Term-structure consistent model class. More...

#include <model.hpp>

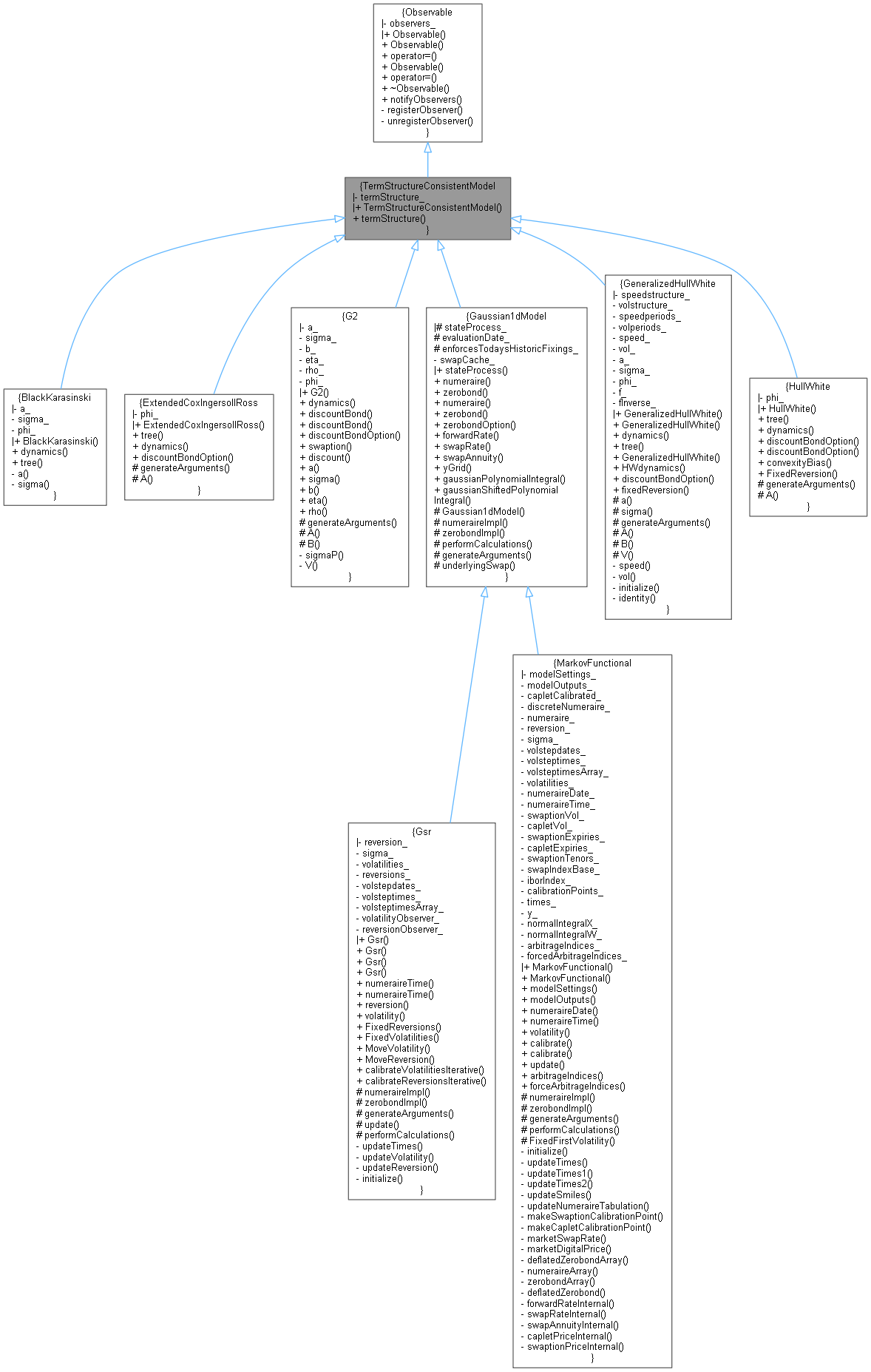

Inheritance diagram for TermStructureConsistentModel:

Inheritance diagram for TermStructureConsistentModel: Collaboration diagram for TermStructureConsistentModel:

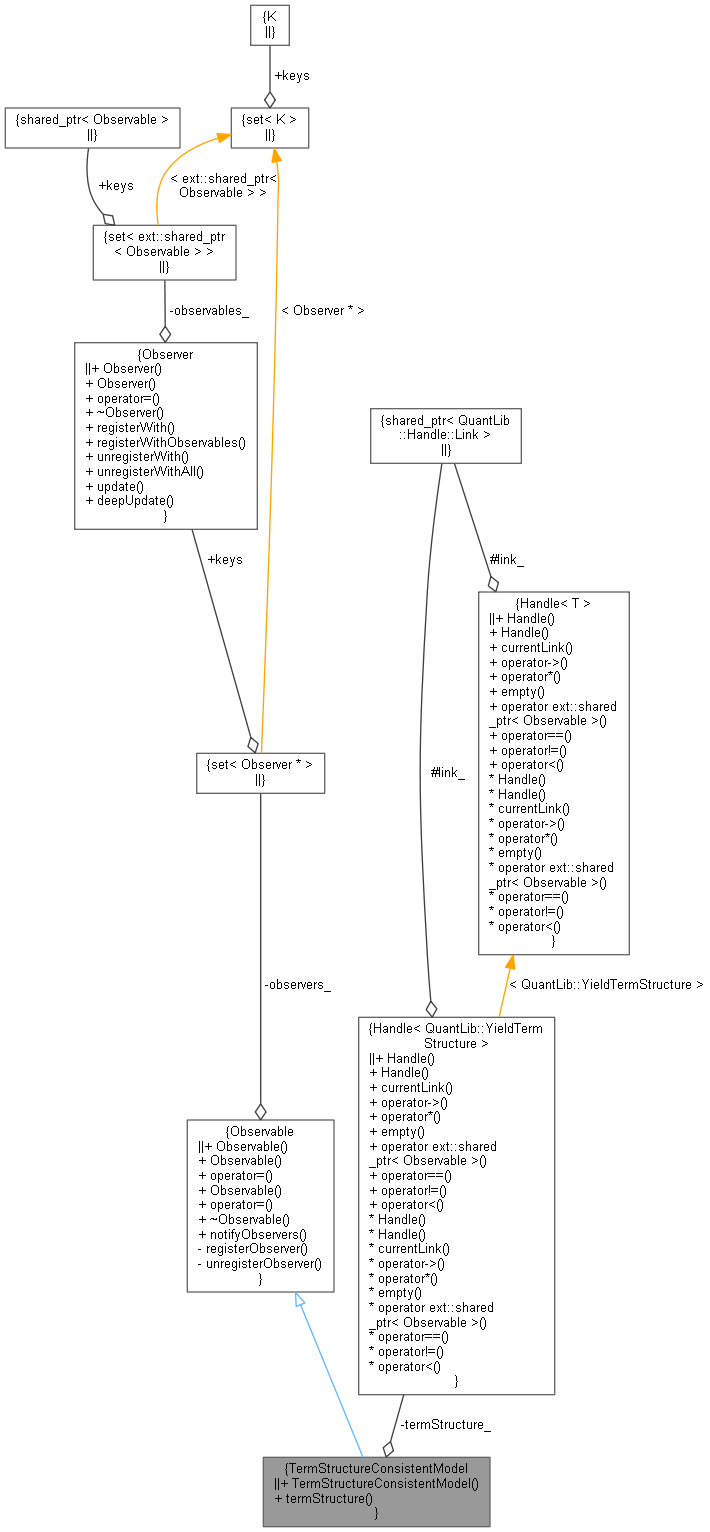

Collaboration diagram for TermStructureConsistentModel:

Public Member Functions | |

| TermStructureConsistentModel (Handle< YieldTermStructure > termStructure) | |

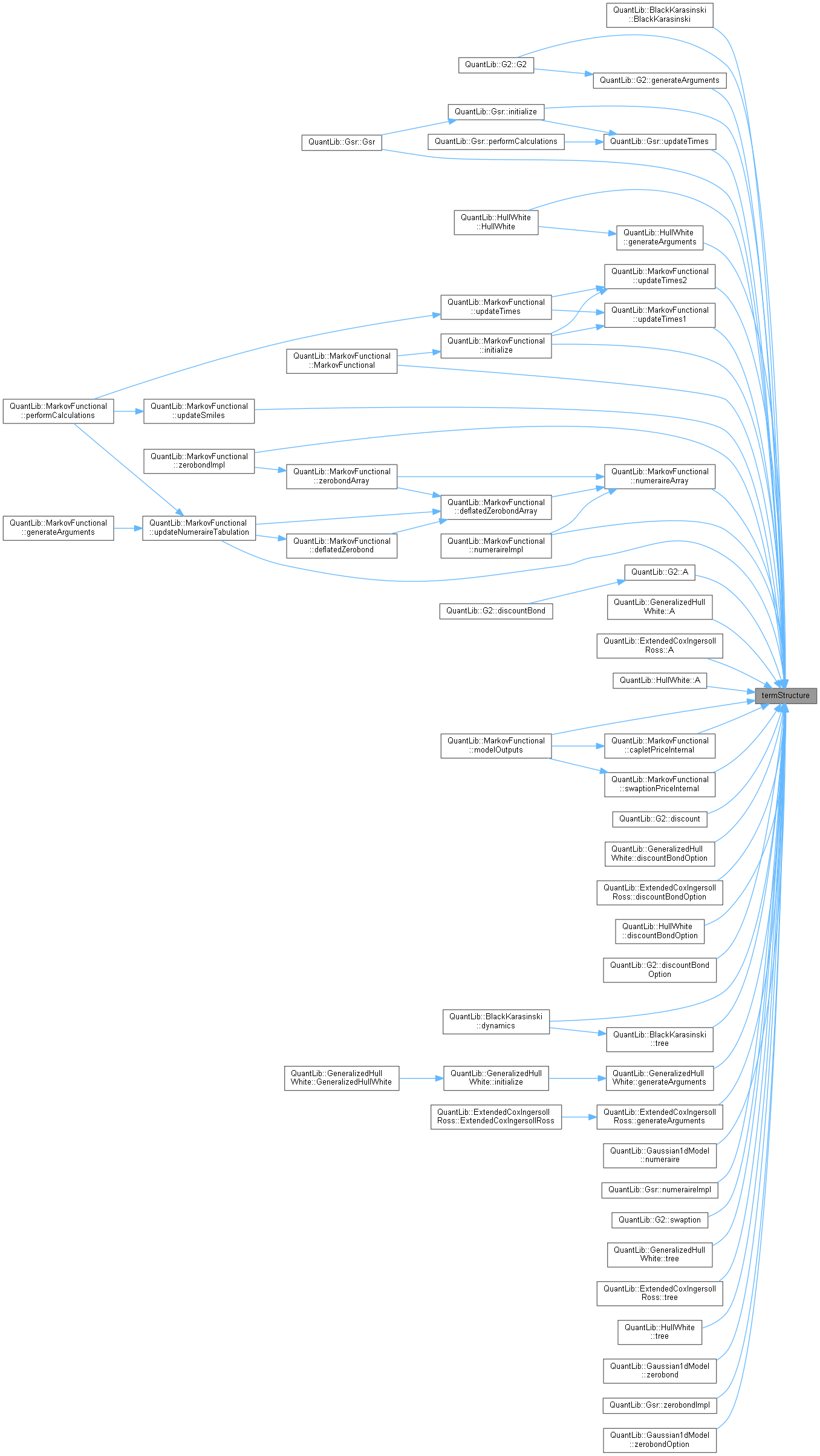

| const Handle< YieldTermStructure > & | termStructure () const |

| Public Member Functions inherited from Observable | |

| Observable ()=default | |

| Observable (const Observable &) | |

| Observable & | operator= (const Observable &) |

| Observable (Observable &&)=delete | |

| Observable & | operator= (Observable &&)=delete |

| virtual | ~Observable ()=default |

| void | notifyObservers () |

Private Attributes | |

| Handle< YieldTermStructure > | termStructure_ |

Detailed Description

Term-structure consistent model class.

This is a base class for models that can reprice exactly any discount bond.

Constructor & Destructor Documentation

◆ TermStructureConsistentModel()

| TermStructureConsistentModel | ( | Handle< YieldTermStructure > | termStructure | ) |

Member Function Documentation

◆ termStructure()

| const Handle< YieldTermStructure > & termStructure | ( | ) | const |

Member Data Documentation

◆ termStructure_

|

private |