Capped or floored inflation coupon. More...

#include <ql/cashflows/capflooredinflationcoupon.hpp>

Inheritance diagram for CappedFlooredYoYInflationCoupon:

Inheritance diagram for CappedFlooredYoYInflationCoupon: Collaboration diagram for CappedFlooredYoYInflationCoupon:

Collaboration diagram for CappedFlooredYoYInflationCoupon:

Public Member Functions | |

| CappedFlooredYoYInflationCoupon (const ext::shared_ptr< YoYInflationCoupon > &underlying, Rate cap=Null< Rate >(), Rate floor=Null< Rate >()) | |

| CappedFlooredYoYInflationCoupon (const Date &paymentDate, Real nominal, const Date &startDate, const Date &endDate, Natural fixingDays, const ext::shared_ptr< YoYInflationIndex > &index, const Period &observationLag, const DayCounter &dayCounter, Real gearing=1.0, Spread spread=0.0, const Rate cap=Null< Rate >(), const Rate floor=Null< Rate >(), const Date &refPeriodStart=Date(), const Date &refPeriodEnd=Date()) | |

augmented Coupon interface | |

| Rate | rate () const override |

| swap(let) rate More... | |

| Rate | cap () const |

| cap More... | |

| Rate | floor () const |

| floor More... | |

| Rate | effectiveCap () const |

| effective cap of fixing More... | |

| Rate | effectiveFloor () const |

| effective floor of fixing More... | |

Observer interface | |

| void | update () override |

| Public Member Functions inherited from YoYInflationCoupon | |

| YoYInflationCoupon (const Date &paymentDate, Real nominal, const Date &startDate, const Date &endDate, Natural fixingDays, const ext::shared_ptr< YoYInflationIndex > &index, const Period &observationLag, const DayCounter &dayCounter, Real gearing=1.0, Spread spread=0.0, const Date &refPeriodStart=Date(), const Date &refPeriodEnd=Date()) | |

| Real | gearing () const |

| index gearing, i.e. multiplicative coefficient for the index More... | |

| Spread | spread () const |

| spread paid over the fixing of the underlying index More... | |

| Rate | adjustedFixing () const |

| const ext::shared_ptr< YoYInflationIndex > & | yoyIndex () const |

| void | accept (AcyclicVisitor &) override |

| Public Member Functions inherited from InflationCoupon | |

| InflationCoupon (const Date &paymentDate, Real nominal, const Date &startDate, const Date &endDate, Natural fixingDays, ext::shared_ptr< InflationIndex > index, const Period &observationLag, DayCounter dayCounter, const Date &refPeriodStart=Date(), const Date &refPeriodEnd=Date(), const Date &exCouponDate=Date()) | |

| Real | amount () const override |

| returns the amount of the cash flow More... | |

| Real | price (const Handle< YieldTermStructure > &discountingCurve) const |

| DayCounter | dayCounter () const override |

| day counter for accrual calculation More... | |

| Real | accruedAmount (const Date &) const override |

| accrued amount at the given date More... | |

| Rate | rate () const override |

| accrued rate More... | |

| const ext::shared_ptr< InflationIndex > & | index () const |

| yoy inflation index More... | |

| Period | observationLag () const |

| how the coupon observes the index More... | |

| Natural | fixingDays () const |

| fixing days More... | |

| virtual Date | fixingDate () const |

| fixing date More... | |

| virtual Rate | indexFixing () const |

| fixing of the underlying index, as observed by the coupon More... | |

| void | performCalculations () const override |

| void | setPricer (const ext::shared_ptr< InflationCouponPricer > &) |

| ext::shared_ptr< InflationCouponPricer > | pricer () const |

| Public Member Functions inherited from Coupon | |

| Coupon (const Date &paymentDate, Real nominal, const Date &accrualStartDate, const Date &accrualEndDate, const Date &refPeriodStart=Date(), const Date &refPeriodEnd=Date(), const Date &exCouponDate=Date()) | |

| Date | date () const override |

| Date | exCouponDate () const override |

| returns the date that the cash flow trades exCoupon More... | |

| virtual Real | nominal () const |

| const Date & | accrualStartDate () const |

| start of the accrual period More... | |

| const Date & | accrualEndDate () const |

| end of the accrual period More... | |

| const Date & | referencePeriodStart () const |

| start date of the reference period More... | |

| const Date & | referencePeriodEnd () const |

| end date of the reference period More... | |

| Time | accrualPeriod () const |

| accrual period as fraction of year More... | |

| Date::serial_type | accrualDays () const |

| accrual period in days More... | |

| Time | accruedPeriod (const Date &) const |

| accrued period as fraction of year at the given date More... | |

| Date::serial_type | accruedDays (const Date &) const |

| accrued days at the given date More... | |

| Public Member Functions inherited from CashFlow | |

| ~CashFlow () override=default | |

| bool | hasOccurred (const Date &refDate=Date(), ext::optional< bool > includeRefDate=ext::nullopt) const override |

