coupon accruing over a fixed period More...

#include <coupon.hpp>

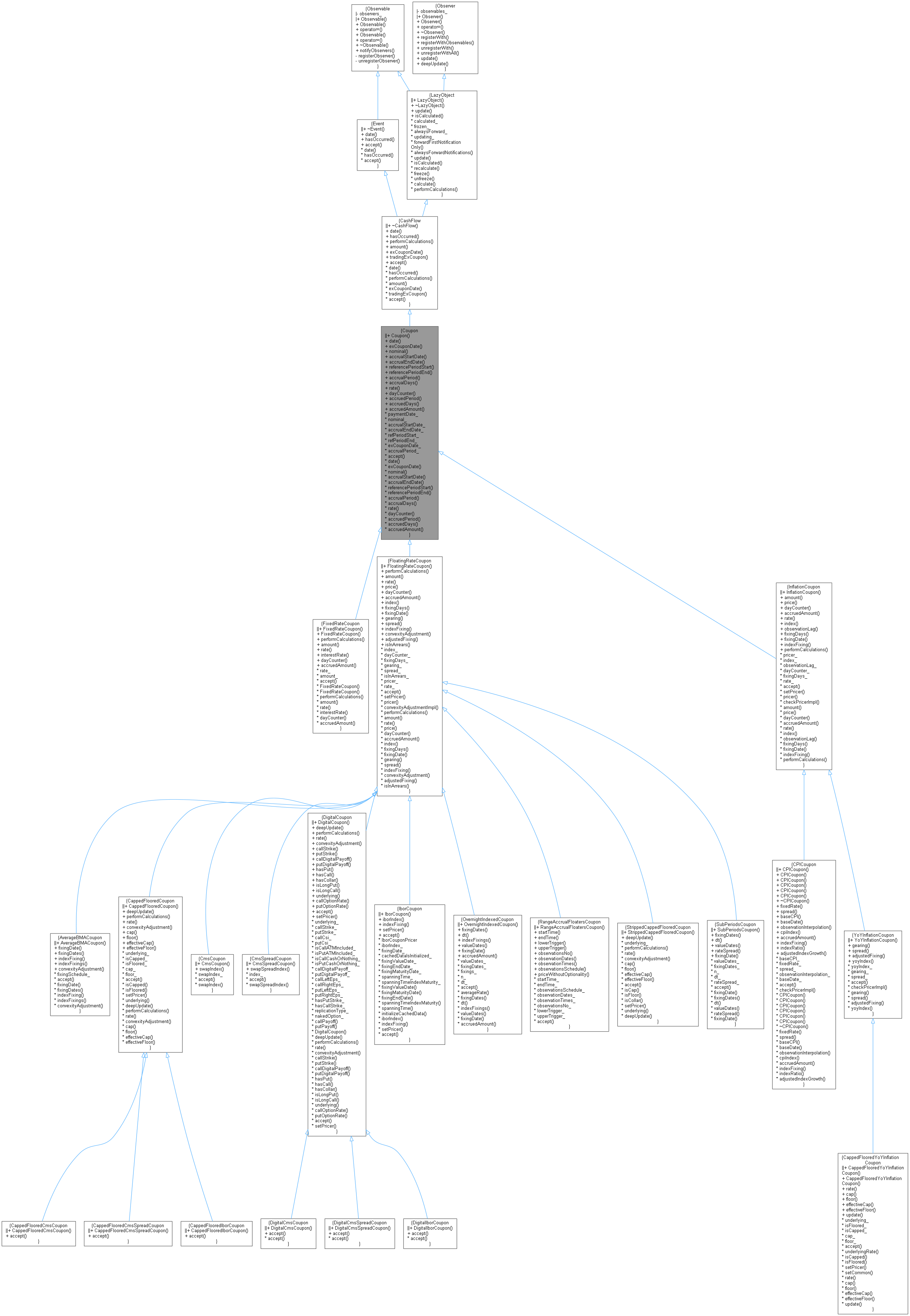

Inheritance diagram for Coupon:

Inheritance diagram for Coupon: Collaboration diagram for Coupon:

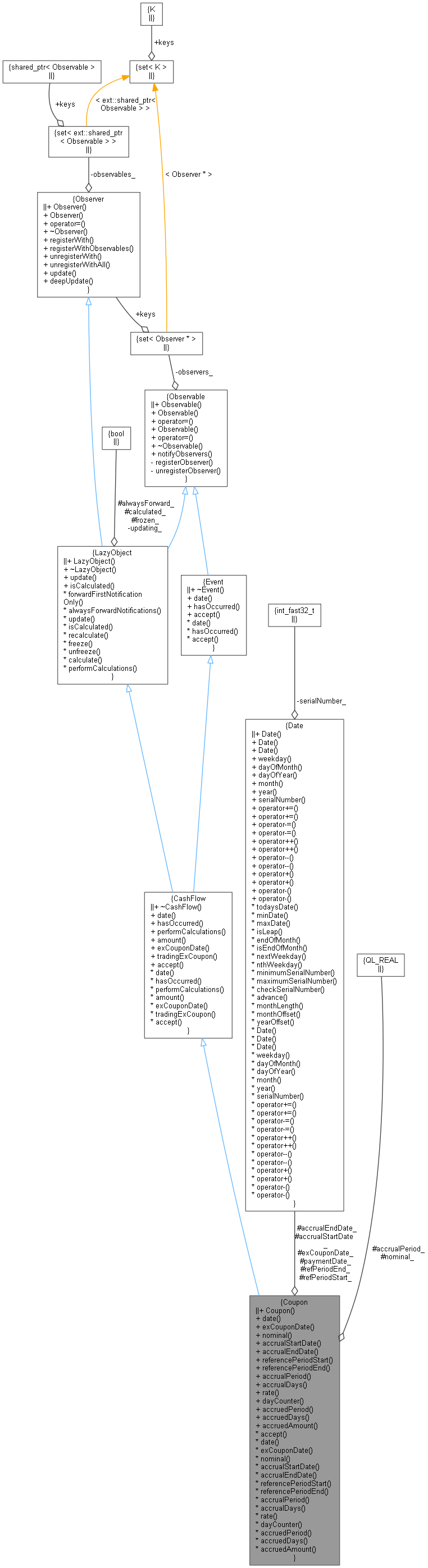

Collaboration diagram for Coupon:

Public Member Functions | |

| Coupon (const Date &paymentDate, Real nominal, const Date &accrualStartDate, const Date &accrualEndDate, const Date &refPeriodStart=Date(), const Date &refPeriodEnd=Date(), const Date &exCouponDate=Date()) | |

Event interface | |

| Date | date () const override |

CashFlow interface | |

| Date | exCouponDate () const override |

| returns the date that the cash flow trades exCoupon More... | |

Inspectors | |

| virtual Real | nominal () const |

| const Date & | accrualStartDate () const |

| start of the accrual period More... | |

| const Date & | accrualEndDate () const |

| end of the accrual period More... | |

| const Date & | referencePeriodStart () const |

| start date of the reference period More... | |

| const Date & | referencePeriodEnd () const |

| end date of the reference period More... | |

| Time | accrualPeriod () const |

| accrual period as fraction of year More... | |

| Date::serial_type | accrualDays () const |

| accrual period in days More... | |

| virtual Rate | rate () const =0 |

| accrued rate More... | |

| virtual DayCounter | dayCounter () const =0 |

| day counter for accrual calculation More... | |

| Time | accruedPeriod (const Date &) const |

| accrued period as fraction of year at the given date More... | |

| Date::serial_type | accruedDays (const Date &) const |

| accrued days at the given date More... | |

| virtual Real | accruedAmount (const Date &) const =0 |

| accrued amount at the given date More... | |

| Public Member Functions inherited from CashFlow | |

| ~CashFlow () override=default | |

| bool | hasOccurred (const Date &refDate=Date(), ext::optional< bool > includeRefDate=ext::nullopt) const override |

| returns true if an event has already occurred before a date More... | |

| void | performCalculations () const override |

| virtual Real | amount () const =0 |

| returns the amount of the cash flow More... | |

| bool | tradingExCoupon (const Date &refDate=Date()) const |

| returns true if the cashflow is trading ex-coupon on the refDate More... | |

| Public Member Functions inherited from Event | |

| ~Event () override=default | |

| Public Member Functions inherited from Observable | |

| Observable ()=default | |

| Observable (const Observable &) | |

| Observable & | operator= (const Observable &) |

| Observable (Observable &&)=delete | |

| Observable & | operator= (Observable &&)=delete |

| virtual | ~Observable ()=default |

| void | notifyObservers () |

| Public Member Functions inherited from LazyObject | |

| LazyObject () | |

| ~LazyObject () override=default | |

| void | update () override |

| bool | isCalculated () const |

| void | forwardFirstNotificationOnly () |

| void | alwaysForwardNotifications () |

| void | recalculate () |

| void | freeze () |

| void | unfreeze () |

| Public Member Functions inherited from Observer | |

| Observer ()=default | |

| Observer (const Observer &) | |

| Observer & | operator= (const Observer &) |

| virtual | ~Observer () |

| std::pair< iterator, bool > | registerWith (const ext::shared_ptr< Observable > &) |

| void | registerWithObservables (const ext::shared_ptr< Observer > &) |

| Size | unregisterWith (const ext::shared_ptr< Observable > &) |

| void | unregisterWithAll () |

| virtual void | update ()=0 |

| virtual void | deepUpdate () |

Visitability | |

| Date | paymentDate_ |

| Real | nominal_ |

| Date | accrualStartDate_ |

| Date | accrualEndDate_ |

| Date | refPeriodStart_ |

| Date | refPeriodEnd_ |

| Date | exCouponDate_ |

| Real | accrualPeriod_ |

| void | accept (AcyclicVisitor &) override |

Additional Inherited Members | |

| Public Types inherited from Observer | |

| typedef set_type::iterator | iterator |

| Protected Member Functions inherited from LazyObject | |

| virtual void | calculate () const |

| Protected Attributes inherited from LazyObject | |

| bool | calculated_ = false |

| bool | frozen_ = false |

| bool | alwaysForward_ |

Detailed Description

coupon accruing over a fixed period

This class implements part of the CashFlow interface but it is still abstract and provides derived classes with methods for accrual period calculations.

Definition at line 39 of file coupon.hpp.

Constructor & Destructor Documentation

◆ Coupon()

| Coupon | ( | const Date & | paymentDate, |

| Real | nominal, | ||

| const Date & | accrualStartDate, | ||

| const Date & | accrualEndDate, | ||

| const Date & | refPeriodStart = Date(), |

||

| const Date & | refPeriodEnd = Date(), |

||

| const Date & | exCouponDate = Date() |

||

| ) |

- Warning:

- the coupon does not adjust the payment date which must already be a business day.

Definition at line 27 of file coupon.cpp.

Member Function Documentation

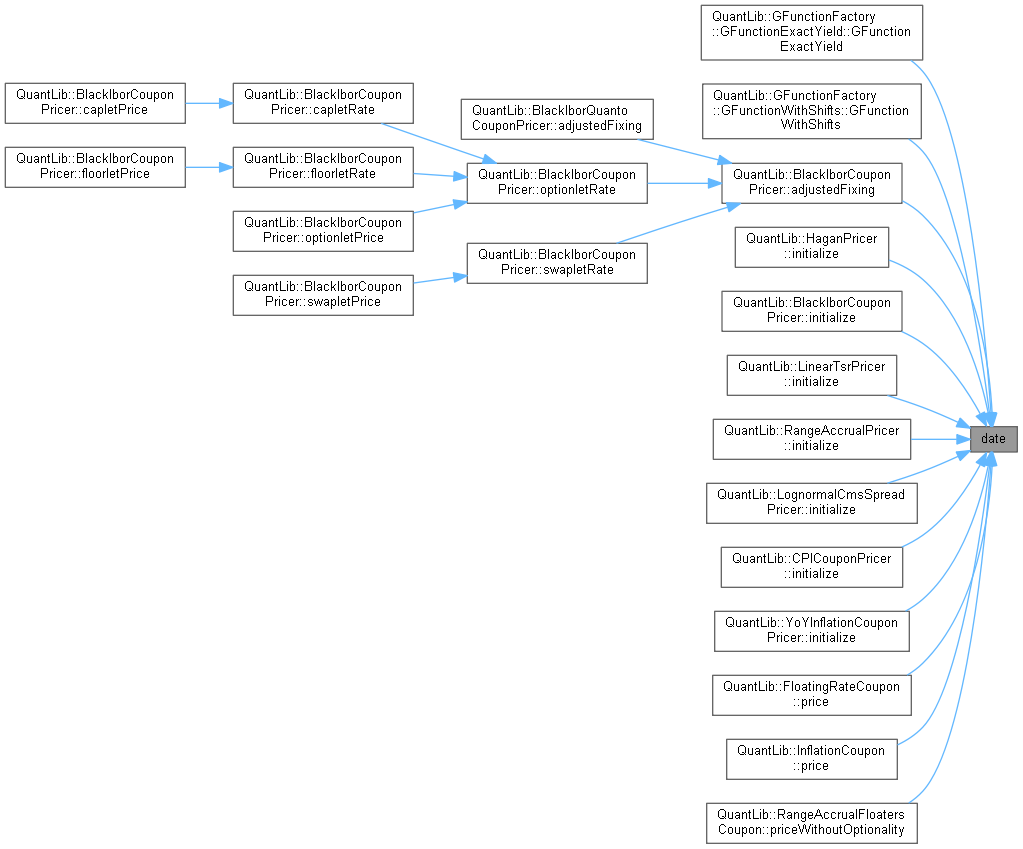

◆ date()

|

overridevirtual |

- Note

- This is inherited from the event class

Implements CashFlow.

Definition at line 53 of file coupon.hpp.

Here is the caller graph for this function:

◆ exCouponDate()

|

overridevirtual |

returns the date that the cash flow trades exCoupon

Reimplemented from CashFlow.

Definition at line 57 of file coupon.hpp.

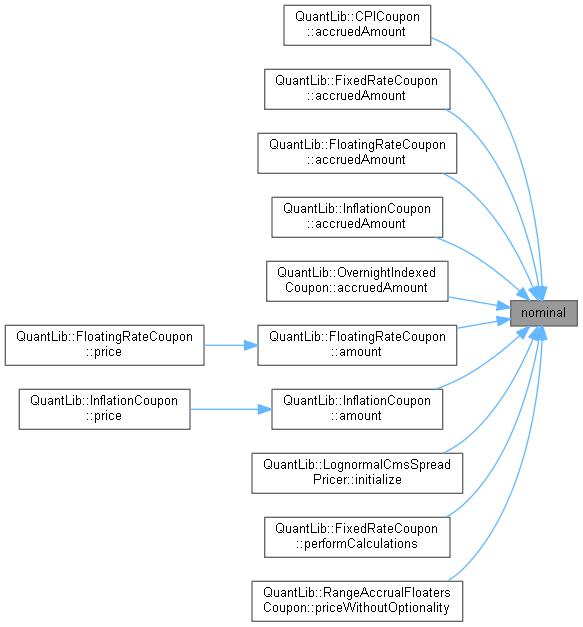

◆ nominal()

|

virtual |

◆ accrualStartDate()

| const Date & accrualStartDate | ( | ) | const |

start of the accrual period

Definition at line 104 of file coupon.hpp.

Here is the caller graph for this function:

◆ accrualEndDate()

| const Date & accrualEndDate | ( | ) | const |

end of the accrual period

Definition at line 108 of file coupon.hpp.

Here is the caller graph for this function:

◆ referencePeriodStart()

| const Date & referencePeriodStart | ( | ) | const |

start date of the reference period

Definition at line 112 of file coupon.hpp.

Here is the caller graph for this function:

◆ referencePeriodEnd()

| const Date & referencePeriodEnd | ( | ) | const |

end date of the reference period

Definition at line 116 of file coupon.hpp.

Here is the caller graph for this function:

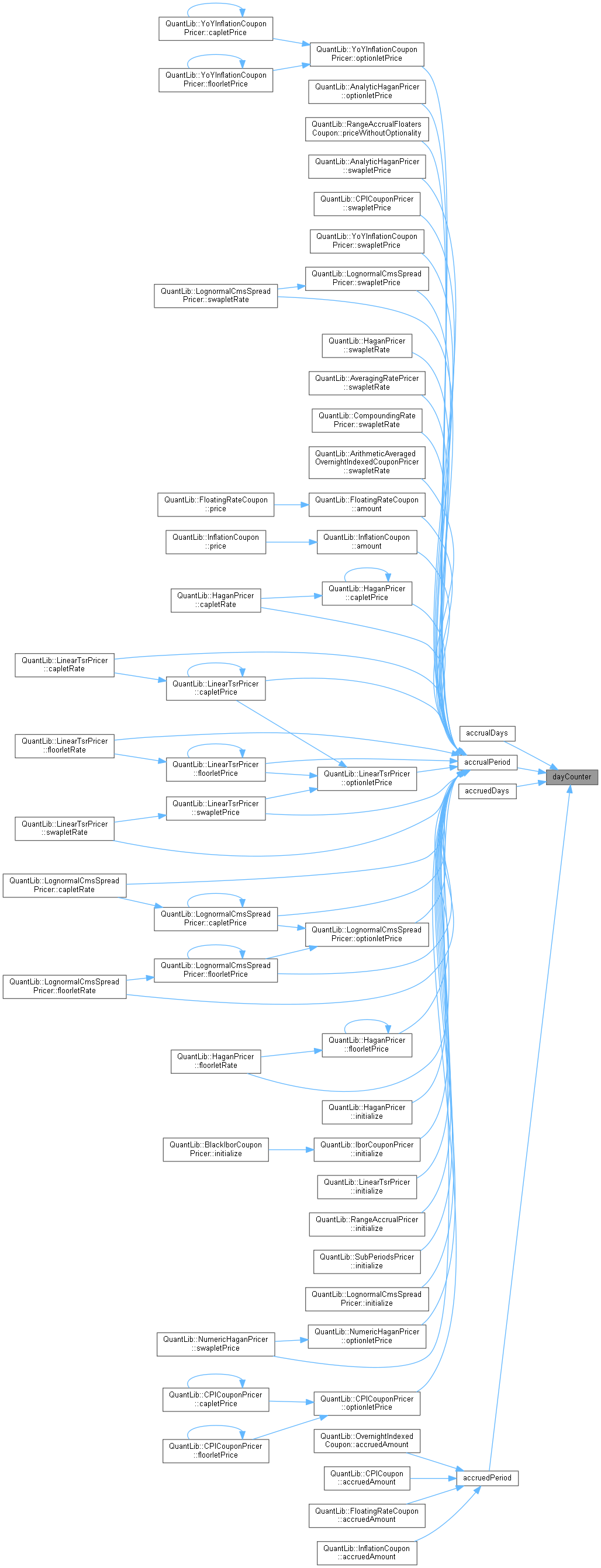

◆ accrualPeriod()

| Time accrualPeriod | ( | ) | const |

accrual period as fraction of year

Definition at line 44 of file coupon.cpp.

