Base class for CDS helpers. More...

#include <defaultprobabilityhelpers.hpp>

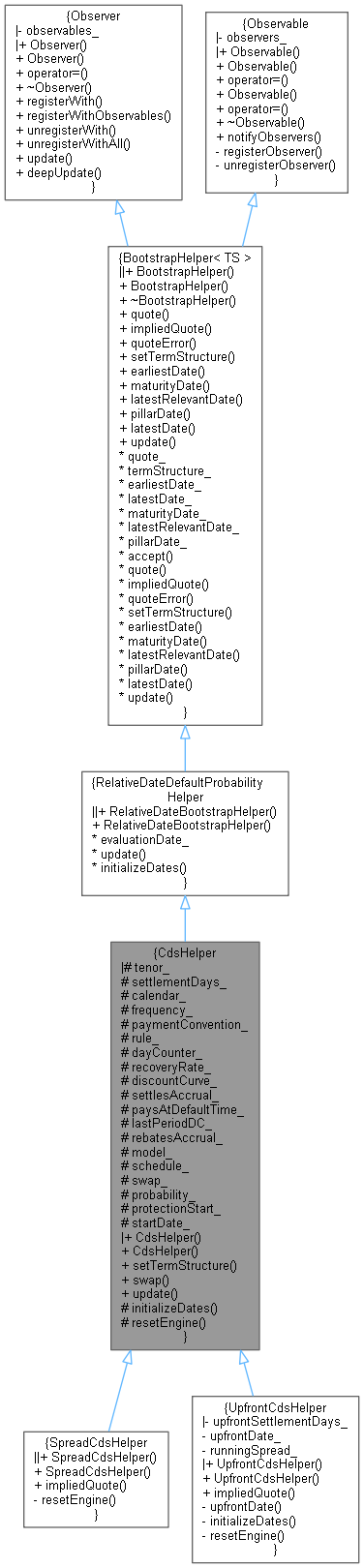

Inheritance diagram for CdsHelper:

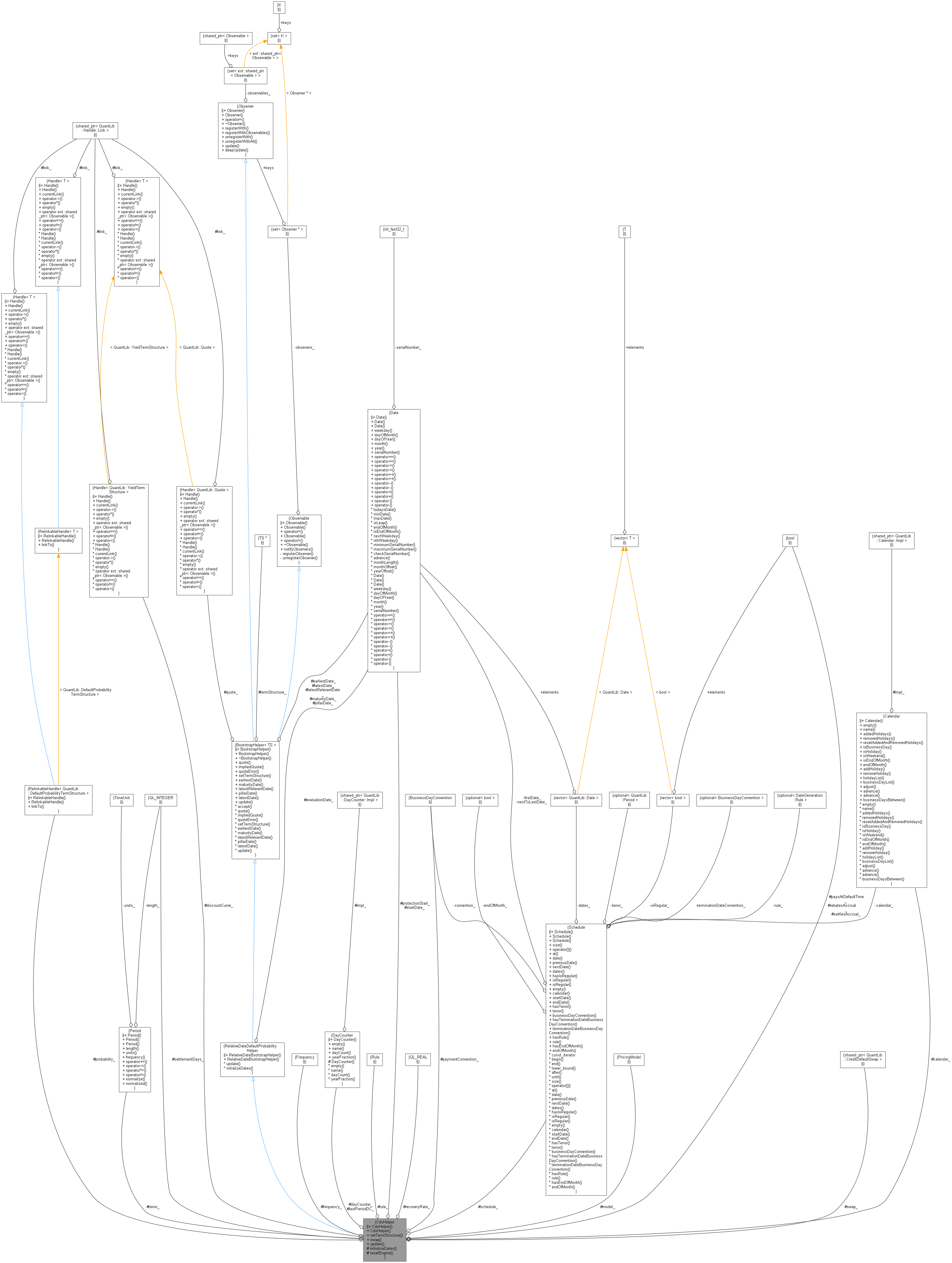

Inheritance diagram for CdsHelper: Collaboration diagram for CdsHelper:

Collaboration diagram for CdsHelper:

Public Member Functions | |

| CdsHelper (const std::variant< Rate, Handle< Quote > > "e, const Period &tenor, Integer settlementDays, Calendar calendar, Frequency frequency, BusinessDayConvention paymentConvention, DateGeneration::Rule rule, DayCounter dayCounter, Real recoveryRate, const Handle< YieldTermStructure > &discountCurve, bool settlesAccrual=true, bool paysAtDefaultTime=true, const Date &startDate=Date(), DayCounter lastPeriodDayCounter=DayCounter(), bool rebatesAccrual=true, CreditDefaultSwap::PricingModel model=CreditDefaultSwap::Midpoint) | |

| void | setTermStructure (DefaultProbabilityTermStructure *) override |

| ext::shared_ptr< CreditDefaultSwap > | swap () const |

| void | update () override |

| Public Member Functions inherited from RelativeDateBootstrapHelper< TS > | |

| RelativeDateBootstrapHelper (const std::variant< Spread, Handle< Quote > > "e, bool updateDates=true) | |

| Public Member Functions inherited from BootstrapHelper< TS > | |

| BootstrapHelper (const std::variant< Spread, Handle< Quote > > "e) | |

| ~BootstrapHelper () override=default | |

| const Handle< Quote > & | quote () const |

| virtual Real | impliedQuote () const =0 |

| Real | quoteError () const |

| virtual void | setTermStructure (TS *) |

| sets the term structure to be used for pricing More... | |

| virtual Date | earliestDate () const |

| earliest relevant date More... | |

| virtual Date | maturityDate () const |

| instrument's maturity date More... | |

| virtual Date | latestRelevantDate () const |

| latest relevant date More... | |

| virtual Date | pillarDate () const |

| pillar date More... | |

| virtual Date | latestDate () const |

| latest date More... | |

| virtual void | accept (AcyclicVisitor &) |

| Public Member Functions inherited from Observer | |

| Observer ()=default | |

| Observer (const Observer &) | |

| Observer & | operator= (const Observer &) |

| virtual | ~Observer () |

| std::pair< iterator, bool > | registerWith (const ext::shared_ptr< Observable > &) |

| void | registerWithObservables (const ext::shared_ptr< Observer > &) |

| Size | unregisterWith (const ext::shared_ptr< Observable > &) |

| void | unregisterWithAll () |

| virtual void | update ()=0 |

| virtual void | deepUpdate () |

| Public Member Functions inherited from Observable | |

| Observable ()=default | |

| Observable (const Observable &) | |

| Observable & | operator= (const Observable &) |

| Observable (Observable &&)=delete | |

| Observable & | operator= (Observable &&)=delete |

| virtual | ~Observable ()=default |

| void | notifyObservers () |

Protected Member Functions | |

| void | initializeDates () override |

| virtual void | resetEngine ()=0 |

| Protected Member Functions inherited from RelativeDateBootstrapHelper< TS > | |

Protected Attributes | |

| Period | tenor_ |

| Integer | settlementDays_ |

| Calendar | calendar_ |

| Frequency | frequency_ |

| BusinessDayConvention | paymentConvention_ |

| DateGeneration::Rule | rule_ |

| DayCounter | dayCounter_ |

| Real | recoveryRate_ |

| Handle< YieldTermStructure > | discountCurve_ |

| bool | settlesAccrual_ |

| bool | paysAtDefaultTime_ |

| DayCounter | lastPeriodDC_ |

| bool | rebatesAccrual_ |

| CreditDefaultSwap::PricingModel | model_ |

| Schedule | schedule_ |

| ext::shared_ptr< CreditDefaultSwap > | swap_ |

| RelinkableHandle< DefaultProbabilityTermStructure > | probability_ |

| Date | protectionStart_ |

| protection effective date. More... | |

| Date | startDate_ |

| Protected Attributes inherited from RelativeDateBootstrapHelper< TS > | |

| Date | evaluationDate_ |

| bool | updateDates_ |

| Protected Attributes inherited from BootstrapHelper< TS > | |

| Handle< Quote > | quote_ |

| TS * | termStructure_ |

| Date | earliestDate_ |

| Date | latestDate_ |

| Date | maturityDate_ |

| Date | latestRelevantDate_ |

| Date | pillarDate_ |

Additional Inherited Members | |

| Public Types inherited from Observer | |

| typedef set_type::iterator | iterator |

Detailed Description

Base class for CDS helpers.

Definition at line 48 of file defaultprobabilityhelpers.hpp.

Constructor & Destructor Documentation

◆ CdsHelper()

| CdsHelper | ( | const std::variant< Rate, Handle< Quote > > & | quote, |

| const Period & | tenor, | ||

| Integer | settlementDays, | ||

| Calendar | calendar, | ||

| Frequency | frequency, | ||

| BusinessDayConvention | paymentConvention, | ||

| DateGeneration::Rule | rule, | ||

| DayCounter | dayCounter, | ||

| Real | recoveryRate, | ||

| const Handle< YieldTermStructure > & | discountCurve, | ||

| bool | settlesAccrual = true, |

||

| bool | paysAtDefaultTime = true, |

||

| const Date & | startDate = Date(), |

||

| DayCounter | lastPeriodDayCounter = DayCounter(), |

||

| bool | rebatesAccrual = true, |

||

| CreditDefaultSwap::PricingModel | model = CreditDefaultSwap::Midpoint |

||

| ) |

Constructor taking CDS market quote

- Parameters

-

quote The helper's market quote. tenor CDS tenor. settlementDays The number of days from evaluation date to the start of the protection period. Prior to the CDS Big Bang in 2009, this was typically 1 calendar day. After the CDS Big Bang, this is typically 0 calendar days i.e. protection starts immediately. calendar CDS calendar. Typically weekends only for standard non-JPY CDS and TYO for JPY. frequency Coupon frequency. Typically 3 months for standard CDS. paymentConvention The convention applied to coupons schedules and settlement dates. rule The date generation rule for generating the CDS schedule. Typically, for CDS prior to the Big Bang, OldCDSshould be used. After the Big Bang,CDSwas typical and since 2015CDS2015is standard.dayCounter The day counter for CDS fee leg coupons. Typically it is Actual/360, excluding accrual end, for all but the final coupon period with Actual/360, including accrual end, for the final coupon. The lastPeriodDayCounterbelow allows for this distinction.recoveryRate The recovery rate of the underlying reference entity. discountCurve A handle to the relevant discount curve. settlesAccrual Set to trueif accrued fee is paid on the occurrence of a credit event and set tofalseif it is not. Typically this istrue.paysAtDefaultTime Set to trueif default payment is made at time of credit event or postponed to the end of the coupon period. Typically this istrue.startDate Used to specify an explicit start date for the CDS schedule and the date from which the CDS maturity is calculated via the tenor. Useful for off-the-run index schedules.lastPeriodDayCounter The day counter for the last fee leg coupon. See comment on dayCounter.rebatesAccrual Set to trueif the fee leg accrual is rebated on the cash settlement date. For CDS after the Big Bang, this is typicallytrue.model The pricing model to use for the helper.

Definition at line 32 of file defaultprobabilityhelpers.cpp.

Here is the call graph for this function:

Member Function Documentation

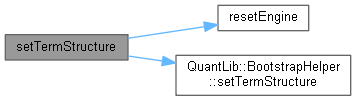

◆ setTermStructure()

|

override |

Definition at line 60 of file defaultprobabilityhelpers.cpp.

Here is the call graph for this function:

◆ swap()

| ext::shared_ptr< CreditDefaultSwap > swap | ( | ) | const |

Definition at line 99 of file defaultprobabilityhelpers.hpp.

◆ update()

|

overridevirtual |

This method must be implemented in derived classes. An instance of Observer does not call this method directly: instead, it will be called by the observables the instance registered with when they need to notify any changes.

Reimplemented from RelativeDateBootstrapHelper< TS >.

Definition at line 70 of file defaultprobabilityhelpers.cpp.

Here is the call graph for this function:

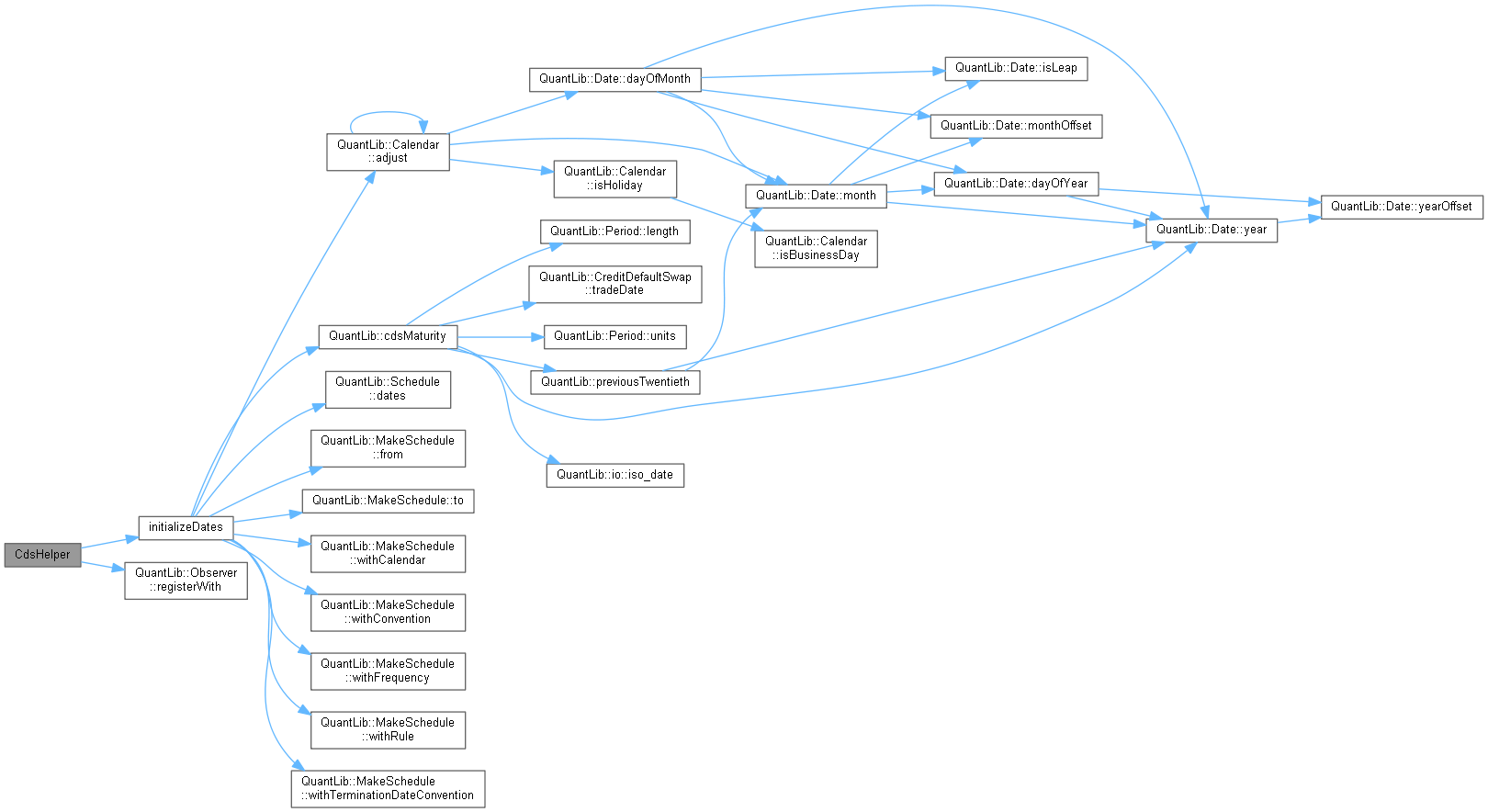

◆ initializeDates()

|

overrideprotectedvirtual |

Implements RelativeDateBootstrapHelper< TS >.

Reimplemented in UpfrontCdsHelper.

Definition at line 75 of file defaultprobabilityhelpers.cpp.

Here is the call graph for this function: Here is the caller graph for this function:

Here is the caller graph for this function:

◆ resetEngine()

|

protectedpure virtual |

Member Data Documentation

◆ tenor_

|

protected |

Definition at line 107 of file defaultprobabilityhelpers.hpp.

◆ settlementDays_

|

protected |

Definition at line 108 of file defaultprobabilityhelpers.hpp.

◆ calendar_

|

protected |

Definition at line 109 of file defaultprobabilityhelpers.hpp.

◆ frequency_

|

protected |

Definition at line 110 of file defaultprobabilityhelpers.hpp.

◆ paymentConvention_

|

protected |

Definition at line 111 of file defaultprobabilityhelpers.hpp.

◆ rule_

|

protected |

Definition at line 112 of file defaultprobabilityhelpers.hpp.

◆ dayCounter_

|

protected |

Definition at line 113 of file defaultprobabilityhelpers.hpp.

◆ recoveryRate_

|

protected |

Definition at line 114 of file defaultprobabilityhelpers.hpp.

◆ discountCurve_

|

protected |

Definition at line 115 of file defaultprobabilityhelpers.hpp.

◆ settlesAccrual_

|

protected |

Definition at line 116 of file defaultprobabilityhelpers.hpp.

◆ paysAtDefaultTime_

|

protected |

Definition at line 117 of file defaultprobabilityhelpers.hpp.

◆ lastPeriodDC_

|

protected |

Definition at line 118 of file defaultprobabilityhelpers.hpp.

◆ rebatesAccrual_

|

protected |

Definition at line 119 of file defaultprobabilityhelpers.hpp.

◆ model_

|

protected |

Definition at line 120 of file defaultprobabilityhelpers.hpp.

◆ schedule_

|

protected |

Definition at line 122 of file defaultprobabilityhelpers.hpp.

◆ swap_

|

protected |

Definition at line 123 of file defaultprobabilityhelpers.hpp.

◆ probability_

|

protected |

Definition at line 124 of file defaultprobabilityhelpers.hpp.

◆ protectionStart_

|

protected |

protection effective date.

Definition at line 126 of file defaultprobabilityhelpers.hpp.

◆ startDate_

|

protected |

Definition at line 127 of file defaultprobabilityhelpers.hpp.