At-the-money swaption-volatility matrix. More...

#include <swaptionvolmatrix.hpp>

Inheritance diagram for SwaptionVolatilityMatrix:

Inheritance diagram for SwaptionVolatilityMatrix: Collaboration diagram for SwaptionVolatilityMatrix:

Collaboration diagram for SwaptionVolatilityMatrix:

Public Member Functions | |

| SwaptionVolatilityMatrix (const Calendar &calendar, BusinessDayConvention bdc, const std::vector< Period > &optionTenors, const std::vector< Period > &swapTenors, const std::vector< std::vector< Handle< Quote > > > &vols, const DayCounter &dayCounter, bool flatExtrapolation=false, VolatilityType type=ShiftedLognormal, const std::vector< std::vector< Real > > &shifts=std::vector< std::vector< Real > >()) | |

| floating reference date, floating market data More... | |

| SwaptionVolatilityMatrix (const Date &referenceDate, const Calendar &calendar, BusinessDayConvention bdc, const std::vector< Period > &optionTenors, const std::vector< Period > &swapTenors, const std::vector< std::vector< Handle< Quote > > > &vols, const DayCounter &dayCounter, bool flatExtrapolation=false, VolatilityType type=ShiftedLognormal, const std::vector< std::vector< Real > > &shifts=std::vector< std::vector< Real > >()) | |

| fixed reference date, floating market data More... | |

| SwaptionVolatilityMatrix (const Calendar &calendar, BusinessDayConvention bdc, const std::vector< Period > &optionTenors, const std::vector< Period > &swapTenors, const Matrix &volatilities, const DayCounter &dayCounter, bool flatExtrapolation=false, VolatilityType type=ShiftedLognormal, const Matrix &shifts=Matrix()) | |

| floating reference date, fixed market data More... | |

| SwaptionVolatilityMatrix (const Date &referenceDate, const Calendar &calendar, BusinessDayConvention bdc, const std::vector< Period > &optionTenors, const std::vector< Period > &swapTenors, const Matrix &volatilities, const DayCounter &dayCounter, bool flatExtrapolation=false, VolatilityType type=ShiftedLognormal, const Matrix &shifts=Matrix()) | |

| fixed reference date, fixed market data More... | |

| SwaptionVolatilityMatrix (const Date &referenceDate, const Calendar &calendar, BusinessDayConvention bdc, const std::vector< Date > &optionDates, const std::vector< Period > &swapTenors, const Matrix &volatilities, const DayCounter &dayCounter, bool flatExtrapolation=false, VolatilityType type=ShiftedLognormal, const Matrix &shifts=Matrix()) | |

| fixed reference date and fixed market data, option dates More... | |

| SwaptionVolatilityMatrix (SwaptionVolatilityMatrix &&)=delete | |

| SwaptionVolatilityMatrix (const SwaptionVolatilityMatrix &)=delete | |

| SwaptionVolatilityMatrix & | operator= (SwaptionVolatilityMatrix &&)=delete |

| SwaptionVolatilityMatrix & | operator= (const SwaptionVolatilityMatrix &)=delete |

| ~SwaptionVolatilityMatrix () override=default | |

LazyObject interface | |

| void | performCalculations () const override |

TermStructure interface | |

| Date | maxDate () const override |

| the latest date for which the curve can return values More... | |

VolatilityTermStructure interface | |

| Rate | minStrike () const override |

| the minimum strike for which the term structure can return vols More... | |

| Rate | maxStrike () const override |

| the maximum strike for which the term structure can return vols More... | |

SwaptionVolatilityStructure interface | |

| const Period & | maxSwapTenor () const override |

| the largest length for which the term structure can return vols More... | |

| Public Member Functions inherited from SwaptionVolatilityDiscrete | |

| SwaptionVolatilityDiscrete (const std::vector< Period > &optionTenors, const std::vector< Period > &swapTenors, Natural settlementDays, const Calendar &cal, BusinessDayConvention bdc, const DayCounter &dc) | |

| SwaptionVolatilityDiscrete (const std::vector< Period > &optionTenors, const std::vector< Period > &swapTenors, const Date &referenceDate, const Calendar &cal, BusinessDayConvention bdc, const DayCounter &dc) | |

