Base class for year-on-year inflation term structures. More...

#include <inflationtermstructure.hpp>

Inheritance diagram for YoYInflationTermStructure:

Inheritance diagram for YoYInflationTermStructure: Collaboration diagram for YoYInflationTermStructure:

Collaboration diagram for YoYInflationTermStructure:

Inspectors | |

| bool | indexIsInterpolated_ = false |

| Rate | yoyRate (const Date &d, const Period &instObsLag=Period(-1, Days), bool forceLinearInterpolation=false, bool extrapolate=false) const |

| year-on-year inflation rate. More... | |

| Rate | yoyRate (Time t, bool extrapolate=false) const |

| year-on-year inflation rate. More... | |

| virtual bool | indexIsInterpolated () const |

| virtual Rate | yoyRateImpl (Time time) const =0 |

| to be defined in derived classes More... | |

Additional Inherited Members | |

| Public Types inherited from Observer | |

| typedef set_type::iterator | iterator |

| Protected Member Functions inherited from InflationTermStructure | |

| void | checkRange (const Date &, bool extrapolate) const |

| void | checkRange (Time t, bool extrapolate) const |

| Protected Member Functions inherited from TermStructure | |

| void | checkRange (const Date &d, bool extrapolate) const |

| date-range check More... | |

| void | checkRange (Time t, bool extrapolate) const |

| time-range check More... | |

| Protected Attributes inherited from InflationTermStructure | |

| ext::shared_ptr< Seasonality > | seasonality_ |

| Period | observationLag_ |

| Frequency | frequency_ |

| Rate | baseRate_ |

| Protected Attributes inherited from TermStructure | |

| bool | moving_ = false |

| bool | updated_ = true |

| Calendar | calendar_ |

Detailed Description

Base class for year-on-year inflation term structures.

Definition at line 181 of file inflationtermstructure.hpp.

Constructor & Destructor Documentation

◆ YoYInflationTermStructure() [1/6]

| QL_DEPRECATED_DISABLE_WARNING YoYInflationTermStructure | ( | Date | baseDate, |

| Rate | baseYoYRate, | ||

| Frequency | frequency, | ||

| const DayCounter & | dayCounter, | ||

| const ext::shared_ptr< Seasonality > & | seasonality = {} |

||

| ) |

Definition at line 179 of file inflationtermstructure.cpp.

◆ YoYInflationTermStructure() [2/6]

| YoYInflationTermStructure | ( | const Date & | referenceDate, |

| Date | baseDate, | ||

| Rate | baseYoYRate, | ||

| Frequency | frequency, | ||

| const DayCounter & | dayCounter, | ||

| const ext::shared_ptr< Seasonality > & | seasonality = {} |

||

| ) |

Definition at line 187 of file inflationtermstructure.cpp.

◆ YoYInflationTermStructure() [3/6]

| YoYInflationTermStructure | ( | Natural | settlementDays, |

| const Calendar & | calendar, | ||

| Date | baseDate, | ||

| Rate | baseYoYRate, | ||

| Frequency | frequency, | ||

| const DayCounter & | dayCounter, | ||

| const ext::shared_ptr< Seasonality > & | seasonality = {} |

||

| ) |

Definition at line 196 of file inflationtermstructure.cpp.

◆ YoYInflationTermStructure() [4/6]

| YoYInflationTermStructure | ( | Date | baseDate, |

| Rate | baseYoYRate, | ||

| Frequency | frequency, | ||

| bool | indexIsInterpolated, | ||

| const DayCounter & | dayCounter, | ||

| const ext::shared_ptr< Seasonality > & | seasonality = {} |

||

| ) |

- Deprecated:

- Use an overload with an explicit base date and without indexIsInterpolated. Deprecated in version 1.37.

Definition at line 206 of file inflationtermstructure.cpp.

Here is the call graph for this function:

◆ YoYInflationTermStructure() [5/6]

| YoYInflationTermStructure | ( | const Date & | referenceDate, |

| Date | baseDate, | ||

| Rate | baseYoYRate, | ||

| Frequency | frequency, | ||

| bool | indexIsInterpolated, | ||

| const DayCounter & | dayCounter, | ||

| const ext::shared_ptr< Seasonality > & | seasonality = {} |

||

| ) |

- Deprecated:

- Use an overload with an explicit base date and without indexIsInterpolated. Deprecated in version 1.37.

Definition at line 217 of file inflationtermstructure.cpp.

Here is the call graph for this function:

◆ YoYInflationTermStructure() [6/6]

| YoYInflationTermStructure | ( | Natural | settlementDays, |

| const Calendar & | calendar, | ||

| Date | baseDate, | ||

| Rate | baseYoYRate, | ||

| Frequency | frequency, | ||

| bool | indexIsInterpolated, | ||

| const DayCounter & | dayCounter, | ||

| const ext::shared_ptr< Seasonality > & | seasonality = {} |

||

| ) |

- Deprecated:

- Use an overload with an explicit base date and without indexIsInterpolated. Deprecated in version 1.37.

