Flat interest-rate curve. More...

#include <flatforward.hpp>

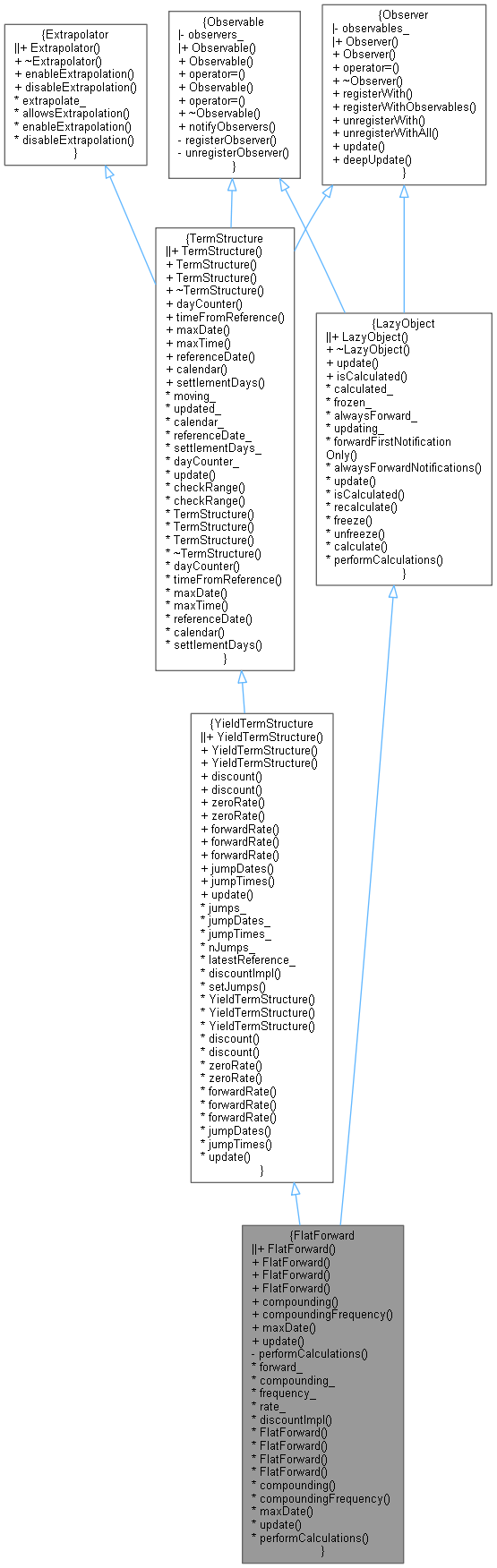

Inheritance diagram for FlatForward:

Inheritance diagram for FlatForward: Collaboration diagram for FlatForward:

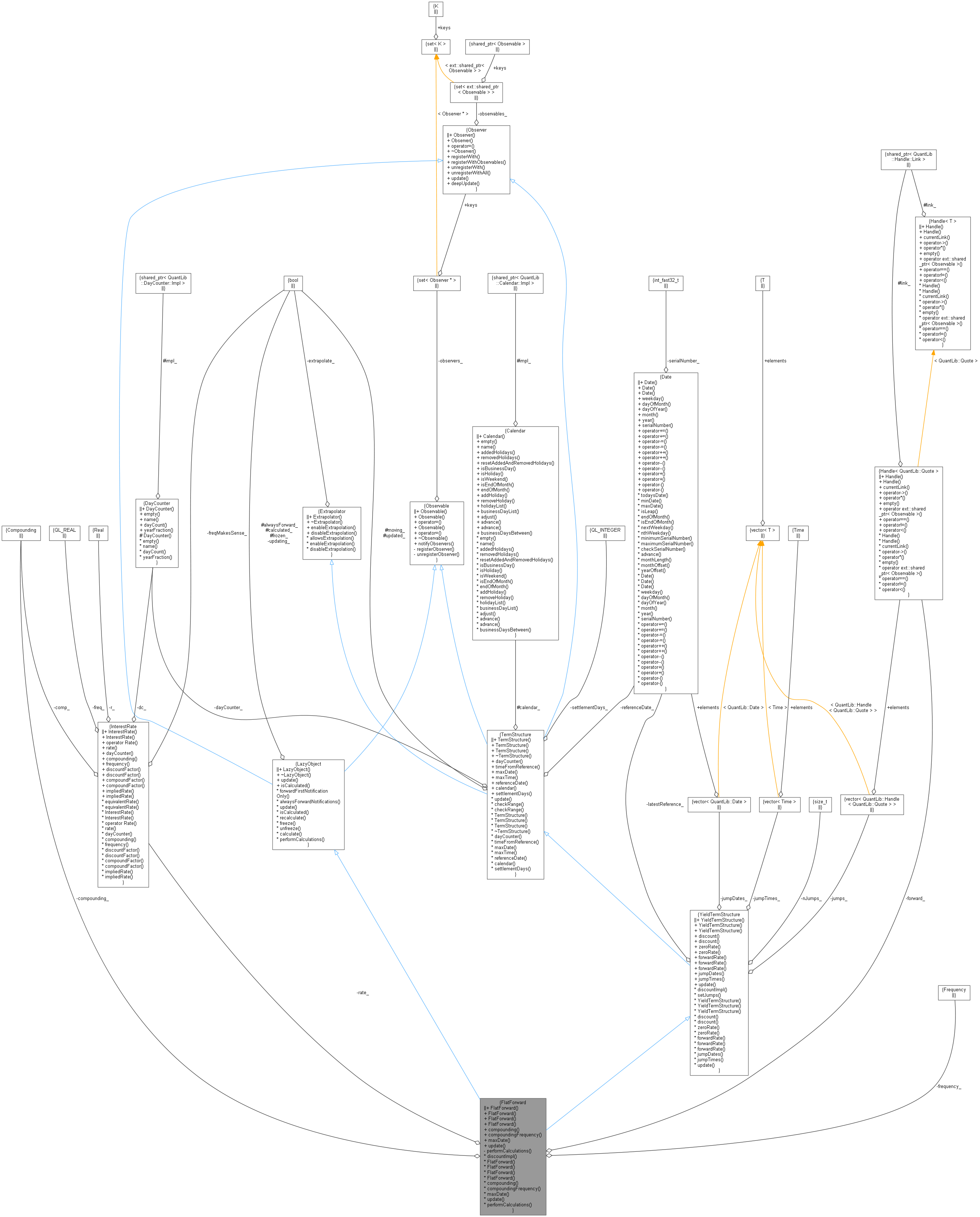

Collaboration diagram for FlatForward:

Public Member Functions | |

Constructors | |

| FlatForward (const Date &referenceDate, Handle< Quote > forward, const DayCounter &dayCounter, Compounding compounding=Continuous, Frequency frequency=Annual) | |

| FlatForward (const Date &referenceDate, Rate forward, const DayCounter &dayCounter, Compounding compounding=Continuous, Frequency frequency=Annual) | |

| FlatForward (Natural settlementDays, const Calendar &calendar, Handle< Quote > forward, const DayCounter &dayCounter, Compounding compounding=Continuous, Frequency frequency=Annual) | |

| FlatForward (Natural settlementDays, const Calendar &calendar, Rate forward, const DayCounter &dayCounter, Compounding compounding=Continuous, Frequency frequency=Annual) | |

| Compounding | compounding () const |

| Frequency | compoundingFrequency () const |

TermStructure interface | |

| Date | maxDate () const override |

| the latest date for which the curve can return values More... | |

Observer interface | |

| void | update () override |

| Public Member Functions inherited from YieldTermStructure | |

| YieldTermStructure (const DayCounter &dc=DayCounter()) | |

| YieldTermStructure (const Date &referenceDate, const Calendar &cal=Calendar(), const DayCounter &dc=DayCounter(), std::vector< Handle< Quote > > jumps={}, const std::vector< Date > &jumpDates={}) | |

| YieldTermStructure (Natural settlementDays, const Calendar &cal, const DayCounter &dc=DayCounter(), std::vector< Handle< Quote > > jumps={}, const std::vector< Date > &jumpDates={}) | |

| DiscountFactor | discount (const Date &d, bool extrapolate=false) const |

| DiscountFactor | discount (Time t, bool extrapolate=false) const |

| InterestRate | zeroRate (const Date &d, const DayCounter &resultDayCounter, Compounding comp, Frequency freq=Annual, bool extrapolate=false) const |

| InterestRate | zeroRate (Time t, Compounding comp, Frequency freq=Annual, bool extrapolate=false) const |

| InterestRate | forwardRate (const Date &d1, const Date &d2, const DayCounter &resultDayCounter, Compounding comp, Frequency freq=Annual, bool extrapolate=false) const |

| InterestRate | forwardRate (const Date &d, const Period &p, const DayCounter &resultDayCounter, Compounding comp, Frequency freq=Annual, bool extrapolate=false) const |