| SwaptionVolatilityDiscrete (const std::vector< Date > &optionDates, const std::vector< Period > &swapTenors, const Date &referenceDate, const Calendar &cal, BusinessDayConvention bdc, const DayCounter &dc) | |

| const std::vector< Period > & | optionTenors () const |

| const std::vector< Date > & | optionDates () const |

| const std::vector< Time > & | optionTimes () const |

| const std::vector< Period > & | swapTenors () const |

| const std::vector< Time > & | swapLengths () const |

| void | update () override |

| Date | optionDateFromTime (Time optionTime) const |

| additional inspectors More... | |

| Public Member Functions inherited from LazyObject | |

| LazyObject () | |

| ~LazyObject () override=default | |

| bool | isCalculated () const |

| void | forwardFirstNotificationOnly () |

| void | alwaysForwardNotifications () |

| void | recalculate () |

| void | freeze () |

| void | unfreeze () |

| Public Member Functions inherited from Observable | |

| Observable ()=default | |

| Observable (const Observable &) | |

| Observable & | operator= (const Observable &) |

| Observable (Observable &&)=delete | |

| Observable & | operator= (Observable &&)=delete |

| virtual | ~Observable ()=default |

| void | notifyObservers () |

| Public Member Functions inherited from Observer | |

| Observer ()=default | |

| Observer (const Observer &) | |

| Observer & | operator= (const Observer &) |

| virtual | ~Observer () |

| std::pair< iterator, bool > | registerWith (const ext::shared_ptr< Observable > &) |

| void | registerWithObservables (const ext::shared_ptr< Observer > &) |

| Size | unregisterWith (const ext::shared_ptr< Observable > &) |

| void | unregisterWithAll () |

| virtual void | update ()=0 |

| virtual void | deepUpdate () |

| Public Member Functions inherited from SwaptionVolatilityStructure | |

| SwaptionVolatilityStructure (BusinessDayConvention bdc, const DayCounter &dc=DayCounter()) | |

| SwaptionVolatilityStructure (const Date &referenceDate, const Calendar &calendar, BusinessDayConvention bdc, const DayCounter &dc=DayCounter()) | |

| initialize with a fixed reference date More... | |

| SwaptionVolatilityStructure (Natural settlementDays, const Calendar &, BusinessDayConvention bdc, const DayCounter &dc=DayCounter()) | |

| calculate the reference date based on the global evaluation date More... | |

| ~SwaptionVolatilityStructure () override=default | |

| Volatility | volatility (const Period &optionTenor, const Period &swapTenor, Rate strike, bool extrapolate=false) const |

| returns the volatility for a given option tenor and swap tenor More... | |

| Volatility | volatility (const Date &optionDate, const Period &swapTenor, Rate strike, bool extrapolate=false) const |

| returns the volatility for a given option date and swap tenor More... | |

| Volatility | volatility (Time optionTime, const Period &swapTenor, Rate strike, bool extrapolate=false) const |

| returns the volatility for a given option time and swap tenor More... | |

| Volatility | volatility (const Period &optionTenor, Time swapLength, Rate strike, bool extrapolate=false) const |

| returns the volatility for a given option tenor and swap length More... | |

| Volatility | volatility (const Date &optionDate, Time swapLength, Rate strike, bool extrapolate=false) const |

| returns the volatility for a given option date and swap length More... | |

| Volatility | volatility (Time optionTime, Time swapLength, Rate strike, bool extrapolate=false) const |

| returns the volatility for a given option time and swap length More... | |

| Real | blackVariance (const Period &optionTenor, const Period &swapTenor, Rate strike, bool extrapolate=false) const |

| returns the Black variance for a given option tenor and swap tenor More... | |

| Real | blackVariance (const Date &optionDate, const Period &swapTenor, Rate strike, bool extrapolate=false) const |

| returns the Black variance for a given option date and swap tenor More... | |

| Real | blackVariance (Time optionTime, const Period &swapTenor, Rate strike, bool extrapolate=false) const |

| returns the Black variance for a given option time and swap tenor More... | |

| Real | blackVariance (const Period &optionTenor, Time swapLength, Rate strike, bool extrapolate=false) const |

