template base class for option pricing engines More...

#include <pricingengine.hpp>

Inheritance diagram for GenericEngine< ArgumentsType, ResultsType >:

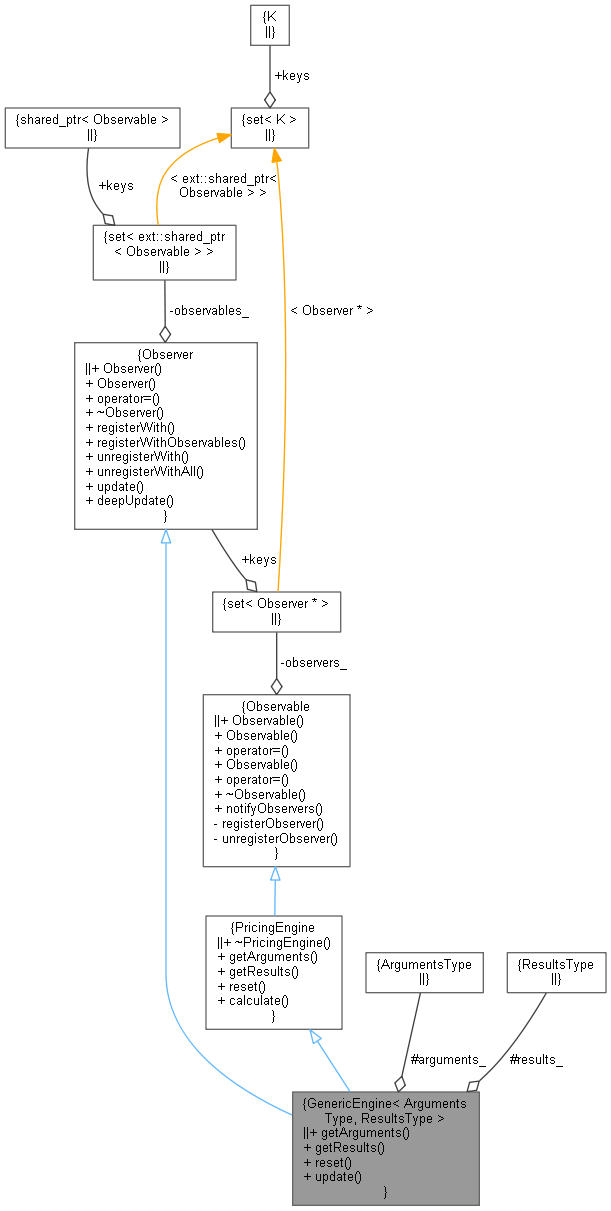

Inheritance diagram for GenericEngine< ArgumentsType, ResultsType >: Collaboration diagram for GenericEngine< ArgumentsType, ResultsType >:

Collaboration diagram for GenericEngine< ArgumentsType, ResultsType >:

Public Member Functions | |

| PricingEngine::arguments * | getArguments () const override |

| const PricingEngine::results * | getResults () const override |

| void | reset () override |

| void | update () override |

| Public Member Functions inherited from PricingEngine | |

| ~PricingEngine () override=default | |

| virtual arguments * | getArguments () const =0 |

| virtual const results * | getResults () const =0 |

| virtual void | reset ()=0 |

| virtual void | calculate () const =0 |

| Public Member Functions inherited from Observable | |

| Observable ()=default | |

| Observable (const Observable &) | |

| Observable & | operator= (const Observable &) |

| Observable (Observable &&)=delete | |

| Observable & | operator= (Observable &&)=delete |

| virtual | ~Observable ()=default |

| void | notifyObservers () |

| Public Member Functions inherited from Observer | |

| Observer ()=default | |

| Observer (const Observer &) | |

| Observer & | operator= (const Observer &) |

| virtual | ~Observer () |

| std::pair< iterator, bool > | registerWith (const ext::shared_ptr< Observable > &) |

| void | registerWithObservables (const ext::shared_ptr< Observer > &) |

| Size | unregisterWith (const ext::shared_ptr< Observable > &) |

| void | unregisterWithAll () |

| virtual void | update ()=0 |

| virtual void | deepUpdate () |

Protected Attributes | |

| ArgumentsType | arguments_ |

| ResultsType | results_ |

Additional Inherited Members | |

| Public Types inherited from Observer | |

| typedef set_type::iterator | iterator |

Detailed Description

class QuantLib::GenericEngine< ArgumentsType, ResultsType >

template base class for option pricing engines

Derived engines only need to implement the calculate() method.

Definition at line 63 of file pricingengine.hpp.

Member Function Documentation

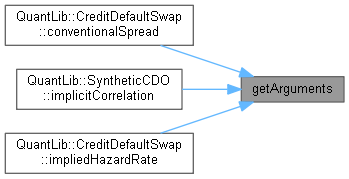

◆ getArguments()

|

overridevirtual |

Implements PricingEngine.

Definition at line 66 of file pricingengine.hpp.

Here is the caller graph for this function:

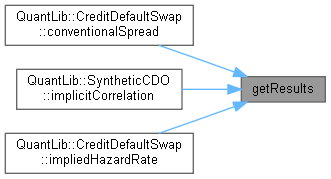

◆ getResults()

|

overridevirtual |

Implements PricingEngine.

Definition at line 67 of file pricingengine.hpp.

Here is the caller graph for this function:

◆ reset()

|

overridevirtual |

Implements PricingEngine.

Definition at line 68 of file pricingengine.hpp.

◆ update()

|

overridevirtual |

This method must be implemented in derived classes. An instance of Observer does not call this method directly: instead, it will be called by the observables the instance registered with when they need to notify any changes.

Implements Observer.

Reimplemented in LatticeShortRateModelEngine< Arguments, Results >, LatticeShortRateModelEngine< CallableBond::arguments, CallableBond::results >, LatticeShortRateModelEngine< CapFloor::arguments, CapFloor::results >, LatticeShortRateModelEngine< Swaption::arguments, Swaption::results >, LatticeShortRateModelEngine< VanillaSwap::arguments, VanillaSwap::results >, AnalyticHestonHullWhiteEngine, COSHestonEngine, FdHestonHullWhiteVanillaEngine, and FdHestonVanillaEngine.

Definition at line 69 of file pricingengine.hpp.

Here is the call graph for this function:

Member Data Documentation

◆ arguments_

|

mutableprotected |

Definition at line 72 of file pricingengine.hpp.

◆ results_

|

mutableprotected |

Definition at line 73 of file pricingengine.hpp.