One factor gsr model, formulation is in forward measure. More...

#include <gsr.hpp>

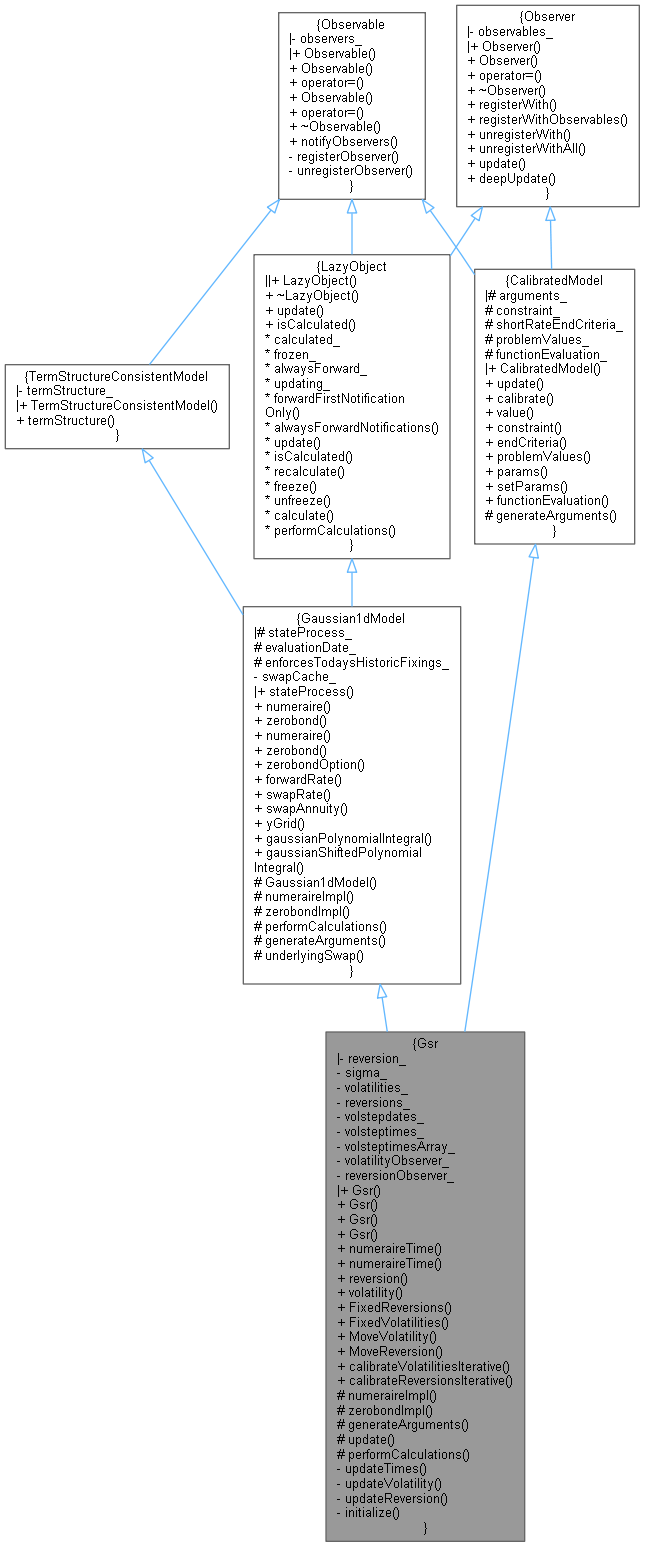

Inheritance diagram for Gsr:

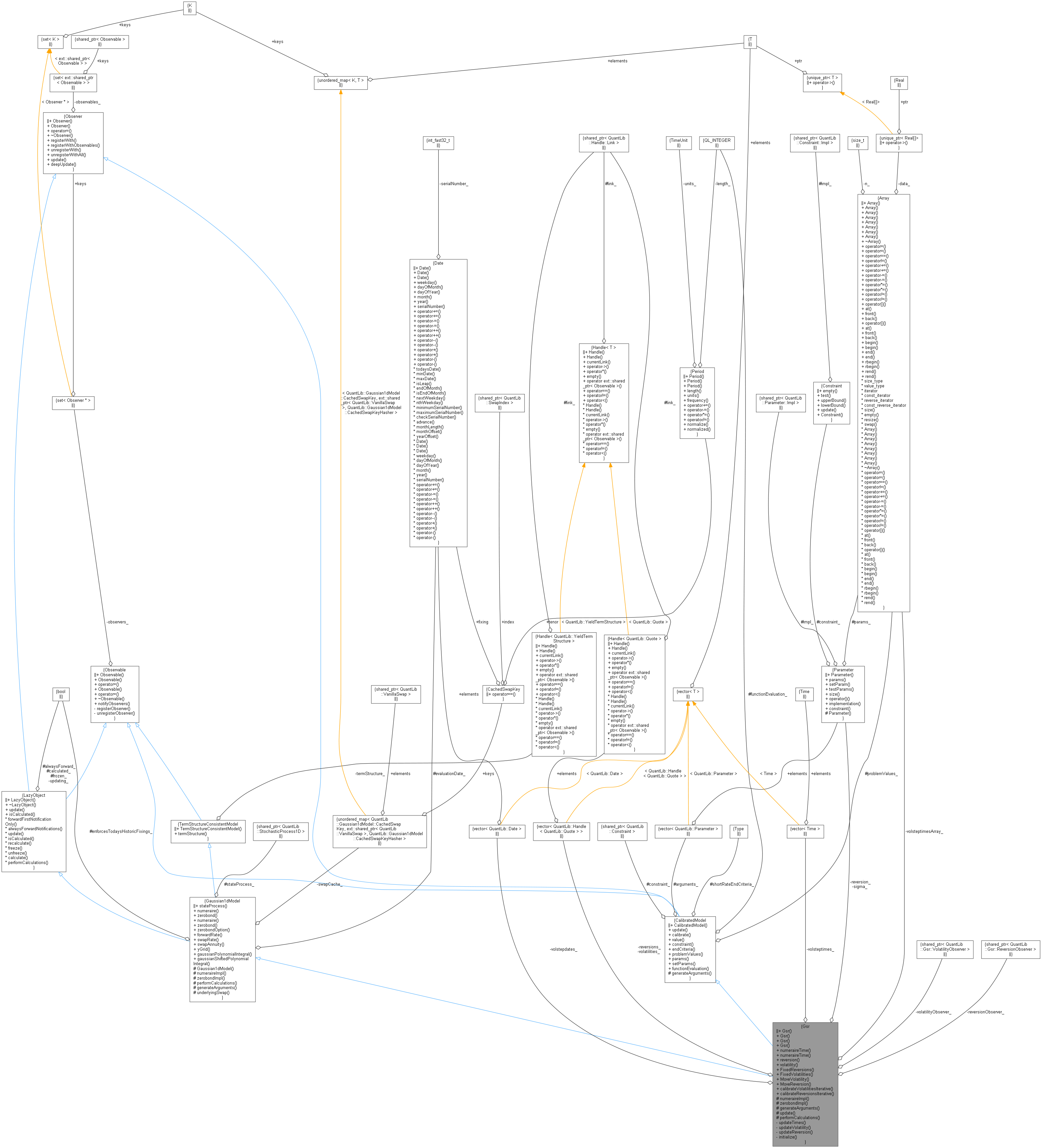

Inheritance diagram for Gsr: Collaboration diagram for Gsr:

Collaboration diagram for Gsr:

Classes | |

| struct | ReversionObserver |

| struct | VolatilityObserver |

Public Member Functions | |

| Gsr (const Handle< YieldTermStructure > &termStructure, std::vector< Date > volstepdates, const std::vector< Real > &volatilities, Real reversion, Real T=60.0) | |

| Gsr (const Handle< YieldTermStructure > &termStructure, std::vector< Date > volstepdates, const std::vector< Real > &volatilities, const std::vector< Real > &reversions, Real T=60.0) | |

| Gsr (const Handle< YieldTermStructure > &termStructure, std::vector< Date > volstepdates, std::vector< Handle< Quote > > volatilities, const Handle< Quote > &reversion, Real T=60.0) | |

| Gsr (const Handle< YieldTermStructure > &termStructure, std::vector< Date > volstepdates, std::vector< Handle< Quote > > volatilities, std::vector< Handle< Quote > > reversions, Real T=60.0) | |

| Real | numeraireTime () const |

| void | numeraireTime (Real T) |

| const Array & | reversion () const |

| const Array & | volatility () const |

| std::vector< bool > | FixedReversions () |

| std::vector< bool > | FixedVolatilities () |

| std::vector< bool > | MoveVolatility (Size i) |

| std::vector< bool > | MoveReversion (Size i) |

| void | calibrateVolatilitiesIterative (const std::vector< ext::shared_ptr< BlackCalibrationHelper > > &helpers, OptimizationMethod &method, const EndCriteria &endCriteria, const Constraint &constraint=Constraint(), const std::vector< Real > &weights=std::vector< Real >()) |

| void | calibrateReversionsIterative (const std::vector< ext::shared_ptr< BlackCalibrationHelper > > &helpers, OptimizationMethod &method, const EndCriteria &endCriteria, const Constraint &constraint=Constraint(), const std::vector< Real > &weights=std::vector< Real >()) |

| Public Member Functions inherited from Gaussian1dModel | |

| ext::shared_ptr< StochasticProcess1D > | stateProcess () const |

| Real | numeraire (Time t, Real y=0.0, const Handle< YieldTermStructure > &yts=Handle< YieldTermStructure >()) const |

| Real | zerobond (Time T, Time t=0.0, Real y=0.0, const Handle< YieldTermStructure > &yts=Handle< YieldTermStructure >()) const |

| Real | numeraire (const Date &referenceDate, Real y=0.0, const Handle< YieldTermStructure > &yts=Handle< YieldTermStructure >()) const |

| Real | zerobond (const Date &maturity, const Date &referenceDate=Date(), Real y=0.0, const Handle< YieldTermStructure > &yts=Handle< YieldTermStructure >()) const |

| Real | zerobondOption (const Option::Type &type, const Date &expiry, const Date &valueDate, const Date &maturity, Rate strike, const Date &referenceDate=Date(), Real y=0.0, const Handle< YieldTermStructure > &yts=Handle< YieldTermStructure >(), Real yStdDevs=7.0, Size yGridPoints=64, bool extrapolatePayoff=true, bool flatPayoffExtrapolation=false) const |

| Real | forwardRate (const Date &fixing, const Date &referenceDate=Date(), Real y=0.0, const ext::shared_ptr< IborIndex > &iborIdx=ext::shared_ptr< IborIndex >()) const |

| Real | swapRate (const Date &fixing, const Period &tenor, const Date &referenceDate=Date(), Real y=0.0, const ext::shared_ptr< SwapIndex > &swapIdx=ext::shared_ptr< SwapIndex >()) const |

| Real | swapAnnuity (const Date &fixing, const Period &tenor, const Date &referenceDate=Date(), Real y=0.0, const ext::shared_ptr< SwapIndex > &swapIdx=ext::shared_ptr< SwapIndex >()) const |

| Array | yGrid (Real yStdDevs, int gridPoints, Real T=1.0, Real t=0, Real y=0) const |