| returns the Black variance for a given option tenor and swap length More... | |

| Real | blackVariance (const Date &optionDate, Time swapLength, Rate strike, bool extrapolate=false) const |

| returns the Black variance for a given option date and swap length More... | |

| Real | blackVariance (Time optionTime, Time swapLength, Rate strike, bool extrapolate=false) const |

| returns the Black variance for a given option time and swap length More... | |

| Real | shift (const Period &optionTenor, const Period &swapTenor, bool extrapolate=false) const |

| returns the shift for a given option tenor and swap tenor More... | |

| Real | shift (const Date &optionDate, const Period &swapTenor, bool extrapolate=false) const |

| returns the shift for a given option date and swap tenor More... | |

| Real | shift (Time optionTime, const Period &swapTenor, bool extrapolate=false) const |

| returns the shift for a given option time and swap tenor More... | |

| Real | shift (const Period &optionTenor, Time swapLength, bool extrapolate=false) const |

| returns the shift for a given option tenor and swap length More... | |

| Real | shift (const Date &optionDate, Time swapLength, bool extrapolate=false) const |

| returns the shift for a given option date and swap length More... | |

| Real | shift (Time optionTime, Time swapLength, bool extrapolate=false) const |

| returns the shift for a given option time and swap length More... | |

| ext::shared_ptr< SmileSection > | smileSection (const Period &optionTenor, const Period &swapTenor, bool extr=false) const |

| returns the smile for a given option tenor and swap tenor More... | |

| ext::shared_ptr< SmileSection > | smileSection (const Date &optionDate, const Period &swapTenor, bool extr=false) const |

| returns the smile for a given option date and swap tenor More... | |

| ext::shared_ptr< SmileSection > | smileSection (Time optionTime, const Period &swapTenor, bool extr=false) const |

| returns the smile for a given option time and swap tenor More... | |

| ext::shared_ptr< SmileSection > | smileSection (const Period &optionTenor, Time swapLength, bool extr=false) const |

| returns the smile for a given option tenor and swap length More... | |

| ext::shared_ptr< SmileSection > | smileSection (const Date &optionDate, Time swapLength, bool extr=false) const |

| returns the smile for a given option date and swap length More... | |

| ext::shared_ptr< SmileSection > | smileSection (Time optionTime, Time swapLength, bool extr=false) const |

| returns the smile for a given option time and swap length More... | |

| Time | maxSwapLength () const |

| the largest swapLength for which the term structure can return vols More... | |

| Time | swapLength (const Period &swapTenor) const |

| implements the conversion between swap tenor and swap (time) length More... | |

| Time | swapLength (const Date &start, const Date &end) const |

| implements the conversion between swap dates and swap (time) length More... | |

| Public Member Functions inherited from VolatilityTermStructure | |

| VolatilityTermStructure (BusinessDayConvention bdc, const DayCounter &dc=DayCounter()) | |

| VolatilityTermStructure (const Date &referenceDate, const Calendar &cal, BusinessDayConvention bdc, const DayCounter &dc=DayCounter()) | |

| initialize with a fixed reference date More... | |

| VolatilityTermStructure (Natural settlementDays, const Calendar &cal, BusinessDayConvention bdc, const DayCounter &dc=DayCounter()) | |

| calculate the reference date based on the global evaluation date More... | |

| virtual BusinessDayConvention | businessDayConvention () const |

| the business day convention used in tenor to date conversion More... | |

| Date | optionDateFromTenor (const Period &) const |

| period/date conversion More... | |

| Public Member Functions inherited from TermStructure | |

| TermStructure (DayCounter dc=DayCounter()) | |

| default constructor More... | |

| TermStructure (const Date &referenceDate, Calendar calendar=Calendar(), DayCounter dc=DayCounter()) | |

| initialize with a fixed reference date More... | |

| TermStructure (Natural settlementDays, Calendar, DayCounter dc=DayCounter()) | |

