Swaption-volatility structure More...

#include <swaptionvolstructure.hpp>

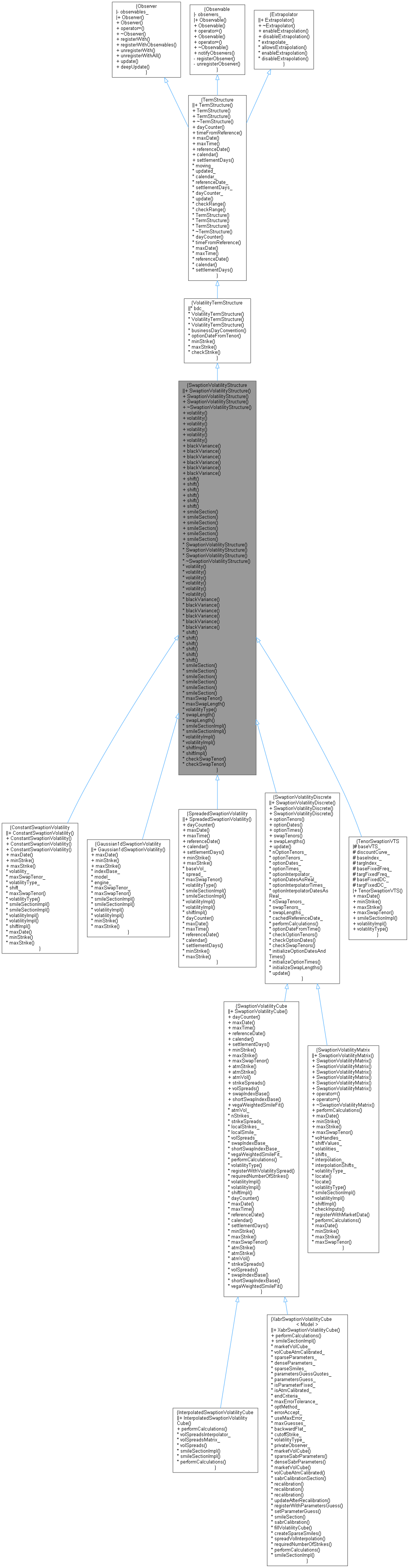

Inheritance diagram for SwaptionVolatilityStructure:

Inheritance diagram for SwaptionVolatilityStructure: Collaboration diagram for SwaptionVolatilityStructure:

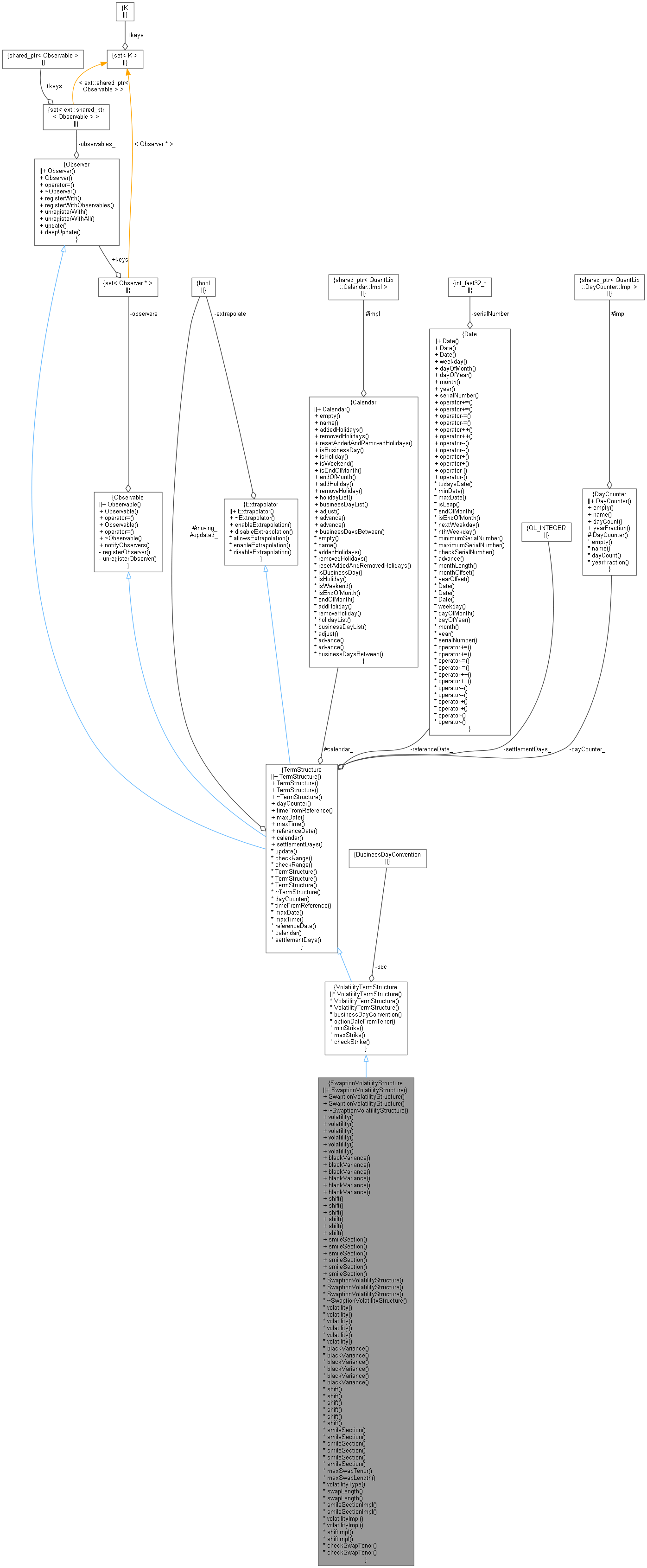

Collaboration diagram for SwaptionVolatilityStructure:

Public Member Functions | |

Constructors | |

See the TermStructure documentation for issues regarding constructors. | |

| SwaptionVolatilityStructure (BusinessDayConvention bdc, const DayCounter &dc=DayCounter()) | |

| SwaptionVolatilityStructure (const Date &referenceDate, const Calendar &calendar, BusinessDayConvention bdc, const DayCounter &dc=DayCounter()) | |

| initialize with a fixed reference date More... | |

| SwaptionVolatilityStructure (Natural settlementDays, const Calendar &, BusinessDayConvention bdc, const DayCounter &dc=DayCounter()) | |

| calculate the reference date based on the global evaluation date More... | |

| ~SwaptionVolatilityStructure () override=default | |

Volatility, variance and smile | |

| Volatility | volatility (const Period &optionTenor, const Period &swapTenor, Rate strike, bool extrapolate=false) const |

| returns the volatility for a given option tenor and swap tenor More... | |

| Volatility | volatility (const Date &optionDate, const Period &swapTenor, Rate strike, bool extrapolate=false) const |

| returns the volatility for a given option date and swap tenor More... | |

| Volatility | volatility (Time optionTime, const Period &swapTenor, Rate strike, bool extrapolate=false) const |

| returns the volatility for a given option time and swap tenor More... | |

| Volatility | volatility (const Period &optionTenor, Time swapLength, Rate strike, bool extrapolate=false) const |

| returns the volatility for a given option tenor and swap length More... | |

| Volatility | volatility (const Date &optionDate, Time swapLength, Rate strike, bool extrapolate=false) const |

| returns the volatility for a given option date and swap length More... | |

| Volatility | volatility (Time optionTime, Time swapLength, Rate strike, bool extrapolate=false) const |

| returns the volatility for a given option time and swap length More... | |

| Real | blackVariance (const Period &optionTenor, const Period &swapTenor, Rate strike, bool extrapolate=false) const |

| returns the Black variance for a given option tenor and swap tenor More... | |

| Real | blackVariance (const Date &optionDate, const Period &swapTenor, Rate strike, bool extrapolate=false) const |

| returns the Black variance for a given option date and swap tenor More... | |

| Real | blackVariance (Time optionTime, const Period &swapTenor, Rate strike, bool extrapolate=false) const |

| returns the Black variance for a given option time and swap tenor More... | |

| Real | blackVariance (const Period &optionTenor, Time swapLength, Rate strike, bool extrapolate=false) const |

