Base class for inflation-rate indexes,. More...

#include <inflationindex.hpp>

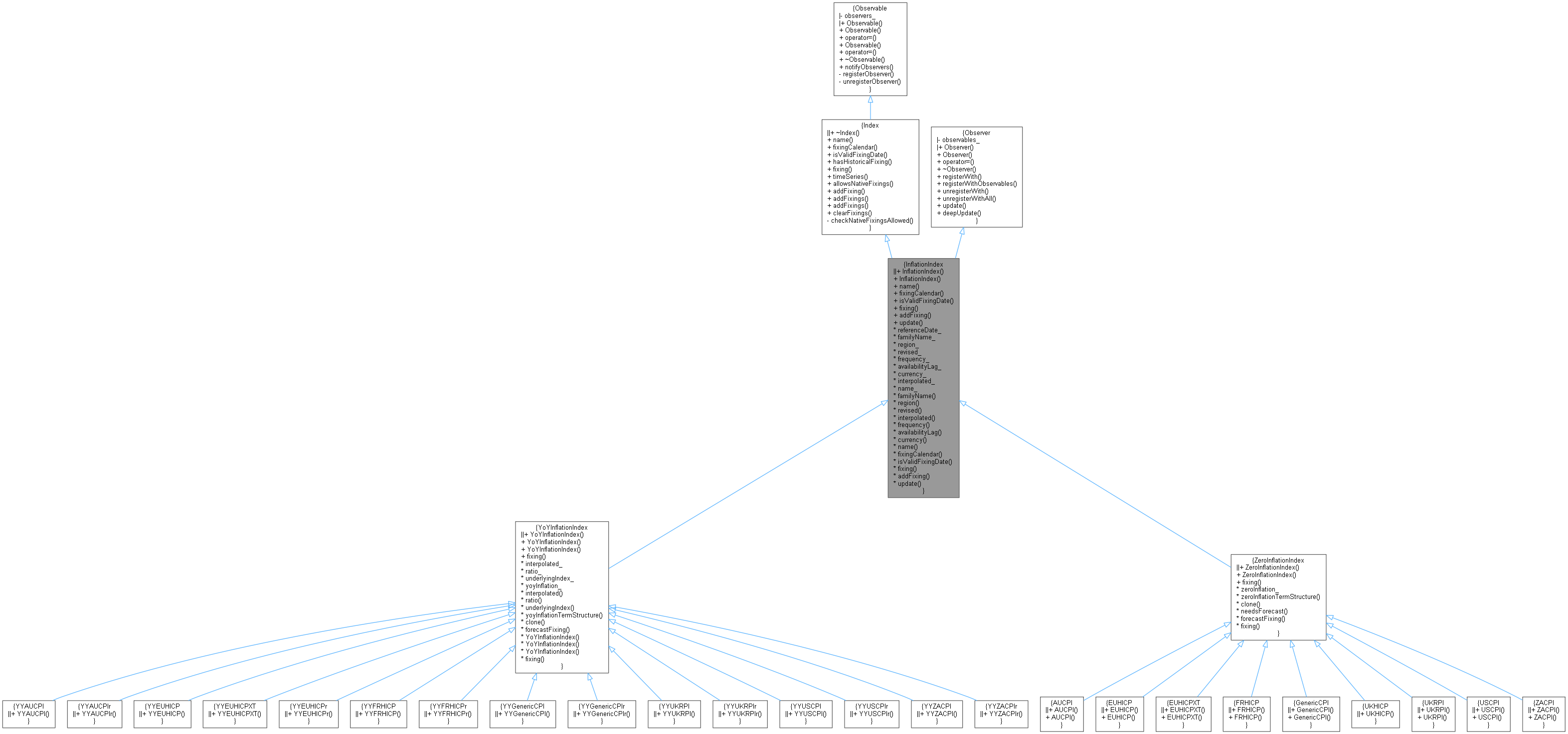

Inheritance diagram for InflationIndex:

Inheritance diagram for InflationIndex: Collaboration diagram for InflationIndex:

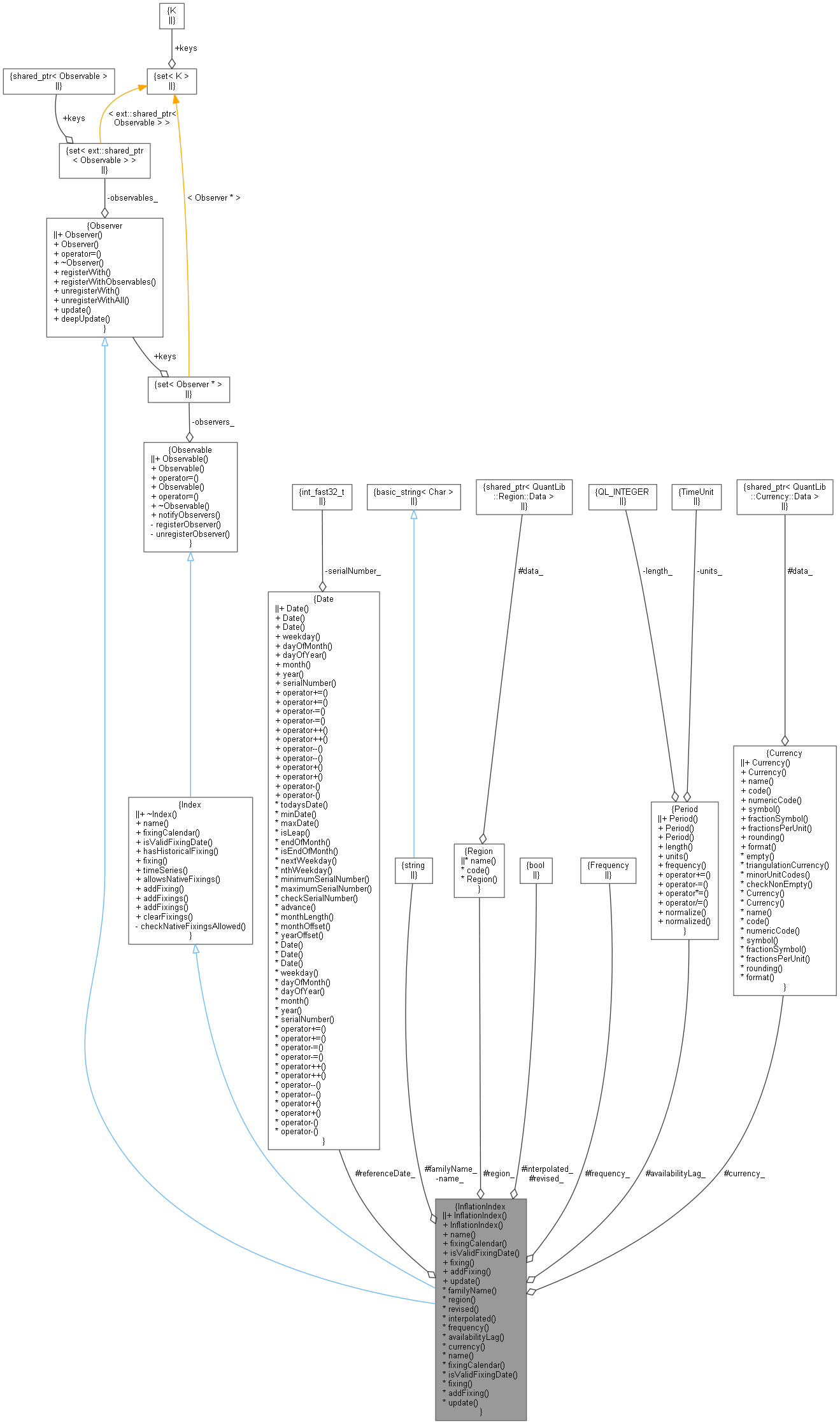

Collaboration diagram for InflationIndex:

Public Member Functions | |

| InflationIndex (std::string familyName, Region region, bool revised, Frequency frequency, const Period &availabilitiyLag, Currency currency) | |

Index interface | |

| std::string | name () const override |

| Returns the name of the index. More... | |

| Calendar | fixingCalendar () const override |

| bool | isValidFixingDate (const Date &) const override |

| returns TRUE if the fixing date is a valid one More... | |

| Real | fixing (const Date &fixingDate, bool forecastTodaysFixing=false) const override=0 |

| Real | pastFixing (const Date &fixingDate) const override=0 |

| returns a past fixing at the given date More... | |

| void | addFixing (const Date &fixingDate, Rate fixing, bool forceOverwrite=false) override |

| Public Member Functions inherited from Index | |

| ~Index () override=default | |

| virtual std::string | name () const =0 |

| Returns the name of the index. More... | |

| virtual Calendar | fixingCalendar () const =0 |

| returns the calendar defining valid fixing dates More... | |

| virtual bool | isValidFixingDate (const Date &fixingDate) const =0 |

| returns TRUE if the fixing date is a valid one More... | |

| bool | hasHistoricalFixing (const Date &fixingDate) const |

| returns whether a historical fixing was stored for the given date More... | |

| virtual Real | fixing (const Date &fixingDate, bool forecastTodaysFixing=false) const =0 |

| returns the fixing at the given date More... | |

| virtual Real | pastFixing (const Date &fixingDate) const |

| returns a past fixing at the given date More... | |

| const TimeSeries< Real > & | timeSeries () const |

| returns the fixing TimeSeries More... | |

| virtual bool | allowsNativeFixings () |

| check if index allows for native fixings. More... | |

| void | update () override |

| void | addFixings (const TimeSeries< Real > &t, bool forceOverwrite=false) |

| stores historical fixings from a TimeSeries More... | |

| template<class DateIterator , class ValueIterator > | |

| void | addFixings (DateIterator dBegin, DateIterator dEnd, ValueIterator vBegin, bool forceOverwrite=false) |