| returns true if an event has already occurred before a date More... | |

| bool | tradingExCoupon (const Date &refDate=Date()) const |

| returns true if the cashflow is trading ex-coupon on the refDate More... | |

| Public Member Functions inherited from Event | |

| ~Event () override=default | |

| Public Member Functions inherited from Observable | |

| Observable () | |

| Observable (const Observable &) | |

| Observable & | operator= (const Observable &) |

| Observable (Observable &&)=delete | |

| Observable & | operator= (Observable &&)=delete |

| virtual | ~Observable ()=default |

| void | notifyObservers () |

| Public Member Functions inherited from LazyObject | |

| LazyObject () | |

| ~LazyObject () override=default | |

| void | update () override |

| bool | isCalculated () const |

| void | forwardFirstNotificationOnly () |

| void | alwaysForwardNotifications () |

| void | recalculate () |

| void | freeze () |

| void | unfreeze () |

| Public Member Functions inherited from Observer | |

| Observer ()=default | |

| Observer (const Observer &) | |

| Observer & | operator= (const Observer &) |

| virtual | ~Observer () |

| std::pair< iterator, bool > | registerWith (const ext::shared_ptr< Observable > &) |

| void | registerWithObservables (const ext::shared_ptr< Observer > &) |

| Size | unregisterWith (const ext::shared_ptr< Observable > &) |

| void | unregisterWithAll () |

| virtual void | update ()=0 |

| virtual void | deepUpdate () |

Visitability | |

| ext::shared_ptr< YoYInflationCoupon > | underlying_ |

| bool | isFloored_ |

| bool | isCapped_ |

| Rate | cap_ |

| Rate | floor_ |

| void | accept (AcyclicVisitor &v) override |

| Rate | underlyingRate () const |

| this returns the expected rate before cap and floor are applied More... | |

| bool | isCapped () const |

| bool | isFloored () const |

| void | setPricer (const ext::shared_ptr< YoYInflationCouponPricer > &) |

| virtual QL_DEPRECATED void | setCommon (Rate cap, Rate floor) |

Additional Inherited Members | |

| Public Types inherited from Observer | |

| typedef set_type::iterator | iterator |

| Protected Member Functions inherited from YoYInflationCoupon | |

| bool | checkPricerImpl (const ext::shared_ptr< InflationCouponPricer > &) const override |

| makes sure you were given the correct type of pricer More... | |

| Protected Member Functions inherited from InflationCoupon | |

| Protected Member Functions inherited from LazyObject | |

| virtual void | calculate () const |

| Protected Attributes inherited from YoYInflationCoupon | |

| Real | gearing_ |

| Spread | spread_ |

| Protected Attributes inherited from InflationCoupon | |

| ext::shared_ptr< InflationCouponPricer > | pricer_ |

| ext::shared_ptr< InflationIndex > | index_ |

| Period | observationLag_ |

| DayCounter | dayCounter_ |

| Natural | fixingDays_ |

| Real | rate_ |

| Protected Attributes inherited from Coupon | |

| Date | paymentDate_ |

| Real | nominal_ |

| Date | accrualStartDate_ |

| Date | accrualEndDate_ |

| Date | refPeriodStart_ |

| Date | refPeriodEnd_ |

| Date | exCouponDate_ |

| Real | accrualPeriod_ |

| Protected Attributes inherited from LazyObject | |

| bool | calculated_ = false |

| bool | frozen_ = false |

| bool | alwaysForward_ |

Detailed Description

Capped or floored inflation coupon.

Essentially a copy of the nominal version but taking a different index and a set of pricers (not just one).

The payoff \( P \) of a capped inflation-rate coupon with paysWithin = true is:

\[ P = N \times T \times \min(a L + b, C). \]

where \( N \) is the notional, \( T \) is the accrual time, \( L \) is the inflation rate, \( a \) is its gearing, \( b \) is the spread, and \( C \) and \( F \) the strikes.

The payoff of a floored inflation-rate coupon is:

\[ P = N \times T \times \max(a L + b, F). \]

The payoff of a collared inflation-rate coupon is:

\[ P = N \times T \times \min(\max(a L + b, F), C). \]

If paysWithin = false then the inverse is returned (this provides for instrument cap and caplet prices).

They can be decomposed in the following manner. Decomposition of a capped floating rate coupon when paysWithin = true:

\[ R = \min(a L + b, C) = (a L + b) + \min(C - b - \xi |a| L, 0) \]

where \( \xi = sgn(a) \). Then:

\[ R = (a L + b) + |a| \min(\frac{C - b}{|a|} - \xi L, 0) \]

Definition at line 66 of file capflooredinflationcoupon.hpp.

Constructor & Destructor Documentation

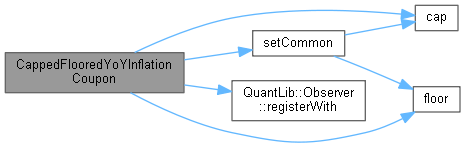

◆ CappedFlooredYoYInflationCoupon() [1/2]

| CappedFlooredYoYInflationCoupon | ( | const ext::shared_ptr< YoYInflationCoupon > & | underlying, |

| Rate | cap = Null<Rate>(), |

||

| Rate | floor = Null<Rate>() |

||

| ) |

Definition at line 57 of file capflooredinflationcoupon.cpp.

