Concrete interest rate class. More...

#include <interestrate.hpp>

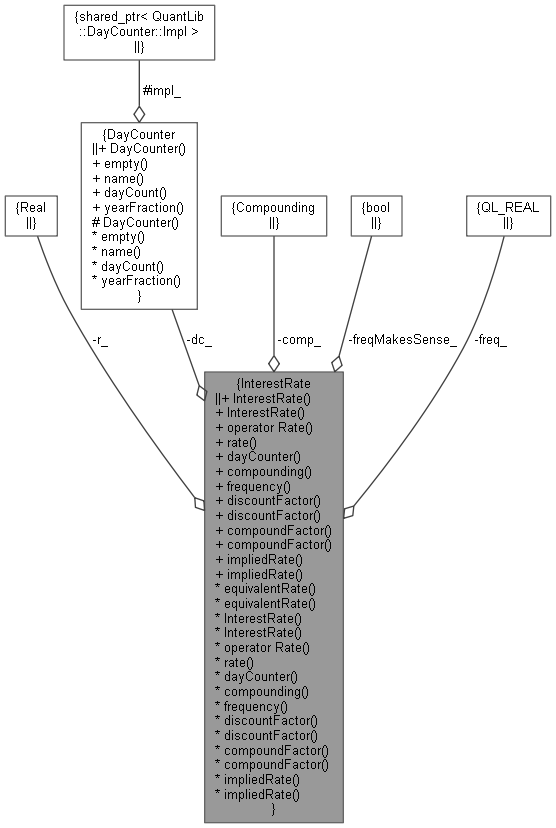

Collaboration diagram for InterestRate:

Collaboration diagram for InterestRate:

Public Member Functions | |

constructors | |

| InterestRate () | |

| Default constructor returning a null interest rate. More... | |

| InterestRate (Rate r, DayCounter dc, Compounding comp, Frequency freq) | |

| Standard constructor. More... | |

conversions | |

| operator Rate () const | |

inspectors | |

| Rate | rate () const |

| const DayCounter & | dayCounter () const |

| Compounding | compounding () const |

| Frequency | frequency () const |

discount/compound factor calculations | |

| DiscountFactor | discountFactor (Time t) const |

| discount factor implied by the rate compounded at time t. More... | |

| DiscountFactor | discountFactor (const Date &d1, const Date &d2, const Date &refStart=Date(), const Date &refEnd=Date()) const |

| discount factor implied by the rate compounded between two dates More... | |

| Real | compoundFactor (Time t) const |

| compound factor implied by the rate compounded at time t. More... | |

| Real | compoundFactor (const Date &d1, const Date &d2, const Date &refStart=Date(), const Date &refEnd=Date()) const |

| compound factor implied by the rate compounded between two dates More... | |

Static Public Member Functions | |

implied rate calculations | |

| static InterestRate | impliedRate (Real compound, const DayCounter &resultDC, Compounding comp, Frequency freq, Time t) |

| implied interest rate for a given compound factor at a given time. More... | |

| static InterestRate | impliedRate (Real compound, const DayCounter &resultDC, Compounding comp, Frequency freq, const Date &d1, const Date &d2, const Date &refStart=Date(), const Date &refEnd=Date()) |

| implied rate for a given compound factor between two dates. More... | |

Related Functions | |

(Note that these are not member functions.) | |

| std::ostream & | operator<< (std::ostream &, const InterestRate &) |

equivalent rate calculations | |

| Rate | r_ |

| DayCounter | dc_ |

| Compounding | comp_ |

| bool | freqMakesSense_ |

| Real | freq_ |

| InterestRate | equivalentRate (Compounding comp, Frequency freq, Time t) const |

| equivalent interest rate for a compounding period t. More... | |

| InterestRate | equivalentRate (const DayCounter &resultDC, Compounding comp, Frequency freq, Date d1, Date d2, const Date &refStart=Date(), const Date &refEnd=Date()) const |

| equivalent rate for a compounding period between two dates More... | |

Detailed Description

Concrete interest rate class.

This class encapsulate the interest rate compounding algebra. It manages day-counting conventions, compounding conventions, conversion between different conventions, discount/compound factor calculations, and implied/equivalent rate calculations.

- Tests:

- Converted rates are checked against known good results

- Examples

- CallableBonds.cpp.

Definition at line 40 of file interestrate.hpp.

Constructor & Destructor Documentation

◆ InterestRate() [1/2]

| InterestRate | ( | ) |

Default constructor returning a null interest rate.

Definition at line 30 of file interestrate.cpp.

Here is the caller graph for this function:

◆ InterestRate() [2/2]

| InterestRate | ( | Rate | r, |

| DayCounter | dc, | ||

| Compounding | comp, | ||

| Frequency | freq | ||

| ) |

Standard constructor.

Definition at line 33 of file interestrate.cpp.

Member Function Documentation

◆ operator Rate()

| operator Rate | ( | ) | const |

Definition at line 51 of file interestrate.hpp.

