Base class for year-on-year inflation indices. More...

#include <inflationindex.hpp>

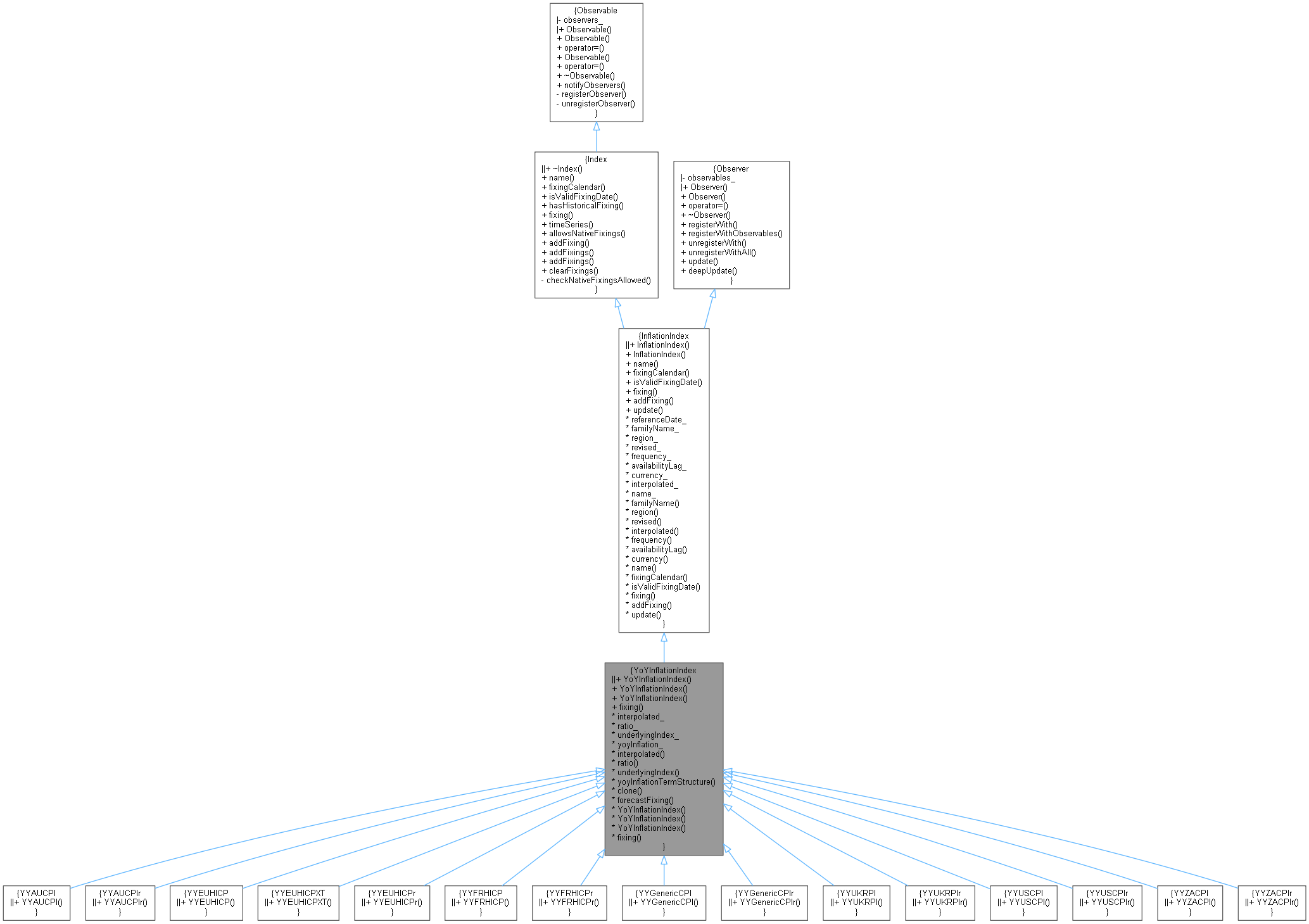

Inheritance diagram for YoYInflationIndex:

Inheritance diagram for YoYInflationIndex: Collaboration diagram for YoYInflationIndex:

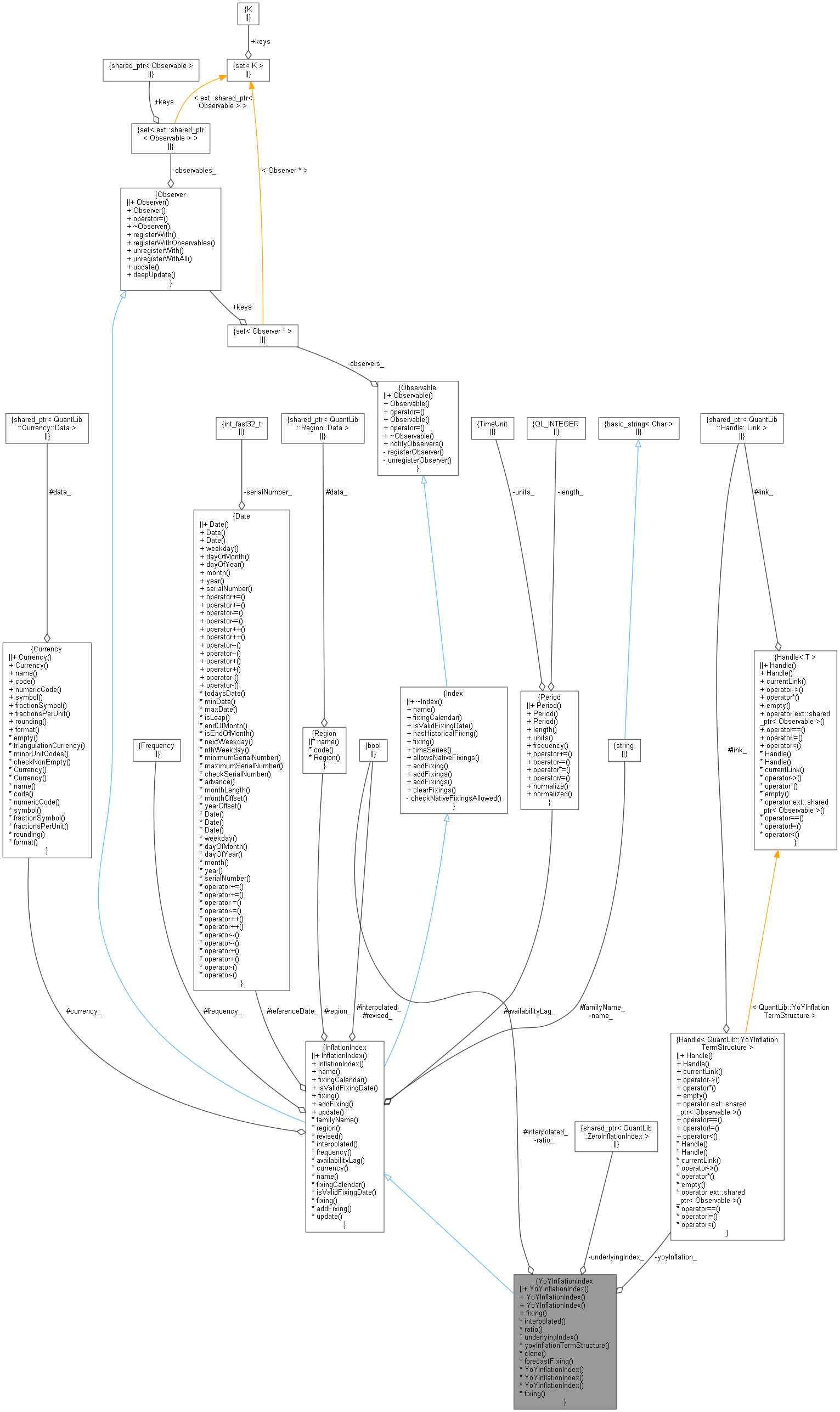

Collaboration diagram for YoYInflationIndex:

Public Member Functions | |

Constructors | |

| YoYInflationIndex (const ext::shared_ptr< ZeroInflationIndex > &underlyingIndex, Handle< YoYInflationTermStructure > ts={}) | |

| Constructor for year-on-year indices defined as a ratio. More... | |

| YoYInflationIndex (const ext::shared_ptr< ZeroInflationIndex > &underlyingIndex, bool interpolated, Handle< YoYInflationTermStructure > ts={}) | |

| YoYInflationIndex (const std::string &familyName, const Region ®ion, bool revised, Frequency frequency, const Period &availabilityLag, const Currency ¤cy, Handle< YoYInflationTermStructure > ts={}) | |

| Constructor for quoted year-on-year indices. More... | |

| YoYInflationIndex (const std::string &familyName, const Region ®ion, bool revised, bool interpolated, Frequency frequency, const Period &availabilityLag, const Currency ¤cy, Handle< YoYInflationTermStructure > ts={}) | |