| returns the Black variance for a given option tenor and swap length More... | |

| Real | blackVariance (const Date &optionDate, Time swapLength, Rate strike, bool extrapolate=false) const |

| returns the Black variance for a given option date and swap length More... | |

| Real | blackVariance (Time optionTime, Time swapLength, Rate strike, bool extrapolate=false) const |

| returns the Black variance for a given option time and swap length More... | |

| Real | shift (const Period &optionTenor, const Period &swapTenor, bool extrapolate=false) const |

| returns the shift for a given option tenor and swap tenor More... | |

| Real | shift (const Date &optionDate, const Period &swapTenor, bool extrapolate=false) const |

| returns the shift for a given option date and swap tenor More... | |

| Real | shift (Time optionTime, const Period &swapTenor, bool extrapolate=false) const |

| returns the shift for a given option time and swap tenor More... | |

| Real | shift (const Period &optionTenor, Time swapLength, bool extrapolate=false) const |

| returns the shift for a given option tenor and swap length More... | |

| Real | shift (const Date &optionDate, Time swapLength, bool extrapolate=false) const |

| returns the shift for a given option date and swap length More... | |

| Real | shift (Time optionTime, Time swapLength, bool extrapolate=false) const |

| returns the shift for a given option time and swap length More... | |

| ext::shared_ptr< SmileSection > | smileSection (const Period &optionTenor, const Period &swapTenor, bool extr=false) const |

| returns the smile for a given option tenor and swap tenor More... | |

| ext::shared_ptr< SmileSection > | smileSection (const Date &optionDate, const Period &swapTenor, bool extr=false) const |

| returns the smile for a given option date and swap tenor More... | |

| ext::shared_ptr< SmileSection > | smileSection (Time optionTime, const Period &swapTenor, bool extr=false) const |

| returns the smile for a given option time and swap tenor More... | |

| ext::shared_ptr< SmileSection > | smileSection (const Period &optionTenor, Time swapLength, bool extr=false) const |

| returns the smile for a given option tenor and swap length More... | |

| ext::shared_ptr< SmileSection > | smileSection (const Date &optionDate, Time swapLength, bool extr=false) const |

| returns the smile for a given option date and swap length More... | |

| ext::shared_ptr< SmileSection > | smileSection (Time optionTime, Time swapLength, bool extr=false) const |

| returns the smile for a given option time and swap length More... | |

| Public Member Functions inherited from VolatilityTermStructure | |

| VolatilityTermStructure (BusinessDayConvention bdc, const DayCounter &dc=DayCounter()) | |

| VolatilityTermStructure (const Date &referenceDate, const Calendar &cal, BusinessDayConvention bdc, const DayCounter &dc=DayCounter()) | |

| initialize with a fixed reference date More... | |

| VolatilityTermStructure (Natural settlementDays, const Calendar &cal, BusinessDayConvention bdc, const DayCounter &dc=DayCounter()) | |

| calculate the reference date based on the global evaluation date More... | |

| virtual BusinessDayConvention | businessDayConvention () const |

| the business day convention used in tenor to date conversion More... | |

| Date | optionDateFromTenor (const Period &) const |

| period/date conversion More... | |

| virtual Rate | minStrike () const =0 |

| the minimum strike for which the term structure can return vols More... | |

| virtual Rate | maxStrike () const =0 |

| the maximum strike for which the term structure can return vols More... | |

| Public Member Functions inherited from TermStructure | |

| TermStructure (DayCounter dc=DayCounter()) | |

| default constructor More... | |

| TermStructure (const Date &referenceDate, Calendar calendar=Calendar(), DayCounter dc=DayCounter()) | |

| initialize with a fixed reference date More... | |

| TermStructure (Natural settlementDays, Calendar, DayCounter dc=DayCounter()) | |

