overnight coupon More...

#include <overnightindexedcoupon.hpp>

Inheritance diagram for OvernightIndexedCoupon:

Inheritance diagram for OvernightIndexedCoupon: Collaboration diagram for OvernightIndexedCoupon:

Collaboration diagram for OvernightIndexedCoupon:

Public Member Functions | |

| OvernightIndexedCoupon (const Date &paymentDate, Real nominal, const Date &startDate, const Date &endDate, const ext::shared_ptr< OvernightIndex > &overnightIndex, Real gearing=1.0, Spread spread=0.0, const Date &refPeriodStart=Date(), const Date &refPeriodEnd=Date(), const DayCounter &dayCounter=DayCounter(), bool telescopicValueDates=false, RateAveraging::Type averagingMethod=RateAveraging::Compound, Natural lookbackDays=Null< Natural >(), Natural lockoutDays=0, bool applyObservationShift=false) | |

Inspectors | |

| const std::vector< Date > & | fixingDates () const |

| fixing dates for the rates to be compounded More... | |

| const std::vector< Time > & | dt () const |

| accrual (compounding) periods More... | |

| const std::vector< Rate > & | indexFixings () const |

| fixings to be compounded More... | |

| const std::vector< Date > & | valueDates () const |

| value dates for the rates to be compounded More... | |

| const std::vector< Date > & | interestDates () const |

| interest dates for the rates to be compounded More... | |

| RateAveraging::Type | averagingMethod () const |

| averaging method More... | |

| Natural | lockoutDays () const |

| lockout days More... | |

| bool | applyObservationShift () const |

| apply observation shift More... | |

FloatingRateCoupon interface | |

| Date | fixingDate () const override |

| the date when the coupon is fully determined More... | |

| Real | accruedAmount (const Date &) const override |

| accrued amount at the given date More... | |

Visitability | |

| void | accept (AcyclicVisitor &) override |

| Public Member Functions inherited from FloatingRateCoupon | |

| FloatingRateCoupon (const Date &paymentDate, Real nominal, const Date &startDate, const Date &endDate, Natural fixingDays, const ext::shared_ptr< InterestRateIndex > &index, Real gearing=1.0, Spread spread=0.0, const Date &refPeriodStart=Date(), const Date &refPeriodEnd=Date(), DayCounter dayCounter=DayCounter(), bool isInArrears=false, const Date &exCouponDate=Date()) | |

| void | performCalculations () const override |

| Real | amount () const override |

| returns the amount of the cash flow More... | |

| Rate | rate () const override |

| accrued rate More... | |

| Real | price (const Handle< YieldTermStructure > &discountingCurve) const |

| DayCounter | dayCounter () const override |

| day counter for accrual calculation More... | |

| const ext::shared_ptr< InterestRateIndex > & | index () const |

| floating index More... | |

| Natural | fixingDays () const |

| fixing days More... | |

| Real | gearing () const |

| index gearing, i.e. multiplicative coefficient for the index More... | |

| Spread | spread () const |

| spread paid over the fixing of the underlying index More... | |

| virtual Rate | indexFixing () const |

| fixing of the underlying index More... | |

| virtual Rate | convexityAdjustment () const |

| convexity adjustment More... | |

| virtual Rate | adjustedFixing () const |

| convexity-adjusted fixing More... | |

| bool | isInArrears () const |

| whether or not the coupon fixes in arrears More... | |

| virtual void | setPricer (const ext::shared_ptr< FloatingRateCouponPricer > &) |

| ext::shared_ptr< FloatingRateCouponPricer > | pricer () const |

| Public Member Functions inherited from Coupon | |

| Coupon (const Date &paymentDate, Real nominal, const Date &accrualStartDate, const Date &accrualEndDate, const Date &refPeriodStart=Date(), const Date &refPeriodEnd=Date(), const Date &exCouponDate=Date()) | |

| Date | date () const override |

| Date | exCouponDate () const override |

| returns the date that the cash flow trades exCoupon More... | |

| virtual Real | nominal () const |

| const Date & | accrualStartDate () const |

| start of the accrual period More... | |

| const Date & | accrualEndDate () const |

| end of the accrual period More... | |

| const Date & | referencePeriodStart () const |

| start date of the reference period More... | |

| const Date & | referencePeriodEnd () const |

| end date of the reference period More... | |

| Time | accrualPeriod () const |

| accrual period as fraction of year More... | |

| Date::serial_type | accrualDays () const |

| accrual period in days More... | |

| Time | accruedPeriod (const Date &) const |

| accrued period as fraction of year at the given date More... | |

| Date::serial_type | accruedDays (const Date &) const |

| accrued days at the given date More... | |

| Public Member Functions inherited from CashFlow | |

| ~CashFlow () override=default | |

| bool | hasOccurred (const Date &refDate=Date(), ext::optional< bool > includeRefDate=ext::nullopt) const override |