Here is the call graph for this function:

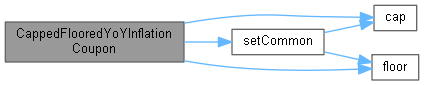

◆ CappedFlooredYoYInflationCoupon() [2/2]

| CappedFlooredYoYInflationCoupon | ( | const Date & | paymentDate, |

| Real | nominal, | ||

| const Date & | startDate, | ||

| const Date & | endDate, | ||

| Natural | fixingDays, | ||

| const ext::shared_ptr< YoYInflationIndex > & | index, | ||

| const Period & | observationLag, | ||

| const DayCounter & | dayCounter, | ||

| Real | gearing = 1.0, |

||

| Spread | spread = 0.0, |

||

| const Rate | cap = Null<Rate>(), |

||

| const Rate | floor = Null<Rate>(), |

||

| const Date & | refPeriodStart = Date(), |

||

| const Date & | refPeriodEnd = Date() |

||

| ) |

Definition at line 75 of file capflooredinflationcoupon.hpp.

Here is the call graph for this function:

Member Function Documentation

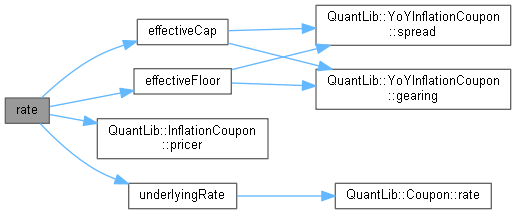

◆ rate()

|

overridevirtual |

swap(let) rate

Implements Coupon.

Definition at line 93 of file capflooredinflationcoupon.cpp.

Here is the call graph for this function:

◆ cap()

| Rate cap | ( | ) | const |

cap

Definition at line 109 of file capflooredinflationcoupon.cpp.

Here is the caller graph for this function:

◆ floor()

| Rate floor | ( | ) | const |

floor

Definition at line 118 of file capflooredinflationcoupon.cpp.

Here is the caller graph for this function:

◆ effectiveCap()

| Rate effectiveCap | ( | ) | const |

effective cap of fixing

Definition at line 127 of file capflooredinflationcoupon.cpp.

Here is the call graph for this function: Here is the caller graph for this function:

Here is the caller graph for this function:

◆ effectiveFloor()

| Rate effectiveFloor | ( | ) | const |

effective floor of fixing

Definition at line 132 of file capflooredinflationcoupon.cpp.

Here is the call graph for this function: Here is the caller graph for this function:

Here is the caller graph for this function:

◆ update()

|

overridevirtual |

This method must be implemented in derived classes. An instance of Observer does not call this method directly: instead, it will be called by the observables the instance registered with when they need to notify any changes.

Implements Observer.

Definition at line 137 of file capflooredinflationcoupon.cpp.

Here is the call graph for this function:

◆ accept()

|

overridevirtual |

Reimplemented from CashFlow.

Definition at line 142 of file capflooredinflationcoupon.cpp.

Here is the call graph for this function:

◆ underlyingRate()

| Rate underlyingRate | ( | ) | const |

this returns the expected rate before cap and floor are applied

Definition at line 89 of file capflooredinflationcoupon.cpp.

Here is the call graph for this function: Here is the caller graph for this function:

Here is the caller graph for this function:

◆ isCapped()

| bool isCapped | ( | ) | const |

Definition at line 125 of file capflooredinflationcoupon.hpp.

◆ isFloored()

| bool isFloored | ( | ) | const |

Definition at line 126 of file capflooredinflationcoupon.hpp.

◆ setPricer()

| void setPricer | ( | const ext::shared_ptr< YoYInflationCouponPricer > & | pricer | ) |

Definition at line 80 of file capflooredinflationcoupon.cpp.

Here is the call graph for this function:

◆ setCommon()

- Deprecated:

- Do not use this method and rely on its being called by the constructor of the base class. If you have overridden it, move the code to the constructor of your derived class. Deprecated in version 1.30.

Definition at line 25 of file capflooredinflationcoupon.cpp.

Here is the call graph for this function: Here is the caller graph for this function:

Here is the caller graph for this function:

Member Data Documentation

◆ underlying_

|

protected |

Definition at line 143 of file capflooredinflationcoupon.hpp.

◆ isFloored_

|

protected |

Definition at line 144 of file capflooredinflationcoupon.hpp.

◆ isCapped_

|

protected |

Definition at line 144 of file capflooredinflationcoupon.hpp.

◆ cap_

|

protected |

Definition at line 145 of file capflooredinflationcoupon.hpp.

◆ floor_

|

protected |

Definition at line 145 of file capflooredinflationcoupon.hpp.