| calculate the reference date based on the global evaluation date More... | |

| ~TermStructure () override=default | |

| virtual DayCounter | dayCounter () const |

| the day counter used for date/time conversion More... | |

| Time | timeFromReference (const Date &date) const |

| date/time conversion More... | |

| virtual Date | maxDate () const =0 |

| the latest date for which the curve can return values More... | |

| virtual Time | maxTime () const |

| the latest time for which the curve can return values More... | |

| virtual const Date & | referenceDate () const |

| the date at which discount = 1.0 and/or variance = 0.0 More... | |

| virtual Calendar | calendar () const |

| the calendar used for reference and/or option date calculation More... | |

| virtual Natural | settlementDays () const |

| the settlementDays used for reference date calculation More... | |

| void | update () override |

| Public Member Functions inherited from Observer | |

| Observer ()=default | |

| Observer (const Observer &) | |

| Observer & | operator= (const Observer &) |

| virtual | ~Observer () |

| std::pair< iterator, bool > | registerWith (const ext::shared_ptr< Observable > &) |

| void | registerWithObservables (const ext::shared_ptr< Observer > &) |

| Size | unregisterWith (const ext::shared_ptr< Observable > &) |

| void | unregisterWithAll () |

| virtual void | update ()=0 |

| virtual void | deepUpdate () |

| Public Member Functions inherited from Observable | |

| Observable ()=default | |

| Observable (const Observable &) | |

| Observable & | operator= (const Observable &) |

| Observable (Observable &&)=delete | |

| Observable & | operator= (Observable &&)=delete |

| virtual | ~Observable ()=default |

| void | notifyObservers () |

| Public Member Functions inherited from Extrapolator | |

| Extrapolator ()=default | |

| virtual | ~Extrapolator ()=default |

| void | enableExtrapolation (bool b=true) |

| enable extrapolation in subsequent calls More... | |

| void | disableExtrapolation (bool b=true) |

| disable extrapolation in subsequent calls More... | |

| bool | allowsExtrapolation () const |

| tells whether extrapolation is enabled More... | |

Limits | |

| virtual const Period & | maxSwapTenor () const =0 |

| the largest length for which the term structure can return vols More... | |

| Time | maxSwapLength () const |

| the largest swapLength for which the term structure can return vols More... | |

| virtual VolatilityType | volatilityType () const |

| volatility type More... | |

| Time | swapLength (const Period &swapTenor) const |

| implements the conversion between swap tenor and swap (time) length More... | |

| Time | swapLength (const Date &start, const Date &end) const |

| implements the conversion between swap dates and swap (time) length More... | |

| virtual ext::shared_ptr< SmileSection > | smileSectionImpl (const Date &optionDate, const Period &swapTenor) const |

| virtual ext::shared_ptr< SmileSection > | smileSectionImpl (Time optionTime, Time swapLength) const =0 |

| virtual Volatility | volatilityImpl (const Date &optionDate, const Period &swapTenor, Rate strike) const |

| virtual Volatility | volatilityImpl (Time optionTime, Time swapLength, Rate strike) const =0 |

| virtual Real | shiftImpl (const Date &optionDate, const Period &swapTenor) const |

| virtual Real | shiftImpl (Time optionTime, Time swapLength) const |

| void | checkSwapTenor (const Period &swapTenor, bool extrapolate) const |

| void | checkSwapTenor (Time swapLength, bool extrapolate) const |

Additional Inherited Members | |

| Public Types inherited from Observer | |

| typedef set_type::iterator | iterator |

| Protected Member Functions inherited from VolatilityTermStructure | |

| void | checkStrike (Rate strike, bool extrapolate) const |

| strike-range check More... | |

| Protected Member Functions inherited from TermStructure | |

| void | checkRange (const Date &d, bool extrapolate) const |

| date-range check More... | |

| void | checkRange (Time t, bool extrapolate) const |

| time-range check More... | |

| Protected Attributes inherited from TermStructure | |

| bool | moving_ = false |

| bool | updated_ = true |

| Calendar | calendar_ |

Detailed Description

Swaption-volatility structure

This abstract class defines the interface of concrete swaption volatility structures which will be derived from this one.

Definition at line 41 of file swaptionvolstructure.hpp.