| Public Member Functions inherited from TermStructureConsistentModel | |

| TermStructureConsistentModel (Handle< YieldTermStructure > termStructure) | |

| const Handle< YieldTermStructure > & | termStructure () const |

| Public Member Functions inherited from Observable | |

| Observable ()=default | |

| Observable (const Observable &) | |

| Observable & | operator= (const Observable &) |

| Observable (Observable &&)=delete | |

| Observable & | operator= (Observable &&)=delete |

| virtual | ~Observable ()=default |

| void | notifyObservers () |

| Public Member Functions inherited from LazyObject | |

| LazyObject () | |

| ~LazyObject () override=default | |

| void | update () override |

| bool | isCalculated () const |

| void | forwardFirstNotificationOnly () |

| void | alwaysForwardNotifications () |

| void | recalculate () |

| void | freeze () |

| void | unfreeze () |

| Public Member Functions inherited from Observer | |

| Observer ()=default | |

| Observer (const Observer &) | |

| Observer & | operator= (const Observer &) |

| virtual | ~Observer () |

| std::pair< iterator, bool > | registerWith (const ext::shared_ptr< Observable > &) |

| void | registerWithObservables (const ext::shared_ptr< Observer > &) |

| Size | unregisterWith (const ext::shared_ptr< Observable > &) |

| void | unregisterWithAll () |

| virtual void | update ()=0 |

| virtual void | deepUpdate () |

| Public Member Functions inherited from CalibratedModel | |

| CalibratedModel (Size nArguments) | |

| void | update () override |

| virtual void | calibrate (const std::vector< ext::shared_ptr< CalibrationHelper > > &, OptimizationMethod &method, const EndCriteria &endCriteria, const Constraint &constraint=Constraint(), const std::vector< Real > &weights=std::vector< Real >(), const std::vector< bool > &fixParameters=std::vector< bool >()) |

| Calibrate to a set of market instruments (usually caps/swaptions) More... | |

| Real | value (const Array ¶ms, const std::vector< ext::shared_ptr< CalibrationHelper > > &) |

| const ext::shared_ptr< Constraint > & | constraint () const |

| EndCriteria::Type | endCriteria () const |

| Returns end criteria result. More... | |

| const Array & | problemValues () const |

| Returns the problem values. More... | |

| Array | params () const |

| Returns array of arguments on which calibration is done. More... | |

| virtual void | setParams (const Array ¶ms) |

| Integer | functionEvaluation () const |

Protected Member Functions | |

| Real | numeraireImpl (Time t, Real y, const Handle< YieldTermStructure > &yts) const override |

| Real | zerobondImpl (Time T, Time t, Real y, const Handle< YieldTermStructure > &yts) const override |

| void | generateArguments () override |

| void | update () override |

| void | performCalculations () const override |

| Protected Member Functions inherited from Gaussian1dModel | |

| Gaussian1dModel (const Handle< YieldTermStructure > &yieldTermStructure) | |

| virtual Real | numeraireImpl (Time t, Real y, const Handle< YieldTermStructure > &yts) const =0 |

| virtual Real | zerobondImpl (Time T, Time t, Real y, const Handle< YieldTermStructure > &yts) const =0 |

| void | performCalculations () const override |

| void | generateArguments () |

| ext::shared_ptr< VanillaSwap > | underlyingSwap (const ext::shared_ptr< SwapIndex > &index, const Date &expiry, const Period &tenor) const |

| Protected Member Functions inherited from LazyObject | |

| virtual void | calculate () const |

| virtual void | generateArguments () |

Private Member Functions | |

| void | updateTimes () const |

| void | updateVolatility () |

| void | updateReversion () |

| void | initialize (Real) |

Private Attributes | |

| Parameter & | reversion_ |

| Parameter & | sigma_ |

| std::vector< Handle< Quote > > | volatilities_ |

| std::vector< Handle< Quote > > | reversions_ |

| std::vector< Date > | volstepdates_ |

| std::vector< Time > | volsteptimes_ |

| Array | volsteptimesArray_ |

| ext::shared_ptr< VolatilityObserver > | volatilityObserver_ |

| ext::shared_ptr< ReversionObserver > | reversionObserver_ |

Additional Inherited Members | |

| Public Types inherited from Observer | |

| typedef set_type::iterator | iterator |

| Static Public Member Functions inherited from Gaussian1dModel | |

| static Real | gaussianPolynomialIntegral (Real a, Real b, Real c, Real d, Real e, Real x0, Real x1) |