Index interface | |

| Rate | fixing (const Date &fixingDate, bool forecastTodaysFixing=false) const override |

| Real | pastFixing (const Date &fixingDate) const override |

| returns a past fixing at the given date More... | |

| Public Member Functions inherited from InflationIndex | |

| InflationIndex (std::string familyName, Region region, bool revised, Frequency frequency, const Period &availabilitiyLag, Currency currency) | |

| std::string | name () const override |

| Returns the name of the index. More... | |

| Calendar | fixingCalendar () const override |

| bool | isValidFixingDate (const Date &) const override |

| returns TRUE if the fixing date is a valid one More... | |

| void | addFixing (const Date &fixingDate, Rate fixing, bool forceOverwrite=false) override |

| std::string | familyName () const |

| Region | region () const |

| bool | revised () const |

| Frequency | frequency () const |

| Period | availabilityLag () const |

| Currency | currency () const |

| Public Member Functions inherited from Index | |

| ~Index () override=default | |

| virtual std::string | name () const =0 |

| Returns the name of the index. More... | |

| virtual Calendar | fixingCalendar () const =0 |

| returns the calendar defining valid fixing dates More... | |

| virtual bool | isValidFixingDate (const Date &fixingDate) const =0 |

| returns TRUE if the fixing date is a valid one More... | |

| bool | hasHistoricalFixing (const Date &fixingDate) const |

| returns whether a historical fixing was stored for the given date More... | |

| virtual Real | fixing (const Date &fixingDate, bool forecastTodaysFixing=false) const =0 |

| returns the fixing at the given date More... | |

| virtual Real | pastFixing (const Date &fixingDate) const |

| returns a past fixing at the given date More... | |

| const TimeSeries< Real > & | timeSeries () const |

| returns the fixing TimeSeries More... | |

| virtual bool | allowsNativeFixings () |

| check if index allows for native fixings. More... | |

| void | update () override |

| void | addFixings (const TimeSeries< Real > &t, bool forceOverwrite=false) |

| stores historical fixings from a TimeSeries More... | |

| template<class DateIterator , class ValueIterator > | |

| void | addFixings (DateIterator dBegin, DateIterator dEnd, ValueIterator vBegin, bool forceOverwrite=false) |

| stores historical fixings at the given dates More... | |

| void | clearFixings () |

| clears all stored historical fixings More... | |

| Public Member Functions inherited from Observable | |

| Observable ()=default | |

| Observable (const Observable &) | |

| Observable & | operator= (const Observable &) |

| Observable (Observable &&)=delete | |

| Observable & | operator= (Observable &&)=delete |

| virtual | ~Observable ()=default |

| void | notifyObservers () |

| Public Member Functions inherited from Observer | |

| Observer ()=default | |

| Observer (const Observer &) | |

| Observer & | operator= (const Observer &) |

| virtual | ~Observer () |

| std::pair< iterator, bool > | registerWith (const ext::shared_ptr< Observable > &) |

| void | registerWithObservables (const ext::shared_ptr< Observer > &) |

| Size | unregisterWith (const ext::shared_ptr< Observable > &) |

| void | unregisterWithAll () |

| virtual void | update ()=0 |

| virtual void | deepUpdate () |

Other methods | |

| bool | interpolated_ |

| bool | ratio_ |

| ext::shared_ptr< ZeroInflationIndex > | underlyingIndex_ |

| Handle< YoYInflationTermStructure > | yoyInflation_ |

| Date | lastFixingDate () const |

| bool | interpolated () const |

| bool | ratio () const |

| ext::shared_ptr< ZeroInflationIndex > | underlyingIndex () const |

| Handle< YoYInflationTermStructure > | yoyInflationTermStructure () const |

| ext::shared_ptr< YoYInflationIndex > | clone (const Handle< YoYInflationTermStructure > &h) const |

| bool | needsForecast (const Date &fixingDate) const |

| Rate | forecastFixing (const Date &fixingDate) const |

Additional Inherited Members | |

| Public Types inherited from Observer | |

| typedef set_type::iterator | iterator |

| Protected Member Functions inherited from Index | |

| ext::shared_ptr< Observable > | notifier () const |

| Protected Attributes inherited from InflationIndex | |

| Date | referenceDate_ |

| std::string | familyName_ |

| Region | region_ |

| bool | revised_ |

| Frequency | frequency_ |

| Period | availabilityLag_ |

| Currency | currency_ |

Detailed Description

Base class for year-on-year inflation indices.