◆ rate()

| Rate rate | ( | ) | const |

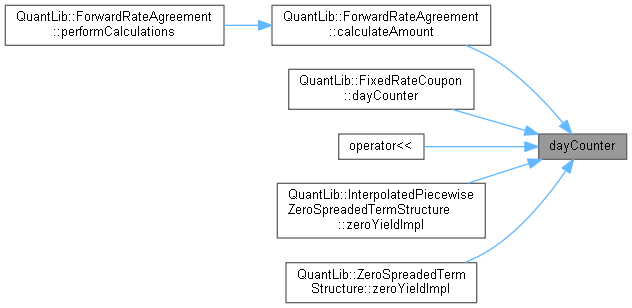

◆ dayCounter()

| const DayCounter & dayCounter | ( | ) | const |

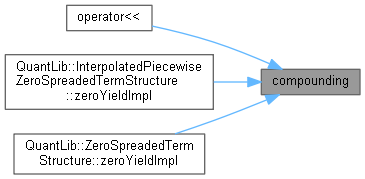

◆ compounding()

| Compounding compounding | ( | ) | const |

◆ frequency()

| Frequency frequency | ( | ) | const |

◆ discountFactor() [1/2]

| DiscountFactor discountFactor | ( | Time | t | ) | const |

discount factor implied by the rate compounded at time t.

- Warning:

- Time must be measured using InterestRate's own day counter.

Definition at line 69 of file interestrate.hpp.

Here is the call graph for this function: Here is the caller graph for this function:

Here is the caller graph for this function:

◆ discountFactor() [2/2]

| DiscountFactor discountFactor | ( | const Date & | d1, |

| const Date & | d2, | ||

| const Date & | refStart = Date(), |

||

| const Date & | refEnd = Date() |

||

| ) | const |

discount factor implied by the rate compounded between two dates

Definition at line 74 of file interestrate.hpp.

Here is the call graph for this function:

◆ compoundFactor() [1/2]

compound factor implied by the rate compounded at time t.

returns the compound (a.k.a capitalization) factor implied by the rate compounded at time t.

- Warning:

- Time must be measured using InterestRate's own day counter.

Definition at line 44 of file interestrate.cpp.

Here is the caller graph for this function:

◆ compoundFactor() [2/2]

| Real compoundFactor | ( | const Date & | d1, |

| const Date & | d2, | ||

| const Date & | refStart = Date(), |

||

| const Date & | refEnd = Date() |

||

| ) | const |

compound factor implied by the rate compounded between two dates

returns the compound (a.k.a capitalization) factor implied by the rate compounded between two dates.

Definition at line 98 of file interestrate.hpp.

Here is the call graph for this function:

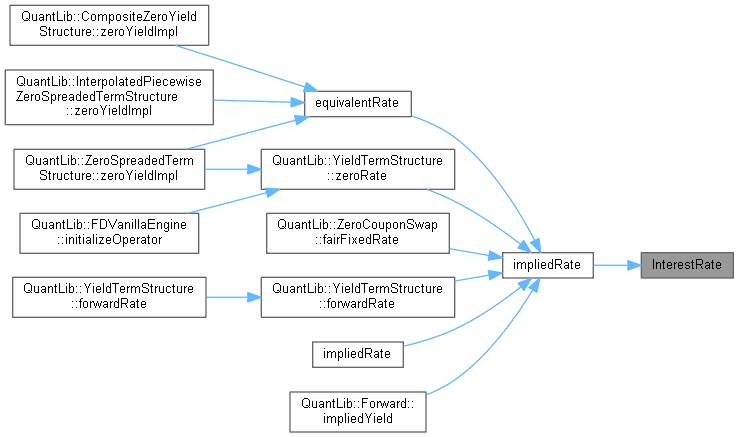

◆ impliedRate() [1/2]

|

static |

implied interest rate for a given compound factor at a given time.

The resulting InterestRate has the day-counter provided as input.

- Warning:

- Time must be measured using the day-counter provided as input.

Definition at line 70 of file interestrate.cpp.

Here is the call graph for this function: Here is the caller graph for this function:

Here is the caller graph for this function:

◆ impliedRate() [2/2]

|

static |

implied rate for a given compound factor between two dates.

The resulting rate is calculated taking the required day-counting rule into account.

Definition at line 129 of file interestrate.hpp.

Here is the call graph for this function:

◆ equivalentRate() [1/2]

| InterestRate equivalentRate | ( | Compounding | comp, |

| Frequency | freq, | ||

| Time | t | ||

| ) | const |

equivalent interest rate for a compounding period t.

The resulting InterestRate shares the same implicit day-counting rule of the original InterestRate instance.

- Warning:

- Time must be measured using the InterestRate's own day counter.

Definition at line 155 of file interestrate.hpp.

Here is the call graph for this function: Here is the caller graph for this function:

Here is the caller graph for this function:

◆ equivalentRate() [2/2]

| InterestRate equivalentRate | ( | const DayCounter & | resultDC, |

| Compounding | comp, | ||

| Frequency | freq, | ||

| Date | d1, | ||

| Date | d2, | ||

| const Date & | refStart = Date(), |

||

| const Date & | refEnd = Date() |

||

| ) | const |

equivalent rate for a compounding period between two dates

The resulting rate is calculated taking the required day-counting rule into account.

Definition at line 165 of file interestrate.hpp.

Here is the call graph for this function:

Friends And Related Function Documentation

◆ operator<<()

|

related |

Member Data Documentation

◆ r_

|

private |

Definition at line 181 of file interestrate.hpp.

◆ dc_

|

private |

Definition at line 182 of file interestrate.hpp.

◆ comp_

|

private |

Definition at line 183 of file interestrate.hpp.

◆ freqMakesSense_

|

private |

Definition at line 184 of file interestrate.hpp.

◆ freq_

|

private |

Definition at line 185 of file interestrate.hpp.