Constructor & Destructor Documentation

◆ SwaptionVolatilityStructure() [1/3]

| SwaptionVolatilityStructure | ( | BusinessDayConvention | bdc, |

| const DayCounter & | dc = DayCounter() |

||

| ) |

- Warning:

- term structures initialized by means of this constructor must manage their own reference date by overriding the referenceDate() method.

Definition at line 27 of file swaptionvolstructure.cpp.

◆ SwaptionVolatilityStructure() [2/3]

| SwaptionVolatilityStructure | ( | const Date & | referenceDate, |

| const Calendar & | calendar, | ||

| BusinessDayConvention | bdc, | ||

| const DayCounter & | dc = DayCounter() |

||

| ) |

initialize with a fixed reference date

Definition at line 32 of file swaptionvolstructure.cpp.

◆ SwaptionVolatilityStructure() [3/3]

| SwaptionVolatilityStructure | ( | Natural | settlementDays, |

| const Calendar & | calendar, | ||

| BusinessDayConvention | bdc, | ||

| const DayCounter & | dc = DayCounter() |

||

| ) |

calculate the reference date based on the global evaluation date

Definition at line 39 of file swaptionvolstructure.cpp.

◆ ~SwaptionVolatilityStructure()

|

overridedefault |

Member Function Documentation

◆ volatility() [1/6]

| Volatility volatility | ( | const Period & | optionTenor, |

| const Period & | swapTenor, | ||

| Rate | strike, | ||

| bool | extrapolate = false |

||

| ) | const |

returns the volatility for a given option tenor and swap tenor

Definition at line 225 of file swaptionvolstructure.hpp.

Here is the call graph for this function: Here is the caller graph for this function:

Here is the caller graph for this function:

◆ volatility() [2/6]

| Volatility volatility | ( | const Date & | optionDate, |

| const Period & | swapTenor, | ||

| Rate | strike, | ||

| bool | extrapolate = false |

||

| ) | const |

returns the volatility for a given option date and swap tenor

Definition at line 325 of file swaptionvolstructure.hpp.

Here is the call graph for this function:

◆ volatility() [3/6]

| Volatility volatility | ( | Time | optionTime, |

| const Period & | swapTenor, | ||

| Rate | strike, | ||

| bool | extrapolate = false |

||

| ) | const |

returns the volatility for a given option time and swap tenor

Definition at line 348 of file swaptionvolstructure.hpp.

Here is the call graph for this function:

◆ volatility() [4/6]

| Volatility volatility | ( | const Period & | optionTenor, |

| Time | swapLength, | ||

| Rate | strike, | ||

| bool | extrapolate = false |

||

| ) | const |

returns the volatility for a given option tenor and swap length

Definition at line 234 of file swaptionvolstructure.hpp.

Here is the call graph for this function:

◆ volatility() [5/6]

| Volatility volatility | ( | const Date & | optionDate, |

| Time | swapLength, | ||

| Rate | strike, | ||

| bool | extrapolate = false |

||

| ) | const |

returns the volatility for a given option date and swap length

Definition at line 336 of file swaptionvolstructure.hpp.

Here is the call graph for this function:

◆ volatility() [6/6]

| Volatility volatility | ( | Time | optionTime, |

| Time | swapLength, | ||

| Rate | strike, | ||

| bool | extrapolate = false |

||

| ) | const |

returns the volatility for a given option time and swap length

Definition at line 360 of file swaptionvolstructure.hpp.

Here is the call graph for this function:

◆ blackVariance() [1/6]

| Real blackVariance | ( | const Period & | optionTenor, |

| const Period & | swapTenor, | ||

| Rate | strike, | ||

| bool | extrapolate = false |

||

| ) | const |

returns the Black variance for a given option tenor and swap tenor

Definition at line 243 of file swaptionvolstructure.hpp.

Here is the call graph for this function: Here is the caller graph for this function:

Here is the caller graph for this function:

◆ blackVariance() [2/6]

| Real blackVariance | ( | const Date & | optionDate, |

| const Period & | swapTenor, | ||

| Rate | strike, | ||

| bool | extrapolate = false |

||

| ) | const |

returns the Black variance for a given option date and swap tenor

Definition at line 286 of file swaptionvolstructure.hpp.