These may be quoted indices published on, say, Bloomberg, or can be defined as the ratio of an index at different time points.

Definition at line 189 of file inflationindex.hpp.

Constructor & Destructor Documentation

◆ YoYInflationIndex() [1/4]

|

explicit |

Constructor for year-on-year indices defined as a ratio.

An index build with this constructor won't store past fixings of its own; they will be calculated as a ratio from the past fixings stored in the underlying index.

Definition at line 243 of file inflationindex.cpp.

Here is the call graph for this function:

◆ YoYInflationIndex() [2/4]

| YoYInflationIndex | ( | const ext::shared_ptr< ZeroInflationIndex > & | underlyingIndex, |

| bool | interpolated, | ||

| Handle< YoYInflationTermStructure > | ts = {} |

||

| ) |

- Deprecated:

- Use the similar overload without the interpolated parameter. Deprecated in version 1.38.

Definition at line 254 of file inflationindex.cpp.

Here is the call graph for this function:

◆ YoYInflationIndex() [3/4]

| YoYInflationIndex | ( | const std::string & | familyName, |

| const Region & | region, | ||

| bool | revised, | ||

| Frequency | frequency, | ||

| const Period & | availabilityLag, | ||

| const Currency & | currency, | ||

| Handle< YoYInflationTermStructure > | ts = {} |

||

| ) |

Constructor for quoted year-on-year indices.

An index built with this constructor needs its past fixings (i.e., the past year-on-year values) to be stored via the addFixing or addFixings method.

Definition at line 261 of file inflationindex.cpp.

Here is the call graph for this function:

◆ YoYInflationIndex() [4/4]

| YoYInflationIndex | ( | const std::string & | familyName, |

| const Region & | region, | ||

| bool | revised, | ||

| bool | interpolated, | ||

| Frequency | frequency, | ||

| const Period & | availabilityLag, | ||

| const Currency & | currency, | ||

| Handle< YoYInflationTermStructure > | ts = {} |

||

| ) |

- Deprecated:

- Use the similar overload without the interpolated parameter. Deprecated in version 1.38.

Definition at line 273 of file inflationindex.cpp.

Here is the call graph for this function:

Member Function Documentation

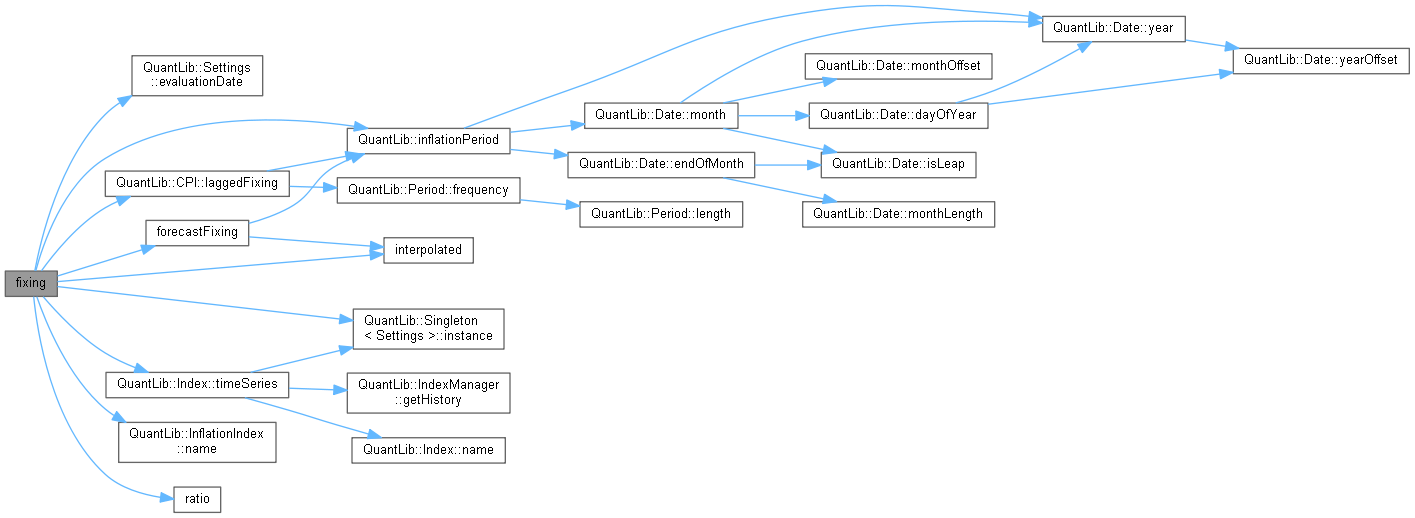

◆ fixing()

Implements InflationIndex.