| calculate the reference date based on the global evaluation date More... | |

| ~TermStructure () override=default | |

| virtual DayCounter | dayCounter () const |

| the day counter used for date/time conversion More... | |

| Time | timeFromReference (const Date &date) const |

| date/time conversion More... | |

| virtual Time | maxTime () const |

| the latest time for which the curve can return values More... | |

| virtual const Date & | referenceDate () const |

| the date at which discount = 1.0 and/or variance = 0.0 More... | |

| virtual Calendar | calendar () const |

| the calendar used for reference and/or option date calculation More... | |

| virtual Natural | settlementDays () const |

| the settlementDays used for reference date calculation More... | |

| Public Member Functions inherited from Extrapolator | |

| Extrapolator ()=default | |

| virtual | ~Extrapolator ()=default |

| void | enableExtrapolation (bool b=true) |

| enable extrapolation in subsequent calls More... | |

| void | disableExtrapolation (bool b=true) |

| disable extrapolation in subsequent calls More... | |

| bool | allowsExtrapolation () const |

| tells whether extrapolation is enabled More... | |

Other inspectors | |

| std::vector< std::vector< Handle< Quote > > > | volHandles_ |

| std::vector< std::vector< Real > > | shiftValues_ |

| Matrix | volatilities_ |

| Matrix | shifts_ |

| Interpolation2D | interpolation_ |

| Interpolation2D | interpolationShifts_ |

| VolatilityType | volatilityType_ |

| std::pair< Size, Size > | locate (const Date &optionDate, const Period &swapTenor) const |

| returns the lower indexes of surrounding volatility matrix corners More... | |

| std::pair< Size, Size > | locate (Time optionTime, Time swapLength) const |

| returns the lower indexes of surrounding volatility matrix corners More... | |

| VolatilityType | volatilityType () const override |

| volatility type More... | |

| ext::shared_ptr< SmileSection > | smileSectionImpl (Time, Time) const override |

| Volatility | volatilityImpl (Time optionTime, Time swapLength, Rate strike) const override |

| Real | shiftImpl (Time optionTime, Time swapLength) const override |

| void | checkInputs (Size volRows, Size volsColumns, Size shiftRows, Size shiftsColumns) const |

| void | registerWithMarketData () |

Additional Inherited Members | |

| Public Types inherited from Observer | |

| typedef set_type::iterator | iterator |

| Protected Member Functions inherited from LazyObject | |

| virtual void | calculate () const |

| Protected Member Functions inherited from SwaptionVolatilityStructure | |

| virtual ext::shared_ptr< SmileSection > | smileSectionImpl (const Date &optionDate, const Period &swapTenor) const |

| virtual Volatility | volatilityImpl (const Date &optionDate, const Period &swapTenor, Rate strike) const |

| virtual Real | shiftImpl (const Date &optionDate, const Period &swapTenor) const |

| void | checkSwapTenor (const Period &swapTenor, bool extrapolate) const |

| void | checkSwapTenor (Time swapLength, bool extrapolate) const |

| Protected Member Functions inherited from VolatilityTermStructure | |

| void | checkStrike (Rate strike, bool extrapolate) const |

| strike-range check More... | |

| Protected Member Functions inherited from TermStructure | |

| void | checkRange (const Date &d, bool extrapolate) const |

| date-range check More... | |

| void | checkRange (Time t, bool extrapolate) const |

| time-range check More... | |

| Protected Attributes inherited from SwaptionVolatilityDiscrete | |

| Size | nOptionTenors_ |

| std::vector< Period > | optionTenors_ |

| std::vector< Date > | optionDates_ |

| std::vector< Time > | optionTimes_ |

| Interpolation | optionInterpolator_ |

| std::vector< Real > | optionDatesAsReal_ |

| std::vector< Time > | optionInterpolatorTimes_ |

| std::vector< Real > | optionInterpolatorDatesAsReal_ |

| Size | nSwapTenors_ |

| std::vector< Period > | swapTenors_ |

| std::vector< Time > | swapLengths_ |

| Date | cachedReferenceDate_ |

| Protected Attributes inherited from LazyObject | |

| bool | calculated_ = false |

| bool | frozen_ = false |

| bool | alwaysForward_ |

| Protected Attributes inherited from TermStructure | |

| bool | moving_ = false |

| bool | updated_ = true |

| Calendar | calendar_ |

Detailed Description

At-the-money swaption-volatility matrix.

