set of CMS quotes More...

#include <cmsmarket.hpp>

Inheritance diagram for CmsMarket:

Inheritance diagram for CmsMarket: Collaboration diagram for CmsMarket:

Collaboration diagram for CmsMarket:

Public Member Functions | |

| CmsMarket (std::vector< Period > swapLengths, std::vector< ext::shared_ptr< SwapIndex > > swapIndexes, ext::shared_ptr< IborIndex > iborIndex, const std::vector< std::vector< Handle< Quote > > > &bidAskSpreads, const std::vector< ext::shared_ptr< CmsCouponPricer > > &pricers, Handle< YieldTermStructure > discountingTS) | |

| Public Member Functions inherited from LazyObject | |

| LazyObject () | |

| ~LazyObject () override=default | |

| bool | isCalculated () const |

| void | forwardFirstNotificationOnly () |

| void | alwaysForwardNotifications () |

| void | recalculate () |

| void | freeze () |

| void | unfreeze () |

| Public Member Functions inherited from Observable | |

| Observable ()=default | |

| Observable (const Observable &) | |

| Observable & | operator= (const Observable &) |

| Observable (Observable &&)=delete | |

| Observable & | operator= (Observable &&)=delete |

| virtual | ~Observable ()=default |

| void | notifyObservers () |

| Public Member Functions inherited from Observer | |

| Observer ()=default | |

| Observer (const Observer &) | |

| Observer & | operator= (const Observer &) |

| virtual | ~Observer () |

| std::pair< iterator, bool > | registerWith (const ext::shared_ptr< Observable > &) |

| void | registerWithObservables (const ext::shared_ptr< Observer > &) |

| Size | unregisterWith (const ext::shared_ptr< Observable > &) |

| void | unregisterWithAll () |

| virtual void | update ()=0 |

| virtual void | deepUpdate () |

Additional Inherited Members | |

| Public Types inherited from Observer | |

| typedef set_type::iterator | iterator |

| Protected Member Functions inherited from LazyObject | |

| virtual void | calculate () const |

| Protected Attributes inherited from LazyObject | |

| bool | calculated_ = false |

| bool | frozen_ = false |

| bool | alwaysForward_ |

Detailed Description

set of CMS quotes

Definition at line 42 of file cmsmarket.hpp.

Constructor & Destructor Documentation

◆ CmsMarket()

| CmsMarket | ( | std::vector< Period > | swapLengths, |

| std::vector< ext::shared_ptr< SwapIndex > > | swapIndexes, | ||

| ext::shared_ptr< IborIndex > | iborIndex, | ||

| const std::vector< std::vector< Handle< Quote > > > & | bidAskSpreads, | ||

| const std::vector< ext::shared_ptr< CmsCouponPricer > > & | pricers, | ||

| Handle< YieldTermStructure > | discountingTS | ||

| ) |

Member Function Documentation

◆ update()

|

overridevirtual |

This method must be implemented in derived classes. An instance of Observer does not call this method directly: instead, it will be called by the observables the instance registered with when they need to notify any changes.

Reimplemented from LazyObject.

Definition at line 52 of file cmsmarket.hpp.

Here is the call graph for this function:

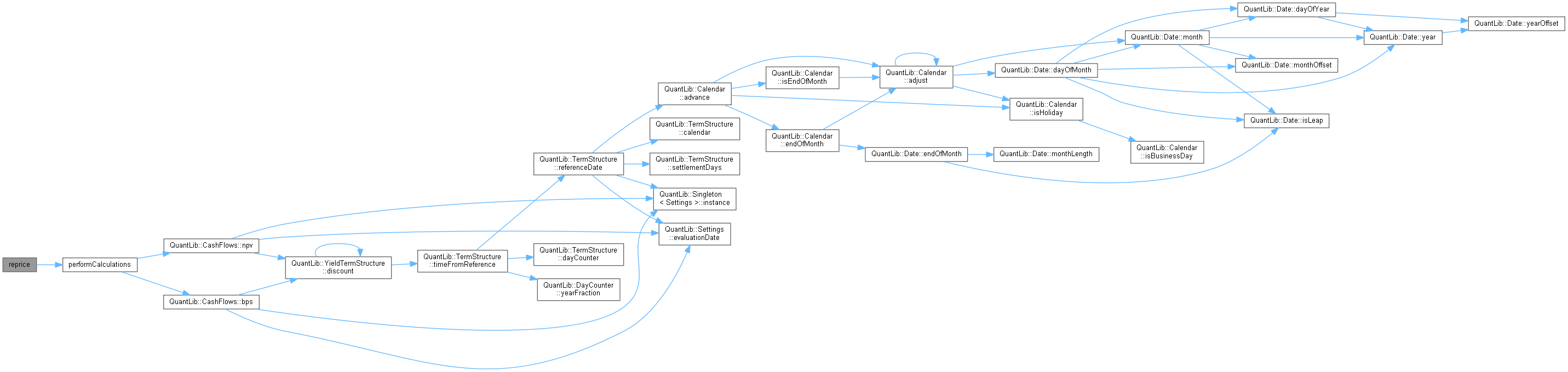

◆ reprice()

| void reprice | ( | const Handle< SwaptionVolatilityStructure > & | volStructure, |

| Real | meanReversion | ||

| ) |

◆ swapTenors()

| const std::vector< Period > & swapTenors | ( | ) | const |

Definition at line 58 of file cmsmarket.hpp.

◆ swapLengths()

| const std::vector< Period > & swapLengths | ( | ) | const |

Definition at line 59 of file cmsmarket.hpp.

◆ impliedCmsSpreads()

| const Matrix & impliedCmsSpreads | ( | ) |

Definition at line 60 of file cmsmarket.hpp.