Definition at line 286 of file inflationindex.cpp.

Here is the call graph for this function:

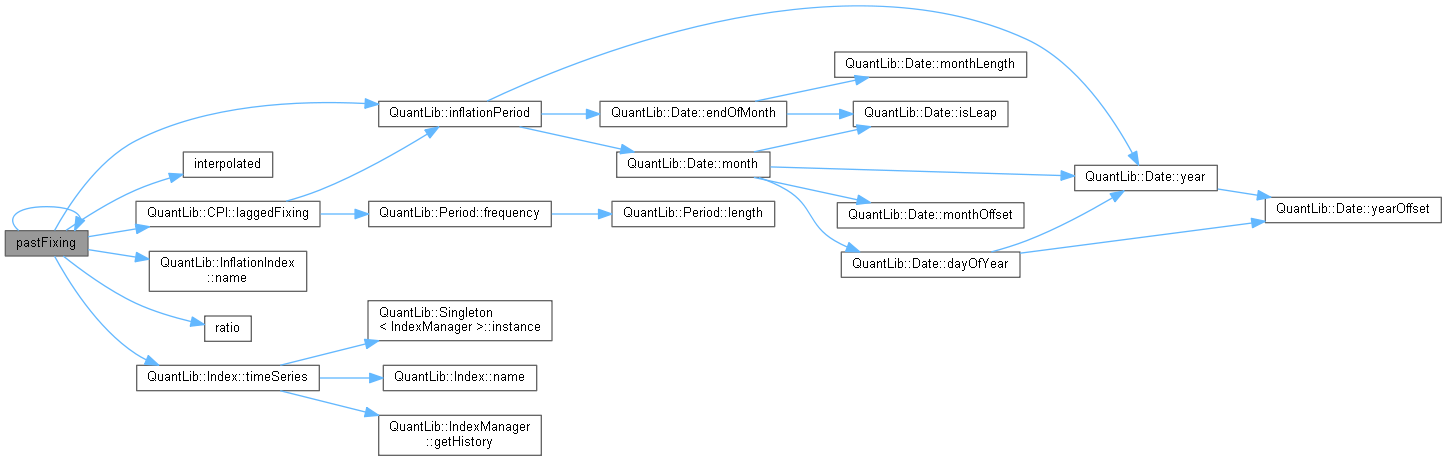

◆ pastFixing()

returns a past fixing at the given date

Implements InflationIndex.

Definition at line 337 of file inflationindex.cpp.

Here is the call graph for this function: Here is the caller graph for this function:

Here is the caller graph for this function:

◆ lastFixingDate()

| Date lastFixingDate | ( | ) | const |

◆ interpolated()

| bool interpolated | ( | ) | const |

◆ ratio()

| bool ratio | ( | ) | const |

◆ underlyingIndex()

| ext::shared_ptr< ZeroInflationIndex > underlyingIndex | ( | ) | const |

Definition at line 336 of file inflationindex.hpp.

◆ yoyInflationTermStructure()

| Handle< YoYInflationTermStructure > yoyInflationTermStructure | ( | ) | const |

Definition at line 341 of file inflationindex.hpp.

◆ clone()

| ext::shared_ptr< YoYInflationIndex > clone | ( | const Handle< YoYInflationTermStructure > & | h | ) | const |

Definition at line 387 of file inflationindex.cpp.

◆ needsForecast()

Definition at line 306 of file inflationindex.cpp.

Here is the call graph for this function: Here is the caller graph for this function:

Here is the caller graph for this function:

◆ forecastFixing()

Definition at line 373 of file inflationindex.cpp.

Here is the call graph for this function: Here is the caller graph for this function:

Here is the caller graph for this function:

Member Data Documentation

◆ interpolated_

|

protected |

Definition at line 262 of file inflationindex.hpp.

◆ ratio_

|

private |

Definition at line 266 of file inflationindex.hpp.

◆ underlyingIndex_

|

private |

Definition at line 267 of file inflationindex.hpp.

◆ yoyInflation_

|

private |

Definition at line 268 of file inflationindex.hpp.