This class provides the at-the-money volatility for a given swaption by interpolating a volatility matrix whose elements are the market volatilities of a set of swaption with given option date and swapLength.

The volatility matrix M must be defined so that:

- the number of rows equals the number of option dates;

- the number of columns equals the number of swap tenors;

M[i][j]contains the volatility corresponding to thei-th option andj-th tenor.

Definition at line 51 of file swaptionvolmatrix.hpp.

Constructor & Destructor Documentation

◆ SwaptionVolatilityMatrix() [1/7]

| SwaptionVolatilityMatrix | ( | const Calendar & | calendar, |

| BusinessDayConvention | bdc, | ||

| const std::vector< Period > & | optionTenors, | ||

| const std::vector< Period > & | swapTenors, | ||

| const std::vector< std::vector< Handle< Quote > > > & | vols, | ||

| const DayCounter & | dayCounter, | ||

| bool | flatExtrapolation = false, |

||

| VolatilityType | type = ShiftedLognormal, |

||

| const std::vector< std::vector< Real > > & | shifts = std::vector<std::vector<Real> >() |

||

| ) |

floating reference date, floating market data

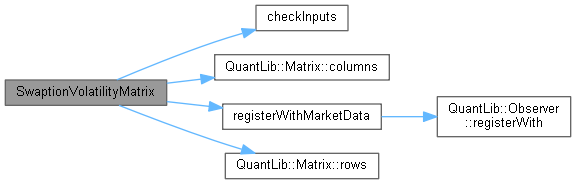

Definition at line 36 of file swaptionvolmatrix.cpp.

Here is the call graph for this function:

◆ SwaptionVolatilityMatrix() [2/7]

| SwaptionVolatilityMatrix | ( | const Date & | referenceDate, |

| const Calendar & | calendar, | ||

| BusinessDayConvention | bdc, | ||

| const std::vector< Period > & | optionTenors, | ||

| const std::vector< Period > & | swapTenors, | ||

| const std::vector< std::vector< Handle< Quote > > > & | vols, | ||

| const DayCounter & | dayCounter, | ||

| bool | flatExtrapolation = false, |

||

| VolatilityType | type = ShiftedLognormal, |

||

| const std::vector< std::vector< Real > > & | shifts = std::vector<std::vector<Real> >() |

||

| ) |

fixed reference date, floating market data

Definition at line 73 of file swaptionvolmatrix.cpp.

Here is the call graph for this function:

◆ SwaptionVolatilityMatrix() [3/7]

| SwaptionVolatilityMatrix | ( | const Calendar & | calendar, |

| BusinessDayConvention | bdc, | ||

| const std::vector< Period > & | optionTenors, | ||

| const std::vector< Period > & | swapTenors, | ||

| const Matrix & | volatilities, | ||

| const DayCounter & | dayCounter, | ||

| bool | flatExtrapolation = false, |

||

| VolatilityType | type = ShiftedLognormal, |

||

| const Matrix & | shifts = Matrix() |

||

| ) |

floating reference date, fixed market data

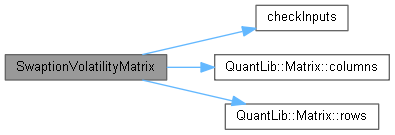

Definition at line 111 of file swaptionvolmatrix.cpp.

Here is the call graph for this function:

◆ SwaptionVolatilityMatrix() [4/7]

| SwaptionVolatilityMatrix | ( | const Date & | referenceDate, |

| const Calendar & | calendar, | ||

| BusinessDayConvention | bdc, | ||

| const std::vector< Period > & | optionTenors, | ||

| const std::vector< Period > & | swapTenors, | ||

| const Matrix & | volatilities, | ||

| const DayCounter & | dayCounter, | ||

| bool | flatExtrapolation = false, |

||

| VolatilityType | type = ShiftedLognormal, |

||

| const Matrix & | shifts = Matrix() |

||

| ) |

fixed reference date, fixed market data

Definition at line 159 of file swaptionvolmatrix.cpp.