Definition at line 230 of file inflationtermstructure.cpp.

Here is the call graph for this function:

◆ ~YoYInflationTermStructure()

|

overridedefault |

Member Function Documentation

◆ yoyRate() [1/2]

| QL_DEPRECATED_ENABLE_WARNING Rate yoyRate | ( | const Date & | d, |

| const Period & | instObsLag = Period(-1,Days), |

||

| bool | forceLinearInterpolation = false, |

||

| bool | extrapolate = false |

||

| ) | const |

year-on-year inflation rate.

The forceLinearInterpolation parameter is relative to the frequency of the TS.

- Note

- this is not the year-on-year swap (YYIIS) rate.

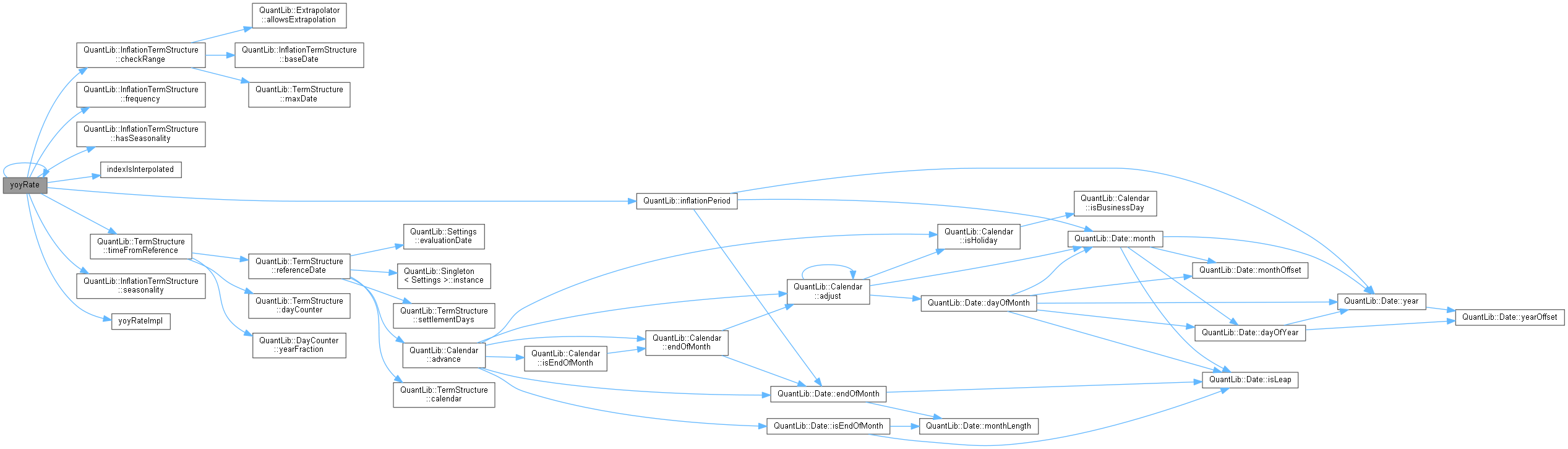

Definition at line 246 of file inflationtermstructure.cpp.

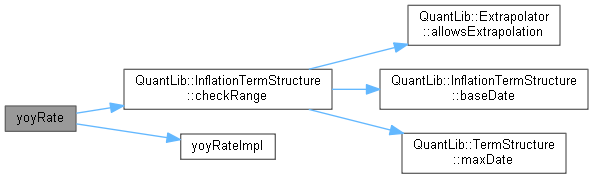

Here is the call graph for this function: Here is the caller graph for this function:

Here is the caller graph for this function:

◆ yoyRate() [2/2]

year-on-year inflation rate.

- Warning:

- Since inflation is highly linked to dates (lags, interpolation, months for seasonality, etc) this method cannot account for all effects. If you call it, You'll have to manage lag, seasonality etc. yourself.

Definition at line 290 of file inflationtermstructure.cpp.

Here is the call graph for this function:

◆ indexIsInterpolated()

|

virtual |

- Deprecated:

- This method will disappear. When it does, the curve will behave as if it returned false. Deprecated in version 1.37.

Definition at line 323 of file inflationtermstructure.hpp.

Here is the caller graph for this function:

◆ yoyRateImpl()

to be defined in derived classes

Implemented in InterpolatedYoYInflationCurve< Interpolator >, and PiecewiseYoYInflationCurve< Interpolator, Bootstrap, Traits >.

Here is the caller graph for this function:

Member Data Documentation

◆ indexIsInterpolated_

|

protected |

- Deprecated:

- This data member will disappear. When it does, the curve will behave as if it was false. Deprecated in version 1.37.

Definition at line 282 of file inflationtermstructure.hpp.