| static Real | gaussianShiftedPolynomialIntegral (Real a, Real b, Real c, Real d, Real e, Real h, Real x0, Real x1) |

| Protected Attributes inherited from Gaussian1dModel | |

| ext::shared_ptr< StochasticProcess1D > | stateProcess_ |

| Date | evaluationDate_ |

| bool | enforcesTodaysHistoricFixings_ |

| Protected Attributes inherited from LazyObject | |

| bool | calculated_ = false |

| bool | frozen_ = false |

| bool | alwaysForward_ |

| Protected Attributes inherited from CalibratedModel | |

| std::vector< Parameter > | arguments_ |

| ext::shared_ptr< Constraint > | constraint_ |

| EndCriteria::Type | shortRateEndCriteria_ = EndCriteria::None |

| Array | problemValues_ |

| Integer | functionEvaluation_ |

Detailed Description

Constructor & Destructor Documentation

◆ Gsr() [1/4]

◆ Gsr() [2/4]

◆ Gsr() [3/4]

◆ Gsr() [4/4]

Member Function Documentation

◆ numeraireTime() [1/2]

◆ numeraireTime() [2/2]

◆ reversion()

| const Array & reversion | ( | ) | const |

◆ volatility()

| const Array & volatility | ( | ) | const |

◆ FixedReversions()

◆ FixedVolatilities()

◆ MoveVolatility()

◆ MoveReversion()

◆ calibrateVolatilitiesIterative()

| void calibrateVolatilitiesIterative | ( | const std::vector< ext::shared_ptr< BlackCalibrationHelper > > & | helpers, |

| OptimizationMethod & | method, | ||

| const EndCriteria & | endCriteria, | ||

| const Constraint & | constraint = Constraint(), |

||

| const std::vector< Real > & | weights = std::vector<Real>() |

||

| ) |

◆ calibrateReversionsIterative()

| void calibrateReversionsIterative | ( | const std::vector< ext::shared_ptr< BlackCalibrationHelper > > & | helpers, |

| OptimizationMethod & | method, | ||

| const EndCriteria & | endCriteria, | ||

| const Constraint & | constraint = Constraint(), |

||

| const std::vector< Real > & | weights = std::vector<Real>() |

||

| ) |

◆ numeraireImpl()

|

overrideprotectedvirtual |

Implements Gaussian1dModel.

Definition at line 204 of file gsr.cpp.

Here is the call graph for this function:

◆ zerobondImpl()

|

overrideprotectedvirtual |

Implements Gaussian1dModel.

Definition at line 180 of file gsr.cpp.

Here is the call graph for this function:

◆ generateArguments()

|

overrideprotectedvirtual |

Reimplemented from CalibratedModel.

Definition at line 144 of file gsr.hpp.

Here is the call graph for this function:

◆ update()

|

overrideprotectedvirtual |

This method must be implemented in derived classes. An instance of Observer does not call this method directly: instead, it will be called by the observables the instance registered with when they need to notify any changes.

Reimplemented from CalibratedModel.

Definition at line 92 of file gsr.cpp.

Here is the call graph for this function: Here is the caller graph for this function:

Here is the caller graph for this function:

◆ performCalculations()

|

overrideprotectedvirtual |

This method must implement any calculations which must be (re)done in order to calculate the desired results.

Reimplemented from Gaussian1dModel.

Definition at line 151 of file gsr.hpp.

Here is the call graph for this function:

◆ updateTimes()

|

private |

◆ updateVolatility()

|

private |

◆ updateReversion()

|

private |

◆ initialize()

|

private |

Member Data Documentation

◆ reversion_

◆ sigma_

◆ volatilities_

◆ reversions_

◆ volstepdates_

◆ volsteptimes_

◆ volsteptimesArray_

◆ volatilityObserver_

|

private |

◆ reversionObserver_

|

private |