| InterestRate | forwardRate (Time t1, Time t2, Compounding comp, Frequency freq=Annual, bool extrapolate=false) const |

| const std::vector< Date > & | jumpDates () const |

| const std::vector< Time > & | jumpTimes () const |

| void | update () override |

| Public Member Functions inherited from TermStructure | |

| TermStructure (DayCounter dc=DayCounter()) | |

| default constructor More... | |

| TermStructure (const Date &referenceDate, Calendar calendar=Calendar(), DayCounter dc=DayCounter()) | |

| initialize with a fixed reference date More... | |

| TermStructure (Natural settlementDays, Calendar, DayCounter dc=DayCounter()) | |

| calculate the reference date based on the global evaluation date More... | |

| ~TermStructure () override=default | |

| virtual DayCounter | dayCounter () const |

| the day counter used for date/time conversion More... | |

| Time | timeFromReference (const Date &date) const |

| date/time conversion More... | |

| virtual Time | maxTime () const |

| the latest time for which the curve can return values More... | |

| virtual const Date & | referenceDate () const |

| the date at which discount = 1.0 and/or variance = 0.0 More... | |

| virtual Calendar | calendar () const |

| the calendar used for reference and/or option date calculation More... | |

| virtual Natural | settlementDays () const |

| the settlementDays used for reference date calculation More... | |

| Public Member Functions inherited from Observer | |

| Observer ()=default | |

| Observer (const Observer &) | |

| Observer & | operator= (const Observer &) |

| virtual | ~Observer () |

| std::pair< iterator, bool > | registerWith (const ext::shared_ptr< Observable > &) |

| void | registerWithObservables (const ext::shared_ptr< Observer > &) |

| Size | unregisterWith (const ext::shared_ptr< Observable > &) |

| void | unregisterWithAll () |

| virtual void | update ()=0 |

| virtual void | deepUpdate () |

| Public Member Functions inherited from Observable | |

| Observable ()=default | |

| Observable (const Observable &) | |

| Observable & | operator= (const Observable &) |

| Observable (Observable &&)=delete | |

| Observable & | operator= (Observable &&)=delete |

| virtual | ~Observable ()=default |

| void | notifyObservers () |

| Public Member Functions inherited from Extrapolator | |

| Extrapolator ()=default | |

| virtual | ~Extrapolator ()=default |

| void | enableExtrapolation (bool b=true) |

| enable extrapolation in subsequent calls More... | |

| void | disableExtrapolation (bool b=true) |

| disable extrapolation in subsequent calls More... | |

| bool | allowsExtrapolation () const |

| tells whether extrapolation is enabled More... | |

| Public Member Functions inherited from LazyObject | |

| LazyObject () | |

| ~LazyObject () override=default | |

| bool | isCalculated () const |

| void | forwardFirstNotificationOnly () |

| void | alwaysForwardNotifications () |

| void | recalculate () |

| void | freeze () |

| void | unfreeze () |

Private Member Functions | |

LazyObject interface | |

| void | performCalculations () const override |

YieldTermStructure implementation | |

| Handle< Quote > | forward_ |

| Compounding | compounding_ |

| Frequency | frequency_ |

| InterestRate | rate_ |

| DiscountFactor | discountImpl (Time) const override |

| discount factor calculation More... | |

Additional Inherited Members | |

| Public Types inherited from Observer | |

| typedef set_type::iterator | iterator |

| Protected Member Functions inherited from YieldTermStructure | |

| Protected Member Functions inherited from TermStructure | |

| void | checkRange (const Date &d, bool extrapolate) const |

| date-range check More... | |

| void | checkRange (Time t, bool extrapolate) const |

| time-range check More... | |

| Protected Member Functions inherited from LazyObject | |

| virtual void | calculate () const |

| Protected Attributes inherited from TermStructure | |

| bool | moving_ = false |

| bool | updated_ = true |

| Calendar | calendar_ |

| Protected Attributes inherited from LazyObject | |

| bool | calculated_ = false |

| bool | frozen_ = false |

| bool | alwaysForward_ |

Detailed Description

Flat interest-rate curve.

Definition at line 36 of file flatforward.hpp.

Constructor & Destructor Documentation

◆ FlatForward() [1/4]

| FlatForward | ( | const Date & | referenceDate, |

| Handle< Quote > | forward, | ||

| const DayCounter & | dayCounter, | ||

| Compounding | compounding = Continuous, |

||

| Frequency | frequency = Annual |

||

| ) |

◆ FlatForward() [2/4]

| FlatForward | ( | const Date & | referenceDate, |

| Rate | forward, | ||

| const DayCounter & | dayCounter, | ||

| Compounding | compounding = Continuous, |

||

| Frequency | frequency = Annual |

||

| ) |

Definition at line 37 of file flatforward.cpp.