| stores historical fixings at the given dates More... | |

| void | clearFixings () |

| clears all stored historical fixings More... | |

| Public Member Functions inherited from Observable | |

| Observable ()=default | |

| Observable (const Observable &) | |

| Observable & | operator= (const Observable &) |

| Observable (Observable &&)=delete | |

| Observable & | operator= (Observable &&)=delete |

| virtual | ~Observable ()=default |

| void | notifyObservers () |

| Public Member Functions inherited from Observer | |

| Observer ()=default | |

| Observer (const Observer &) | |

| Observer & | operator= (const Observer &) |

| virtual | ~Observer () |

| std::pair< iterator, bool > | registerWith (const ext::shared_ptr< Observable > &) |

| void | registerWithObservables (const ext::shared_ptr< Observer > &) |

| Size | unregisterWith (const ext::shared_ptr< Observable > &) |

| void | unregisterWithAll () |

| virtual void | update ()=0 |

| virtual void | deepUpdate () |

Inspectors | |

| Date | referenceDate_ |

| std::string | familyName_ |

| Region | region_ |

| bool | revised_ |

| Frequency | frequency_ |

| Period | availabilityLag_ |

| Currency | currency_ |

| std::string | name_ |

| std::string | familyName () const |

| Region | region () const |

| bool | revised () const |

| Frequency | frequency () const |

| Period | availabilityLag () const |

| Currency | currency () const |

Additional Inherited Members | |

| Public Types inherited from Observer | |

| typedef set_type::iterator | iterator |

| Protected Member Functions inherited from Index | |

| ext::shared_ptr< Observable > | notifier () const |

Detailed Description

Base class for inflation-rate indexes,.

Definition at line 84 of file inflationindex.hpp.

Constructor & Destructor Documentation

◆ InflationIndex()

Member Function Documentation

◆ name()

|

overridevirtual |

Returns the name of the index.

- Warning:

- This method is used for output and comparison between indexes. It is not meant to be used for writing switch-on-type code.

Implements Index.

Definition at line 295 of file inflationindex.hpp.

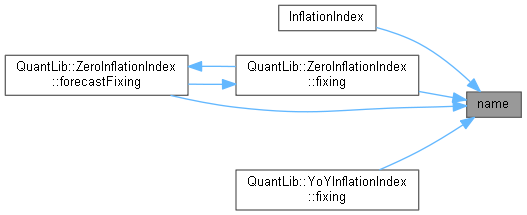

Here is the caller graph for this function:

◆ fixingCalendar()

|

overridevirtual |

Inflation indices are not associated to a particular day, but to months or quarters. Therefore, they do not have fixing calendars. Since we're forced by the base Index interface to add one, this method returns a NullCalendar instance.

Implements Index.

Definition at line 132 of file inflationindex.cpp.

◆ isValidFixingDate()

returns TRUE if the fixing date is a valid one

Implements Index.

Definition at line 104 of file inflationindex.hpp.

◆ fixing()

|

overridepure virtual |

Forecasting index values requires an inflation term structure, with a base date that is earlier than its asof date. This must be so because indices are available only with a lag. Usually, it makes sense for the base date to be the first day of the month of the last published fixing.

Implements Index.

Implemented in ZeroInflationIndex, and YoYInflationIndex.

Here is the caller graph for this function:

◆ pastFixing()

returns a past fixing at the given date

Reimplemented from Index.

Implemented in ZeroInflationIndex, and YoYInflationIndex.

◆ addFixing()

|

overridevirtual |

Reimplemented from Index.

Definition at line 137 of file inflationindex.cpp.

Here is the call graph for this function:

◆ familyName()

| std::string familyName | ( | ) | const |

Definition at line 299 of file inflationindex.hpp.

◆ region()

| Region region | ( | ) | const |

Definition at line 303 of file inflationindex.hpp.

◆ revised()

| bool revised | ( | ) | const |

Definition at line 307 of file inflationindex.hpp.

◆ frequency()

| Frequency frequency | ( | ) | const |

Definition at line 311 of file inflationindex.hpp.

◆ availabilityLag()

| Period availabilityLag | ( | ) | const |

The availability lag describes when the index might be available; for instance, the inflation value for January may only be available in April. This doesn't mean that that inflation value is considered as the April fixing; it remains the January fixing, independently of the lag in availability.

Definition at line 315 of file inflationindex.hpp.

◆ currency()

| Currency currency | ( | ) | const |

Definition at line 319 of file inflationindex.hpp.

Member Data Documentation

◆ referenceDate_

|

protected |

Definition at line 139 of file inflationindex.hpp.

◆ familyName_

|

protected |

Definition at line 140 of file inflationindex.hpp.

◆ region_

|

protected |

Definition at line 141 of file inflationindex.hpp.

◆ revised_

|

protected |

Definition at line 142 of file inflationindex.hpp.

◆ frequency_

|

protected |

Definition at line 143 of file inflationindex.hpp.

◆ availabilityLag_

|

protected |

Definition at line 144 of file inflationindex.hpp.

◆ currency_

|

protected |

Definition at line 145 of file inflationindex.hpp.

◆ name_

|

private |

Definition at line 148 of file inflationindex.hpp.