Here is the call graph for this function:

◆ SwaptionVolatilityMatrix() [5/7]

| SwaptionVolatilityMatrix | ( | const Date & | referenceDate, |

| const Calendar & | calendar, | ||

| BusinessDayConvention | bdc, | ||

| const std::vector< Date > & | optionDates, | ||

| const std::vector< Period > & | swapTenors, | ||

| const Matrix & | volatilities, | ||

| const DayCounter & | dayCounter, | ||

| bool | flatExtrapolation = false, |

||

| VolatilityType | type = ShiftedLognormal, |

||

| const Matrix & | shifts = Matrix() |

||

| ) |

fixed reference date and fixed market data, option dates

Definition at line 208 of file swaptionvolmatrix.cpp.

Here is the call graph for this function:

◆ SwaptionVolatilityMatrix() [6/7]

|

delete |

◆ SwaptionVolatilityMatrix() [7/7]

|

delete |

◆ ~SwaptionVolatilityMatrix()

|

overridedefault |

Member Function Documentation

◆ operator=() [1/2]

|

delete |

◆ operator=() [2/2]

|

delete |

◆ performCalculations()

|

overridevirtual |

This method must implement any calculations which must be (re)done in order to calculate the desired results.

Reimplemented from SwaptionVolatilityDiscrete.

Definition at line 294 of file swaptionvolmatrix.cpp.

Here is the call graph for this function:

◆ maxDate()

|

overridevirtual |

the latest date for which the curve can return values

Implements TermStructure.

Definition at line 175 of file swaptionvolmatrix.hpp.

◆ minStrike()

|

overridevirtual |

the minimum strike for which the term structure can return vols

Implements VolatilityTermStructure.

Definition at line 179 of file swaptionvolmatrix.hpp.

◆ maxStrike()

|

overridevirtual |

the maximum strike for which the term structure can return vols

Implements VolatilityTermStructure.

Definition at line 183 of file swaptionvolmatrix.hpp.

◆ maxSwapTenor()

|

overridevirtual |

the largest length for which the term structure can return vols

Implements SwaptionVolatilityStructure.

Definition at line 187 of file swaptionvolmatrix.hpp.

◆ locate() [1/2]

returns the lower indexes of surrounding volatility matrix corners

Definition at line 137 of file swaptionvolmatrix.hpp.

Here is the call graph for this function: Here is the caller graph for this function:

Here is the caller graph for this function:

◆ locate() [2/2]

returns the lower indexes of surrounding volatility matrix corners

Definition at line 143 of file swaptionvolmatrix.hpp.

Here is the call graph for this function:

◆ volatilityType()

|

overridevirtual |

volatility type

Reimplemented from SwaptionVolatilityStructure.

Definition at line 198 of file swaptionvolmatrix.hpp.

Here is the caller graph for this function:

◆ smileSectionImpl()

|

overrideprotectedvirtual |

Implements SwaptionVolatilityStructure.

Definition at line 320 of file swaptionvolmatrix.cpp.

Here is the call graph for this function:

◆ volatilityImpl()

|

overrideprotectedvirtual |

Implements SwaptionVolatilityStructure.

Definition at line 191 of file swaptionvolmatrix.hpp.

Here is the call graph for this function: Here is the caller graph for this function:

Here is the caller graph for this function:

◆ shiftImpl()

Reimplemented from SwaptionVolatilityStructure.

Definition at line 202 of file swaptionvolmatrix.hpp.

Here is the call graph for this function:

◆ checkInputs()

◆ registerWithMarketData()

|

private |

Definition at line 287 of file swaptionvolmatrix.cpp.

Here is the call graph for this function: Here is the caller graph for this function:

Here is the caller graph for this function:

Member Data Documentation

◆ volHandles_

Definition at line 166 of file swaptionvolmatrix.hpp.

◆ shiftValues_

|

private |

Definition at line 167 of file swaptionvolmatrix.hpp.

◆ volatilities_

|

mutableprivate |

Definition at line 168 of file swaptionvolmatrix.hpp.

◆ shifts_

|

private |

Definition at line 168 of file swaptionvolmatrix.hpp.

◆ interpolation_

|

private |

Definition at line 169 of file swaptionvolmatrix.hpp.

◆ interpolationShifts_

|

private |

Definition at line 169 of file swaptionvolmatrix.hpp.

◆ volatilityType_

|

private |

Definition at line 170 of file swaptionvolmatrix.hpp.