◆ FlatForward() [3/4]

| FlatForward | ( | Natural | settlementDays, |

| const Calendar & | calendar, | ||

| Handle< Quote > | forward, | ||

| const DayCounter & | dayCounter, | ||

| Compounding | compounding = Continuous, |

||

| Frequency | frequency = Annual |

||

| ) |

◆ FlatForward() [4/4]

| FlatForward | ( | Natural | settlementDays, |

| const Calendar & | calendar, | ||

| Rate | forward, | ||

| const DayCounter & | dayCounter, | ||

| Compounding | compounding = Continuous, |

||

| Frequency | frequency = Annual |

||

| ) |

Definition at line 57 of file flatforward.cpp.

Member Function Documentation

◆ compounding()

| Compounding compounding | ( | ) | const |

Definition at line 66 of file flatforward.hpp.

◆ compoundingFrequency()

| Frequency compoundingFrequency | ( | ) | const |

Definition at line 67 of file flatforward.hpp.

◆ maxDate()

|

overridevirtual |

the latest date for which the curve can return values

Implements TermStructure.

Definition at line 71 of file flatforward.hpp.

Here is the call graph for this function:

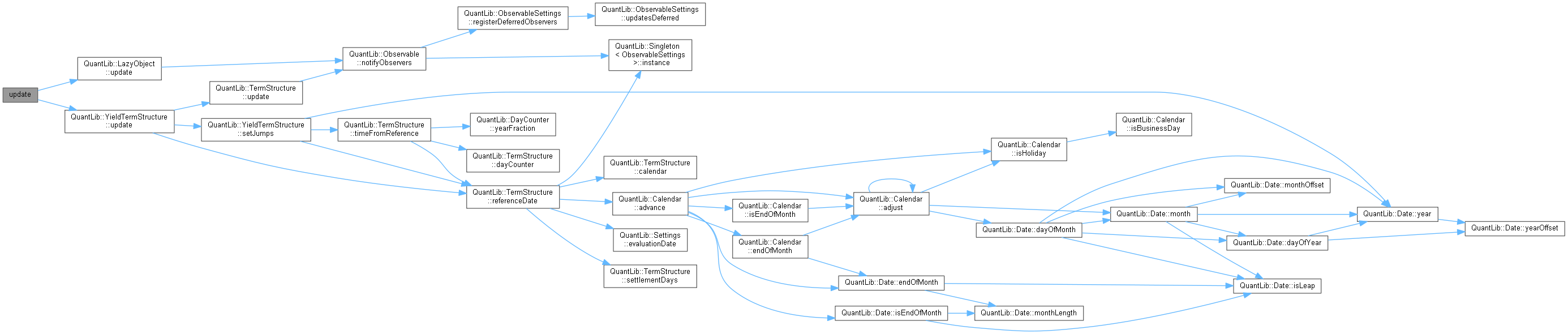

◆ update()

|

overridevirtual |

This method must be implemented in derived classes. An instance of Observer does not call this method directly: instead, it will be called by the observables the instance registered with when they need to notify any changes.

Reimplemented from LazyObject.

Definition at line 97 of file flatforward.hpp.

Here is the call graph for this function:

◆ performCalculations()

|

overrideprivatevirtual |

This method must implement any calculations which must be (re)done in order to calculate the desired results.

Implements LazyObject.

Definition at line 107 of file flatforward.hpp.

Here is the call graph for this function:

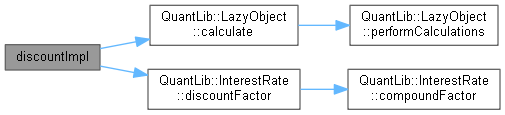

◆ discountImpl()

|

overrideprivatevirtual |

discount factor calculation

Implements YieldTermStructure.

Definition at line 102 of file flatforward.hpp.

Here is the call graph for this function:

Member Data Documentation

◆ forward_

Definition at line 89 of file flatforward.hpp.

◆ compounding_

|

private |

Definition at line 90 of file flatforward.hpp.

◆ frequency_

|

private |

Definition at line 91 of file flatforward.hpp.

◆ rate_

|

mutableprivate |

Definition at line 92 of file flatforward.hpp.