#include <pricingengine.hpp>

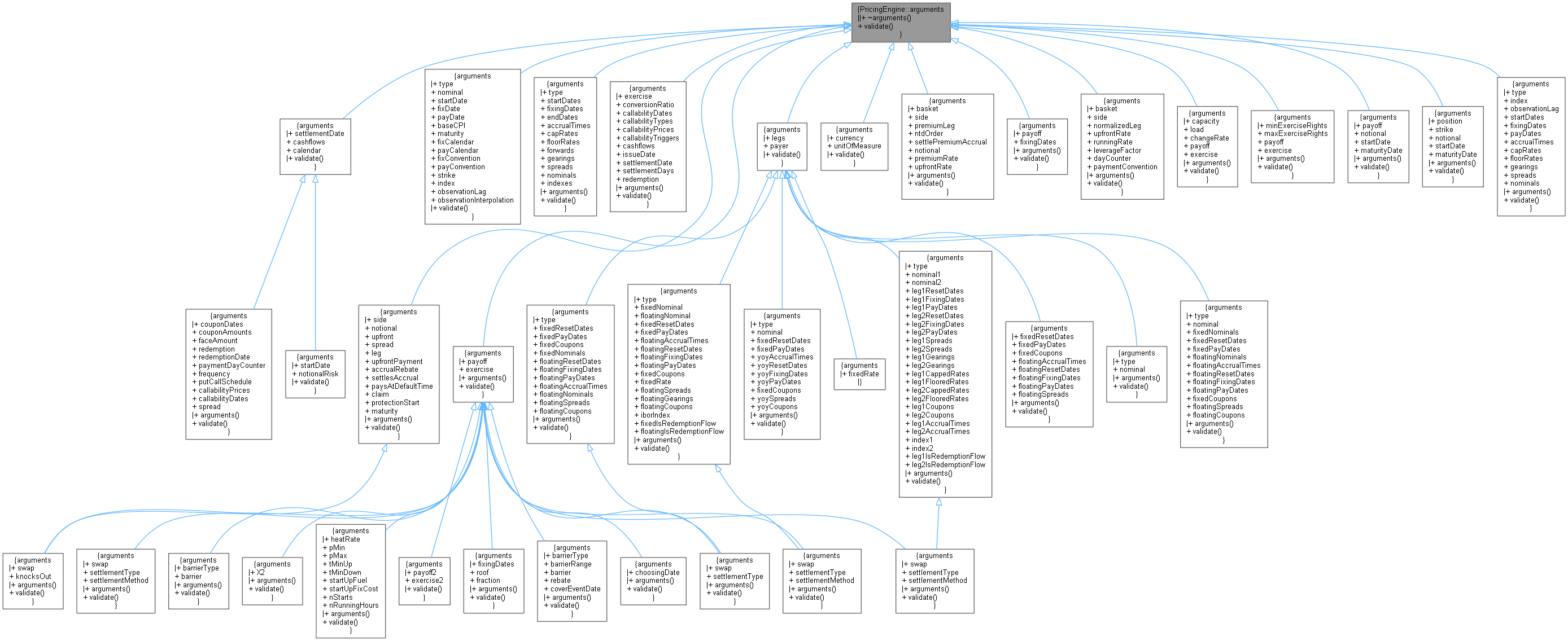

Inheritance diagram for PricingEngine::arguments:

Inheritance diagram for PricingEngine::arguments: Collaboration diagram for PricingEngine::arguments:

Collaboration diagram for PricingEngine::arguments:

Public Member Functions | |

| virtual | ~arguments ()=default |

| virtual void | validate () const =0 |

Detailed Description

Definition at line 45 of file pricingengine.hpp.

Constructor & Destructor Documentation

◆ ~arguments()

|

virtualdefault |

Member Function Documentation

◆ validate()

|

pure virtual |

Implemented in CallableBond::arguments, CatBond::arguments, EnergyCommodity::arguments, CdsOption::arguments, NthToDefault::arguments, SyntheticCDO::arguments, PagodaOption::arguments, VanillaVPPOption::arguments, PathMultiAssetOption::arguments, IrregularSwap::arguments, IrregularSwaption::arguments, VarianceOption::arguments, AssetSwap::arguments, Bond::arguments, ConvertibleBond::arguments, CapFloor::arguments, CPICapFloor::arguments, CPISwap::arguments, CreditDefaultSwap::arguments, FixedVsFloatingSwap::arguments, FloatFloatSwap::arguments, FloatFloatSwaption::arguments, YoYInflationCapFloor::arguments, NonstandardSwap::arguments, NonstandardSwaption::arguments, PartialTimeBarrierOption::arguments, SimpleChooserOption::arguments, Swap::arguments, Swaption::arguments, TwoAssetBarrierOption::arguments, TwoAssetCorrelationOption::arguments, VanillaStorageOption::arguments, VanillaSwingOption::arguments, VarianceSwap::arguments, WriterExtensibleOption::arguments, YearOnYearInflationSwap::arguments, and Option::arguments.

Here is the caller graph for this function: