quote for the futures-convexity adjustment of an index More...

#include <futuresconvadjustmentquote.hpp>

Inheritance diagram for FuturesConvAdjustmentQuote:

Inheritance diagram for FuturesConvAdjustmentQuote: Collaboration diagram for FuturesConvAdjustmentQuote:

Collaboration diagram for FuturesConvAdjustmentQuote:

Public Member Functions | |

| FuturesConvAdjustmentQuote (const ext::shared_ptr< IborIndex > &index, const Date &futuresDate, Handle< Quote > futuresQuote, Handle< Quote > volatility, Handle< Quote > meanReversion) | |

| FuturesConvAdjustmentQuote (const ext::shared_ptr< IborIndex > &index, const std::string &immCode, Handle< Quote > futuresQuote, Handle< Quote > volatility, Handle< Quote > meanReversion) | |

Quote interface | |

| Real | value () const override |

| returns the current value More... | |

| bool | isValid () const override |

| returns true if the Quote holds a valid value More... | |

| void | update () override |

| Public Member Functions inherited from Quote | |

| ~Quote () override=default | |

| virtual Real | value () const =0 |

| returns the current value More... | |

| virtual bool | isValid () const =0 |

| returns true if the Quote holds a valid value More... | |

| Public Member Functions inherited from Observable | |

| Observable ()=default | |

| Observable (const Observable &) | |

| Observable & | operator= (const Observable &) |

| Observable (Observable &&)=delete | |

| Observable & | operator= (Observable &&)=delete |

| virtual | ~Observable ()=default |

| void | notifyObservers () |

| Public Member Functions inherited from Observer | |

| Observer ()=default | |

| Observer (const Observer &) | |

| Observer & | operator= (const Observer &) |

| virtual | ~Observer () |

| std::pair< iterator, bool > | registerWith (const ext::shared_ptr< Observable > &) |

| void | registerWithObservables (const ext::shared_ptr< Observer > &) |

| Size | unregisterWith (const ext::shared_ptr< Observable > &) |

| void | unregisterWithAll () |

| virtual void | update ()=0 |

| virtual void | deepUpdate () |

Inspectors | |

| DayCounter | dc_ |

| const Date | futuresDate_ |

| const Date | indexMaturityDate_ |

| Handle< Quote > | futuresQuote_ |

| Handle< Quote > | volatility_ |

| Handle< Quote > | meanReversion_ |

| Real | rate_ = Null<Real>() |

| Real | futuresValue () const |

| Real | volatility () const |

| Real | meanReversion () const |

| Date | immDate () const |

Additional Inherited Members | |

| Public Types inherited from Observer | |

| typedef set_type::iterator | iterator |

Detailed Description

quote for the futures-convexity adjustment of an index

Definition at line 37 of file futuresconvadjustmentquote.hpp.

Constructor & Destructor Documentation

◆ FuturesConvAdjustmentQuote() [1/2]

| FuturesConvAdjustmentQuote | ( | const ext::shared_ptr< IborIndex > & | index, |

| const Date & | futuresDate, | ||

| Handle< Quote > | futuresQuote, | ||

| Handle< Quote > | volatility, | ||

| Handle< Quote > | meanReversion | ||

| ) |

Definition at line 27 of file futuresconvadjustmentquote.cpp.

Here is the call graph for this function:

◆ FuturesConvAdjustmentQuote() [2/2]

| FuturesConvAdjustmentQuote | ( | const ext::shared_ptr< IborIndex > & | index, |

| const std::string & | immCode, | ||

| Handle< Quote > | futuresQuote, | ||

| Handle< Quote > | volatility, | ||

| Handle< Quote > | meanReversion | ||

| ) |

Definition at line 42 of file futuresconvadjustmentquote.cpp.

Here is the call graph for this function:

Member Function Documentation

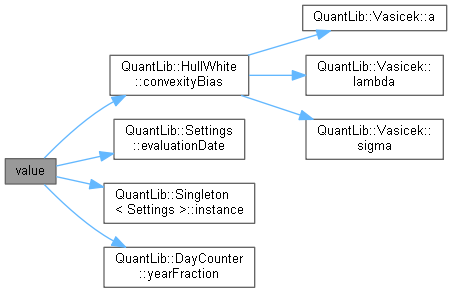

◆ value()

|

overridevirtual |

returns the current value

Implements Quote.

Definition at line 57 of file futuresconvadjustmentquote.cpp.

Here is the call graph for this function:

◆ isValid()

|

overridevirtual |

returns true if the Quote holds a valid value

Implements Quote.

Definition at line 72 of file futuresconvadjustmentquote.cpp.

◆ update()

|

overridevirtual |

This method must be implemented in derived classes. An instance of Observer does not call this method directly: instead, it will be called by the observables the instance registered with when they need to notify any changes.

Implements Observer.

Definition at line 74 of file futuresconvadjustmentquote.hpp.

Here is the call graph for this function:

◆ futuresValue()

| Real futuresValue | ( | ) | const |

Definition at line 58 of file futuresconvadjustmentquote.hpp.

◆ volatility()

| Real volatility | ( | ) | const |

Definition at line 59 of file futuresconvadjustmentquote.hpp.

◆ meanReversion()

| Real meanReversion | ( | ) | const |

Definition at line 60 of file futuresconvadjustmentquote.hpp.

◆ immDate()

| Date immDate | ( | ) | const |

Definition at line 61 of file futuresconvadjustmentquote.hpp.

Member Data Documentation

◆ dc_

|

protected |

Definition at line 64 of file futuresconvadjustmentquote.hpp.

◆ futuresDate_

|

protected |

Definition at line 65 of file futuresconvadjustmentquote.hpp.

◆ indexMaturityDate_

|

protected |

Definition at line 65 of file futuresconvadjustmentquote.hpp.

◆ futuresQuote_

Definition at line 66 of file futuresconvadjustmentquote.hpp.

◆ volatility_

Definition at line 67 of file futuresconvadjustmentquote.hpp.

◆ meanReversion_

Definition at line 68 of file futuresconvadjustmentquote.hpp.

◆ rate_

Definition at line 69 of file futuresconvadjustmentquote.hpp.