Here is the call graph for this function: Here is the caller graph for this function:

Here is the caller graph for this function:

◆ accrualDays()

| Date::serial_type accrualDays | ( | ) | const |

accrual period in days

Definition at line 52 of file coupon.cpp.

Here is the call graph for this function:

◆ rate()

|

pure virtual |

accrued rate

Implemented in CappedFlooredCoupon, CappedFlooredYoYInflationCoupon, DigitalCoupon, FixedRateCoupon, FloatingRateCoupon, InflationCoupon, and StrippedCappedFlooredCoupon.

Here is the caller graph for this function:

◆ dayCounter()

|

pure virtual |

day counter for accrual calculation

Implemented in FixedRateCoupon, FloatingRateCoupon, and InflationCoupon.

Here is the caller graph for this function:

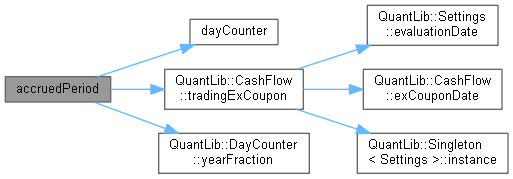

◆ accruedPeriod()

accrued period as fraction of year at the given date

Definition at line 57 of file coupon.cpp.

Here is the call graph for this function: Here is the caller graph for this function:

Here is the caller graph for this function:

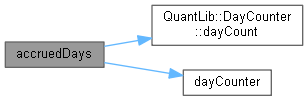

◆ accruedDays()

| Date::serial_type accruedDays | ( | const Date & | d | ) | const |

accrued days at the given date

Definition at line 71 of file coupon.cpp.

Here is the call graph for this function:

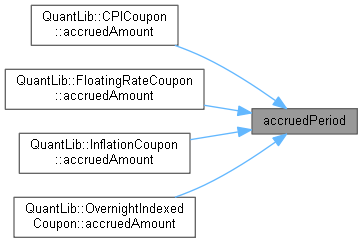

◆ accruedAmount()

accrued amount at the given date

Implemented in CPICoupon, FixedRateCoupon, FloatingRateCoupon, InflationCoupon, and OvernightIndexedCoupon.

◆ accept()

|

overridevirtual |

Reimplemented from CashFlow.

Reimplemented in CPICoupon, DigitalCmsCoupon, DigitalCoupon, DigitalIborCoupon, FixedRateCoupon, FloatingRateCoupon, IborCoupon, InflationCoupon, MultipleResetsCoupon, OvernightIndexedCoupon, RangeAccrualFloatersCoupon, YoYInflationCoupon, CmsSpreadCoupon, DigitalCmsSpreadCoupon, StrippedCappedFlooredCoupon, and CappedFlooredCmsSpreadCoupon.

Definition at line 80 of file coupon.cpp.

Here is the call graph for this function: Here is the caller graph for this function:

Here is the caller graph for this function:

Member Data Documentation

◆ paymentDate_

|

protected |

Definition at line 90 of file coupon.hpp.

◆ nominal_

|

protected |

Definition at line 91 of file coupon.hpp.

◆ accrualStartDate_

|

protected |

Definition at line 92 of file coupon.hpp.

◆ accrualEndDate_

|

protected |

Definition at line 92 of file coupon.hpp.

◆ refPeriodStart_

|

protected |

Definition at line 92 of file coupon.hpp.

◆ refPeriodEnd_

|

protected |

Definition at line 92 of file coupon.hpp.

◆ exCouponDate_

|

protected |

Definition at line 93 of file coupon.hpp.

◆ accrualPeriod_

|

mutableprotected |

Definition at line 94 of file coupon.hpp.