purely virtual base class for market observables More...

#include <quote.hpp>

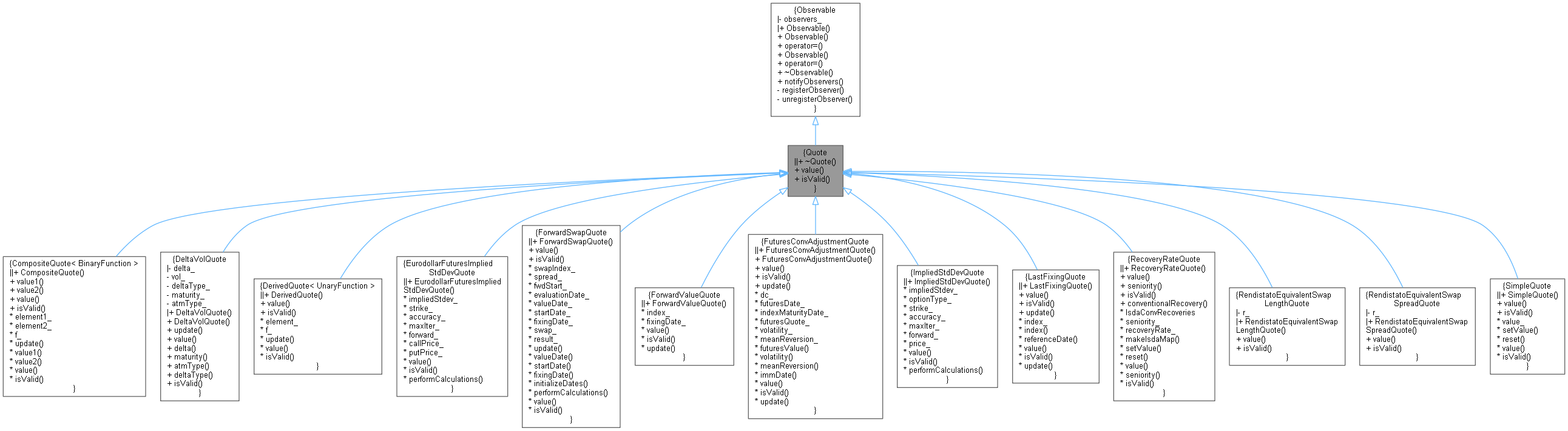

Inheritance diagram for Quote:

Inheritance diagram for Quote: Collaboration diagram for Quote:

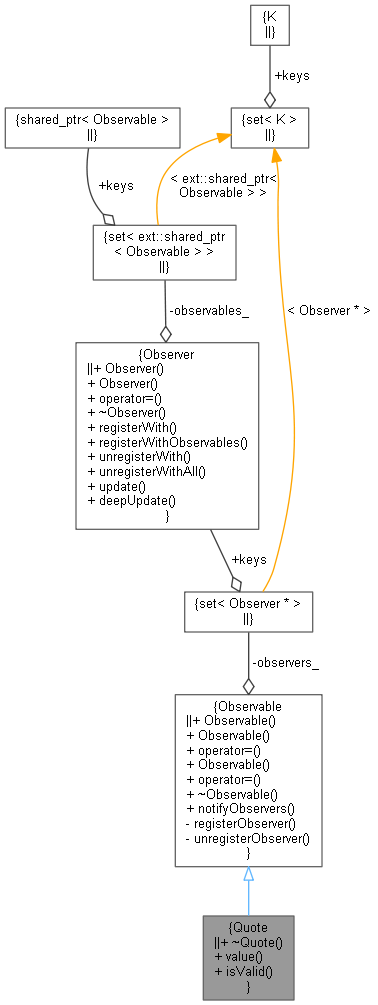

Collaboration diagram for Quote:

Public Member Functions | |

| ~Quote () override=default | |

| virtual Real | value () const =0 |

| returns the current value More... | |

| virtual bool | isValid () const =0 |

| returns true if the Quote holds a valid value More... | |

| Public Member Functions inherited from Observable | |

| Observable ()=default | |

| Observable (const Observable &) | |

| Observable & | operator= (const Observable &) |

| Observable (Observable &&)=delete | |

| Observable & | operator= (Observable &&)=delete |

| virtual | ~Observable ()=default |

| void | notifyObservers () |

Detailed Description

purely virtual base class for market observables

- Tests:

- the observability of class instances is tested.

Constructor & Destructor Documentation

◆ ~Quote()

|

overridedefault |

Member Function Documentation

◆ value()

|

pure virtual |

returns the current value

Implemented in RecoveryRateQuote, DeltaVolQuote, RendistatoEquivalentSwapLengthQuote, RendistatoEquivalentSwapSpreadQuote, CompositeQuote< BinaryFunction >, DerivedQuote< UnaryFunction >, EurodollarFuturesImpliedStdDevQuote, ForwardSwapQuote, ForwardValueQuote, FuturesConvAdjustmentQuote, ImpliedStdDevQuote, LastFixingQuote, and SimpleQuote.

◆ isValid()

|

pure virtual |

returns true if the Quote holds a valid value

Implemented in RecoveryRateQuote, DeltaVolQuote, RendistatoEquivalentSwapLengthQuote, RendistatoEquivalentSwapSpreadQuote, CompositeQuote< BinaryFunction >, DerivedQuote< UnaryFunction >, EurodollarFuturesImpliedStdDevQuote, ForwardSwapQuote, ForwardValueQuote, FuturesConvAdjustmentQuote, ImpliedStdDevQuote, LastFixingQuote, and SimpleQuote.