Here is the call graph for this function:

◆ blackVariance() [3/6]

| Real blackVariance | ( | Time | optionTime, |

| const Period & | swapTenor, | ||

| Rate | strike, | ||

| bool | extrapolate = false |

||

| ) | const |

returns the Black variance for a given option time and swap tenor

Definition at line 296 of file swaptionvolstructure.hpp.

Here is the call graph for this function:

◆ blackVariance() [4/6]

| Real blackVariance | ( | const Period & | optionTenor, |

| Time | swapLength, | ||

| Rate | strike, | ||

| bool | extrapolate = false |

||

| ) | const |

returns the Black variance for a given option tenor and swap length

Definition at line 252 of file swaptionvolstructure.hpp.

Here is the call graph for this function:

◆ blackVariance() [5/6]

| Real blackVariance | ( | const Date & | optionDate, |

| Time | swapLength, | ||

| Rate | strike, | ||

| bool | extrapolate = false |

||

| ) | const |

returns the Black variance for a given option date and swap length

Definition at line 305 of file swaptionvolstructure.hpp.

Here is the call graph for this function:

◆ blackVariance() [6/6]

| Real blackVariance | ( | Time | optionTime, |

| Time | swapLength, | ||

| Rate | strike, | ||

| bool | extrapolate = false |

||

| ) | const |

returns the Black variance for a given option time and swap length

Definition at line 315 of file swaptionvolstructure.hpp.

Here is the call graph for this function:

◆ shift() [1/6]

returns the shift for a given option tenor and swap tenor

Definition at line 261 of file swaptionvolstructure.hpp.

Here is the call graph for this function: Here is the caller graph for this function:

Here is the caller graph for this function:

◆ shift() [2/6]

returns the shift for a given option date and swap tenor

Definition at line 371 of file swaptionvolstructure.hpp.

Here is the call graph for this function:

◆ shift() [3/6]

returns the shift for a given option time and swap tenor

Definition at line 390 of file swaptionvolstructure.hpp.

Here is the call graph for this function:

◆ shift() [4/6]

returns the shift for a given option tenor and swap length

Definition at line 269 of file swaptionvolstructure.hpp.

Here is the call graph for this function:

◆ shift() [5/6]

returns the shift for a given option date and swap length

Definition at line 380 of file swaptionvolstructure.hpp.

Here is the call graph for this function:

◆ shift() [6/6]

returns the shift for a given option time and swap length

Definition at line 400 of file swaptionvolstructure.hpp.

Here is the call graph for this function:

◆ smileSection() [1/6]

| ext::shared_ptr< SmileSection > smileSection | ( | const Period & | optionTenor, |

| const Period & | swapTenor, | ||

| bool | extr = false |

||

| ) | const |

returns the smile for a given option tenor and swap tenor

Definition at line 277 of file swaptionvolstructure.hpp.

Here is the call graph for this function: Here is the caller graph for this function:

Here is the caller graph for this function:

◆ smileSection() [2/6]

| ext::shared_ptr< SmileSection > smileSection | ( | const Date & | optionDate, |

| const Period & | swapTenor, | ||

| bool | extr = false |

||

| ) | const |

returns the smile for a given option date and swap tenor

Definition at line 409 of file swaptionvolstructure.hpp.

Here is the call graph for this function:

◆ smileSection() [3/6]

| ext::shared_ptr< SmileSection > smileSection | ( | Time | optionTime, |

| const Period & | swapTenor, | ||

| bool | extr = false |

||

| ) | const |

returns the smile for a given option time and swap tenor

Definition at line 418 of file swaptionvolstructure.hpp.

Here is the call graph for this function:

◆ smileSection() [4/6]

| ext::shared_ptr< SmileSection > smileSection | ( | const Period & | optionTenor, |

| Time | swapLength, | ||

| bool | extr = false |

||

| ) | const |

returns the smile for a given option tenor and swap length

Definition at line 427 of file swaptionvolstructure.hpp.

Here is the call graph for this function:

◆ smileSection() [5/6]

| ext::shared_ptr< SmileSection > smileSection | ( | const Date & | optionDate, |

| Time | swapLength, | ||

| bool | extr = false |

||

| ) | const |

returns the smile for a given option date and swap length

Definition at line 437 of file swaptionvolstructure.hpp.

Here is the call graph for this function:

◆ smileSection() [6/6]

| ext::shared_ptr< SmileSection > smileSection | ( | Time | optionTime, |

| Time | swapLength, | ||

| bool | extr = false |

||

| ) | const |

returns the smile for a given option time and swap length

Definition at line 446 of file swaptionvolstructure.hpp.

Here is the call graph for this function:

◆ maxSwapTenor()

|

pure virtual |

the largest length for which the term structure can return vols

Implemented in TenorSwaptionVTS, Gaussian1dSwaptionVolatility, SpreadedSwaptionVolatility, ConstantSwaptionVolatility, SwaptionVolatilityCube, and SwaptionVolatilityMatrix.

Here is the caller graph for this function:

◆ maxSwapLength()

| Time maxSwapLength | ( | ) | const |

the largest swapLength for which the term structure can return vols

Definition at line 485 of file swaptionvolstructure.hpp.

Here is the call graph for this function: Here is the caller graph for this function:

Here is the caller graph for this function:

◆ volatilityType()

|

virtual |

volatility type

Reimplemented in TenorSwaptionVTS, SpreadedSwaptionVolatility, ConstantSwaptionVolatility, SwaptionVolatilityCube, and SwaptionVolatilityMatrix.

Definition at line 189 of file swaptionvolstructure.hpp.

Here is the caller graph for this function:

◆ swapLength() [1/2]

implements the conversion between swap tenor and swap (time) length

Definition at line 47 of file swaptionvolstructure.cpp.

Here is the call graph for this function: Here is the caller graph for this function:

Here is the caller graph for this function:

◆ swapLength() [2/2]

implements the conversion between swap dates and swap (time) length

Definition at line 60 of file swaptionvolstructure.cpp.

◆ smileSectionImpl() [1/2]

|

protectedvirtual |

Reimplemented in Gaussian1dSwaptionVolatility, ConstantSwaptionVolatility, InterpolatedSwaptionVolatilityCube, and SpreadedSwaptionVolatility.

Definition at line 457 of file swaptionvolstructure.hpp.

Here is the call graph for this function: Here is the caller graph for this function:

Here is the caller graph for this function:

◆ smileSectionImpl() [2/2]

|

protectedpure virtual |

◆ volatilityImpl() [1/2]

|

protectedvirtual |

Reimplemented in Gaussian1dSwaptionVolatility, ConstantSwaptionVolatility, SpreadedSwaptionVolatility, and SwaptionVolatilityCube.

Definition at line 464 of file swaptionvolstructure.hpp.

Here is the call graph for this function: Here is the caller graph for this function:

Here is the caller graph for this function:

◆ volatilityImpl() [2/2]

|

protectedpure virtual |

◆ shiftImpl() [1/2]

Definition at line 473 of file swaptionvolstructure.hpp.

Here is the call graph for this function: Here is the caller graph for this function:

Here is the caller graph for this function:

◆ shiftImpl() [2/2]

Reimplemented in SpreadedSwaptionVolatility, ConstantSwaptionVolatility, SwaptionVolatilityCube, and SwaptionVolatilityMatrix.

Definition at line 478 of file swaptionvolstructure.hpp.

Here is the call graph for this function:

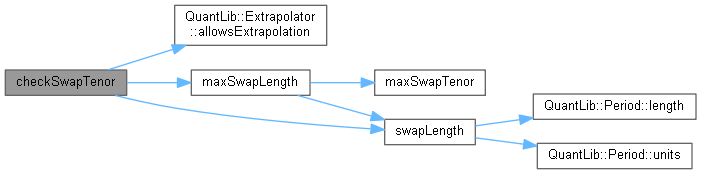

◆ checkSwapTenor() [1/2]

Definition at line 70 of file swaptionvolstructure.cpp.

Here is the call graph for this function: Here is the caller graph for this function:

Here is the caller graph for this function: