real | inverseCumulativeY (Probability p, Size iVariable) const |

| Real | inverseCumulativeZ (Probability p) const |

| std::vector< Real > | allFactorCumulInverter (const std::vector< Real > &probs) const |

| Real | latentVarValue (const std::vector< Real > &allFactors, Size iVar) const |

| const copulaType & | copula () const |

Integration facility interface | |

| std::vector< std::vector< Real > > | factorWeights_ |

| Handle< Quote > | cachedMktFactor_ |

| std::vector< Real > | idiosyncFctrs_ |

| Size | nFactors_ |

| Number of systemic factors. More... | |

| Size | nVariables_ |

| Number of latent model variables, idiosyncratic terms or model dim. More... | |

| copulaType | copula_ |

| Real | integratedExpectedValue (const std::function< Real(const std::vector< Real > &v1)> &f) const |

| std::vector< Real > | integratedExpectedValueV (const std::function< std::vector< Real >(const std::vector< Real > &v1)> &f) const |

| virtual const ext::shared_ptr< LMIntegration > & | integration () const |

Additional Inherited Members | |

| Public Types inherited from Observer | |

| typedef set_type::iterator | iterator |

Detailed Description

class QuantLib::LatentModel< copulaPolicyImpl >

Generic multifactor latent variable model.

- In this model set up one considers latent (random) variables \( Y_i \) described by:

\[ \begin{array}{ccccc} Y_1 & = & \sum_k M_k a_{1,k} & + \sqrt{1-\sum_k a_{1,k}^2} Z_1 & \sim \Phi_{Y_1}\nonumber \\ ... & = & ... & ... & \nonumber \\ Y_i & = & \sum_k M_k a_{i,k} & + \sqrt{1-\sum_k a_{i,k}^2} Z_i & \sim \Phi_{Y_i}\nonumber \\ ... & = & ... & ... & \nonumber \\ Y_N & = & \sum_k M_k a_{N,k} & + \sqrt{1-\sum_k a_{N,k}^2} Z_N & \sim \Phi_{Y_N} \end{array} \]

where the systemic \( M_k \) and idiosyncratic \( Z_i \) (this last one known as error term in some contexts) random variables have independent zero-mean unit-variance distributions. A restriction of the model implemented here is that the N idiosyncratic variables all follow the same probability law \( \Phi_Z(z)\) (but they are still independent random variables) Also the model is normalized so that: \(-1\leq a_{i,k} \leq 1\) (technically the \(Y_i\) are convex linear combinations). The correlation between \(Y_i\) and \(Y_j\) is then \(\sum_k a_{i,k} a_{j,k}\). \(\Phi_{Y_i}\) denotes the cumulative distribution function of \(Y_i\) which in general differs for each latent variable.

- In its single factor set up this model is usually employed in derivative pricing and it is best to use it through integration of the desired statistical properties of the model; in its multifactorial version (with typically around a dozen factors) it is used in the context of portfolio risk metrics; because of the number of variables it is best to opt for a simulation to compute model properties/magnitudes. For this reason this class template provides a random factor sample interface and an integration interface that will be instantiated by derived concrete models as needed. The class is neutral on the integration and random generation algorithms

- The latent variables are typically treated as unobservable magnitudes and they serve to model one or several magnitudes related to them through some function

\[ \begin{array}{ccc} F_i(Y_i) & = & F_i(\sum_k M_k a_{i,k} + \sqrt{1-\sum_k a_{i,k}^2} Z_i )\nonumber \\ & = & F_i(M_1,..., M_k, ..., M_K, Z_i) \end{array} \]

The transfer function can have a more generic form: \(F_i(Y_1,....,Y_N)\) but here the model is restricted to a one to one relation between the latent variables and the modelled ones. Also it is assumed that \(F_i(y_i; \tau)\) is monotonic in \(y_i\); it can then be inverted and the relation of the cumulative probability of \(F_i\) and \(Y_i\) is simple:\[ \int_{\infty}^b \phi_{F_i} df = \int_{\infty}^{F_i^{-1}(b)} \phi_{Y_i} dy \]

If \(t\) is some value of the functional or modelled variable, \(y\) is mapped to \(t\) such that percentiles match, i.e. \(F_Y(y)=Q_i(t)\) or \(y=F_Y^{-1}(Q_i(t))\). The class provides an integration facility of arbitrary functions dependent on the model states. It also provides random number generation interfaces for usage of the model in monte carlo simulations.

- Now let \(\Phi_Z(z)\) be the cumulated distribution function of (all equal as mentioned) \(Z_i\). For a given realization of \(M_k\), this determines the distribution of \(y\):

\[ Prob \,(Y_i < y|M_k) = \Phi_Z \left( \frac{y-\sum_k a_{i,k}\,M_k} {\sqrt{1-\sum_k a_{i,k}^2}}\right) \qquad \mbox{or} \qquad Prob \,(t_i < t|M) = \Phi_Z \left( \frac {F_{Y_{i}}^{-1}(Q_i(t))-\sum_k a_{i,k}\,M_k} {\sqrt{1-\sum_k a_{i,k}^2}} \right) \]

The distribution functions of \( M_k, Z_i \) are specified in specific copula template classes. The distribution function of \( Y_i \) is then given by the convolution\[ F_{Y_{i}}(y) = Prob\,(Y_i<y) = \int_{-\infty}^\infty\,\cdots\,\int_{-\infty}^{\infty}\: D_Z(z)\,\prod_k D_{M_{k}}(m_k) \quad \Theta \left(y - \sum_k a_{i,k}m_k - \sqrt{1-\sum_k a_{i,k}^2}\,z\right)\,d\bar{m}\,dz, \qquad \Theta (x) = \left\{ \begin{array}{ll} 1 & x \geq 0 \\ 0 & x < 0 \end{array}\right. \]

where \( D_Z(z) \) and \( D_M(m) \) are the probability densities of \( Z\) and \( M, \) respectively.

- This convolution can also be written

\[ F_{Y_{i}}(y) = Prob \,(Y_i < y) = \int_{-\infty}^\infty\,\cdots\,\int_{-\infty}^{\infty} D_{M_{k}}(m_k)\,dm_k\: \int_{-\infty}^{g(y,\vec{a},\vec{m})} D_Z(z)\,dz, \qquad g(y,\vec{a},\vec{m}) = \frac{y - \sum_k a_{i,k}m_k} {\sqrt{1-\sum_k a_{i,k}^2}}, \qquad \sum_k a_{i,k}^2 < 1 \]

In general, \( F_{Y_{i}}(y) \) needs to be computed numerically.

- The policy class template separates the copula function (the distributions involved) and the functionality (i.e. what the latent

model represents: a default probability, a recovery...). Since the

copula methods for the probabilities are to be called repeatedly from an integration or a MC simulation, virtual tables are avoided and template parameter mechnics is preferred.

- There is nothing at this level enforncing the requirement on the factor distributions to be of zero mean and unit variance. Thats the user responsibility and the model fails to behave correctly if it is not the case.

- Derived classes should implement a modelled magnitude (default time, etc) and will provide probability distributions and conditional values. They could also provide functionality for the parameter inversion problem, the (e.g.) time at which the modeled variable first takes a given value. This problem has solution/sense depending on the transfer function \(F_i(Y_i)\) characteristics.

To make direct integration and simulation time efficient virtual functions have been avoided in accessing methods in the copula policy and in the sampling of the random factors

Definition at line 278 of file latentmodel.hpp.

Member Typedef Documentation

◆ copulaType

| typedef copulaPolicyImpl copulaType |

Definition at line 285 of file latentmodel.hpp.

Constructor & Destructor Documentation

◆ LatentModel() [1/4]

|

explicit |

Constructs a LM with an arbitrary number of latent variables and factors given by the dimensions of the passed matrix.

- Parameters

-

factorsWeights Ordering is factorWeights_[iVar][iFactor] ini Initialization variables. Trait type from the copula policy to allow for static policies (this solution needs to be revised, possibly drop the static policy and create a policy member in LatentModel)

◆ LatentModel() [2/4]

|

explicit |

Constructs a LM with an arbitrary number of latent variables depending only on one random factor but contributing to each latent variable through different weights.

- Parameters

-

factorsWeight Ordering is factorWeights_[iVariable] ini Initialization variables. Trait type from the copula policy to allow for static policies (this solution needs to be revised, possibly drop the static policy and create a policy member in LatentModel)

◆ LatentModel() [3/4]

|

explicit |

Constructs a LM with an arbitrary number of latent variables depending only on one random factor with the same weight for all latent variables.

correlSqr is the weight, same for all.

ini is a trait type from the copula policy, to allow for static policies (this solution needs to be revised, possibly drop the static policy and create a policy member in LatentModel)

◆ LatentModel() [4/4]

|

explicit |

Constructs a LM with an arbitrary number of latent variables depending only on one random factor with the same weight for all latent variables. The weight is observed and this constructor is intended to be used when the model relates to a market value.

singleFactorCorrel is the weight/mkt-factor, same for all.

ini is a trait type from the copula policy, to allow for static policies (this solution needs to be revised, possibly drop the static policy and create a policy member in LatentModel)

Member Function Documentation

◆ update()

|

overridevirtual |

This method must be implemented in derived classes. An instance of Observer does not call this method directly: instead, it will be called by the observables the instance registered with when they need to notify any changes.

Implements Observer.

Definition at line 711 of file latentmodel.hpp.