◆ spreadErrors()

| const Matrix & spreadErrors | ( | ) |

Definition at line 61 of file cmsmarket.hpp.

◆ browse()

| Matrix browse | ( | ) | const |

◆ weightedSpreadError()

◆ weightedSpotNpvError()

◆ weightedFwdNpvError()

◆ weightedSpreadErrors()

◆ weightedSpotNpvErrors()

◆ weightedFwdNpvErrors()

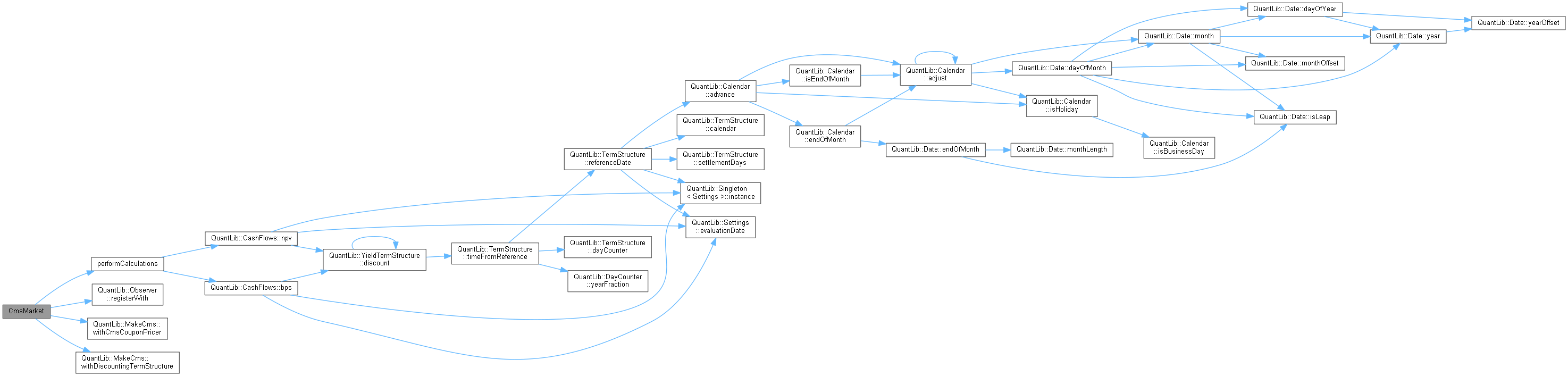

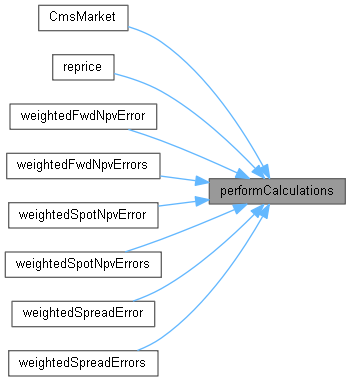

◆ performCalculations()

|

overrideprivatevirtual |

This method must implement any calculations which must be (re)done in order to calculate the desired results.

Implements LazyObject.

Definition at line 108 of file cmsmarket.cpp.

Here is the call graph for this function: Here is the caller graph for this function:

Here is the caller graph for this function:

◆ weightedMean()

◆ weightedMeans()

Member Data Documentation

◆ swapLengths_

|

private |

Definition at line 77 of file cmsmarket.hpp.

◆ swapIndexes_

|

private |

Definition at line 78 of file cmsmarket.hpp.

◆ iborIndex_

|

private |

Definition at line 79 of file cmsmarket.hpp.

◆ bidAskSpreads_

Definition at line 80 of file cmsmarket.hpp.

◆ pricers_

|

private |

Definition at line 81 of file cmsmarket.hpp.

◆ discTS_

|

private |

Definition at line 82 of file cmsmarket.hpp.

◆ nExercise_

|

private |

Definition at line 84 of file cmsmarket.hpp.

◆ nSwapIndexes_

|

private |

Definition at line 85 of file cmsmarket.hpp.

◆ swapTenors_

|

private |

Definition at line 86 of file cmsmarket.hpp.

◆ spotFloatLegNPV_

|

mutableprivate |

Definition at line 87 of file cmsmarket.hpp.

◆ spotFloatLegBPS_

|

private |

Definition at line 87 of file cmsmarket.hpp.

◆ mktBidSpreads_

|

mutableprivate |

Definition at line 90 of file cmsmarket.hpp.

◆ mktAskSpreads_

|

private |

Definition at line 90 of file cmsmarket.hpp.

◆ mktSpreads_

|

private |

Definition at line 90 of file cmsmarket.hpp.

◆ mdlSpreads_

|

mutableprivate |

Definition at line 92 of file cmsmarket.hpp.

◆ errSpreads_

|

mutableprivate |

Definition at line 94 of file cmsmarket.hpp.

◆ mktSpotCmsLegNPV_

|

mutableprivate |

Definition at line 97 of file cmsmarket.hpp.

◆ mdlSpotCmsLegNPV_

|

mutableprivate |

Definition at line 99 of file cmsmarket.hpp.

◆ errSpotCmsLegNPV_

|

mutableprivate |

Definition at line 101 of file cmsmarket.hpp.

◆ mktFwdCmsLegNPV_

|

mutableprivate |

Definition at line 104 of file cmsmarket.hpp.

◆ mdlFwdCmsLegNPV_

|

mutableprivate |

Definition at line 106 of file cmsmarket.hpp.

◆ errFwdCmsLegNPV_

|

mutableprivate |

Definition at line 108 of file cmsmarket.hpp.

◆ spotSwaps_

|

private |

Definition at line 110 of file cmsmarket.hpp.

◆ fwdSwaps_

|

private |

Definition at line 111 of file cmsmarket.hpp.