Here is the caller graph for this function:

◆ cumulativeY()

| Probability cumulativeY | ( | Real | val, |

| Size | iVariable | ||

| ) | const |

Cumulative probability of the \( Y_i \) modelled latent random variable to take a given value.

Definition at line 289 of file latentmodel.hpp.

◆ cumulativeZ()

| Probability cumulativeZ | ( | Real | z | ) | const |

Cumulative distribution of Z, the idiosyncratic/error factors.

Definition at line 293 of file latentmodel.hpp.

◆ density()

| Probability density | ( | const std::vector< Real > & | m | ) | const |

Density function of M, the market/systemic factors.

Definition at line 297 of file latentmodel.hpp.

◆ inverseCumulativeDensity()

| Real inverseCumulativeDensity | ( | Probability | p, |

| Size | iFactor | ||

| ) | const |

Inverse cumulative distribution of the systemic factor iFactor.

Definition at line 305 of file latentmodel.hpp.

◆ inverseCumulativeY()

| Real inverseCumulativeY | ( | Probability | p, |

| Size | iVariable | ||

| ) | const |

Inverse cumulative value of the i-th random latent variable with a given probability.

Definition at line 310 of file latentmodel.hpp.

◆ inverseCumulativeZ()

| Real inverseCumulativeZ | ( | Probability | p | ) | const |

Inverse cumulative value of the idiosyncratic variable with a given probability.

Definition at line 315 of file latentmodel.hpp.

◆ allFactorCumulInverter()

All factor cumulative inversion. Used in integrations and sampling. Inverts all the cumulative random factors probabilities in the model. These are all the systemic factors plus all the idiosyncratic ones, so the size of the inversion is the number of systemic factors plus the number of latent modelled variables

Definition at line 323 of file latentmodel.hpp.

◆ latentVarValue()

The value of the latent variable Y_i conditional to (given) a set of values of the factors.

The passed allFactors vector contains values for all the independent factors in the model (systemic and idiosyncratic, in that order). A full sample is required, i.e. all the idiosyncratic values are expected to be present even if only the relevant one is used.

Definition at line 337 of file latentmodel.hpp.

Here is the call graph for this function:

◆ copula()

| const copulaType & copula | ( | ) | const |

Definition at line 348 of file latentmodel.hpp.

◆ size()

| Size size | ( | ) | const |

Definition at line 499 of file latentmodel.hpp.

◆ numFactors()

| Size numFactors | ( | ) | const |

Number of systemic factors.

Definition at line 501 of file latentmodel.hpp.

Here is the caller graph for this function:

◆ numTotalFactors()

| Size numTotalFactors | ( | ) | const |

Number of total free random factors; systemic and idiosyncratic.

Definition at line 503 of file latentmodel.hpp.

◆ factorWeights()

| const std::vector< std::vector< Real > > & factorWeights | ( | ) | const |

Provides values of the factors \( a_{i,k} \).

Definition at line 561 of file latentmodel.hpp.

◆ idiosyncFctrs()

| const std::vector< Real > & idiosyncFctrs | ( | ) | const |

Provides values of the normalized idiosyncratic factors \( Z_i \).

Definition at line 565 of file latentmodel.hpp.

◆ latentVariableCorrel()

Latent variable correlations:

Definition at line 568 of file latentmodel.hpp.

◆ integratedExpectedValue()

Integrates an arbitrary scalar function over the density domain(i.e. computes its expected value).

Definition at line 581 of file latentmodel.hpp.

Here is the call graph for this function:

◆ integratedExpectedValueV()

| std::vector< Real > integratedExpectedValueV | ( | const std::function< std::vector< Real >(const std::vector< Real > &v1)> & | f | ) | const |

Integrates an arbitrary vector function over the density domain(i.e. computes its expected value).

Definition at line 591 of file latentmodel.hpp.

Here is the call graph for this function:

◆ integration()

|

protectedvirtual |

Reimplemented in DefaultLatentModel< copulaPolicy >, and SpotRecoveryLatentModel< copulaPolicy >.

Definition at line 603 of file latentmodel.hpp.

Here is the caller graph for this function:

Member Data Documentation

◆ factorWeights_

|

mutableprotected |

Definition at line 609 of file latentmodel.hpp.

◆ cachedMktFactor_

Definition at line 623 of file latentmodel.hpp.

◆ idiosyncFctrs_

|

mutableprotected |

Definition at line 628 of file latentmodel.hpp.

◆ nFactors_

|

mutableprotected |

Number of systemic factors.

Definition at line 630 of file latentmodel.hpp.

◆ nVariables_

|

mutableprotected |

Number of latent model variables, idiosyncratic terms or model dim.

Definition at line 632 of file latentmodel.hpp.

◆ copula_

|

mutableprotected |

Definition at line 634 of file latentmodel.hpp.