| returns true if an event has already occurred before a date More... | |

| bool | tradingExCoupon (const Date &refDate=Date()) const |

| returns true if the cashflow is trading ex-coupon on the refDate More... | |

| Public Member Functions inherited from Event | |

| ~Event () override=default | |

| Public Member Functions inherited from Observable | |

| Observable ()=default | |

| Observable (const Observable &) | |

| Observable & | operator= (const Observable &) |

| Observable (Observable &&)=delete | |

| Observable & | operator= (Observable &&)=delete |

| virtual | ~Observable ()=default |

| void | notifyObservers () |

| Public Member Functions inherited from LazyObject | |

| LazyObject () | |

| ~LazyObject () override=default | |

| void | update () override |

| bool | isCalculated () const |

| void | forwardFirstNotificationOnly () |

| void | alwaysForwardNotifications () |

| void | recalculate () |

| void | freeze () |

| void | unfreeze () |

| Public Member Functions inherited from Observer | |

| Observer ()=default | |

| Observer (const Observer &) | |

| Observer & | operator= (const Observer &) |

| virtual | ~Observer () |

| std::pair< iterator, bool > | registerWith (const ext::shared_ptr< Observable > &) |

| void | registerWithObservables (const ext::shared_ptr< Observer > &) |

| Size | unregisterWith (const ext::shared_ptr< Observable > &) |

| void | unregisterWithAll () |

| virtual void | update ()=0 |

| virtual void | deepUpdate () |

Telescopic property | |

Telescopic formula cannot be used with lookback days being different than intrinsic index fixing delay. Only when index fixing delay is 0 and observation shift is used, we can apply telescopic formula, when applying lookback period. | |

| std::vector< Date > | valueDates_ |

| std::vector< Date > | interestDates_ |

| std::vector< Date > | fixingDates_ |

| std::vector< Rate > | fixings_ |

| Size | n_ |

| std::vector< Time > | dt_ |

| RateAveraging::Type | averagingMethod_ |

| Natural | lockoutDays_ |

| bool | applyObservationShift_ |

| bool | canApplyTelescopicFormula () const |

| Rate | averageRate (const Date &date) const |

Additional Inherited Members | |

| Public Types inherited from Observer | |

| typedef set_type::iterator | iterator |

| Protected Member Functions inherited from FloatingRateCoupon | |

| Rate | convexityAdjustmentImpl (Rate fixing) const |

| convexity adjustment for the given index fixing More... | |

| Protected Member Functions inherited from LazyObject | |

| virtual void | calculate () const |

| Protected Attributes inherited from FloatingRateCoupon | |

| ext::shared_ptr< InterestRateIndex > | index_ |

| DayCounter | dayCounter_ |

| Natural | fixingDays_ |

| Real | gearing_ |

| Spread | spread_ |

| bool | isInArrears_ |

| ext::shared_ptr< FloatingRateCouponPricer > | pricer_ |

| Real | rate_ |

| Protected Attributes inherited from Coupon | |

| Date | paymentDate_ |

| Real | nominal_ |

| Date | accrualStartDate_ |

| Date | accrualEndDate_ |

| Date | refPeriodStart_ |

| Date | refPeriodEnd_ |

| Date | exCouponDate_ |

| Real | accrualPeriod_ |

| Protected Attributes inherited from LazyObject | |

| bool | calculated_ = false |

| bool | frozen_ = false |

| bool | alwaysForward_ |

Detailed Description

overnight coupon

Coupon paying the interest, depending on the averaging convention, due to daily overnight fixings.

- Warning:

- telescopicValueDates optimizes the schedule for calculation speed, but might fail to produce correct results if the coupon ages by more than a grace period of 7 days. It is therefore recommended not to set this flag to true unless you know exactly what you are doing. The intended use is rather by the OISRateHelper which is safe, since it reinitialises the instrument each time the evaluation date changes.

Definition at line 50 of file overnightindexedcoupon.hpp.

Constructor & Destructor Documentation

◆ OvernightIndexedCoupon()

| OvernightIndexedCoupon | ( | const Date & | paymentDate, |

| Real | nominal, | ||

| const Date & | startDate, | ||

| const Date & | endDate, | ||

| const ext::shared_ptr< OvernightIndex > & | overnightIndex, | ||

| Real | gearing = 1.0, |

||

| Spread | spread = 0.0, |

||

| const Date & | refPeriodStart = Date(), |

||

| const Date & | refPeriodEnd = Date(), |

||

| const DayCounter & | dayCounter = DayCounter(), |

||

| bool | telescopicValueDates = false, |

||

| RateAveraging::Type | averagingMethod = RateAveraging::Compound, |

||

| Natural | lookbackDays = Null<Natural>(), |

||

| Natural | lockoutDays = 0, |

||

| bool | applyObservationShift = false |

||

| ) |

Member Function Documentation

◆ fixingDates()

| const std::vector< Date > & fixingDates | ( | ) | const |

fixing dates for the rates to be compounded

Definition at line 71 of file overnightindexedcoupon.hpp.

Here is the caller graph for this function:

◆ dt()

| const std::vector< Time > & dt | ( | ) | const |

accrual (compounding) periods

Definition at line 73 of file overnightindexedcoupon.hpp.

Here is the caller graph for this function:

◆ indexFixings()

| const vector< Rate > & indexFixings | ( | ) | const |

fixings to be compounded

Definition at line 209 of file overnightindexedcoupon.cpp.

◆ valueDates()

| const std::vector< Date > & valueDates | ( | ) | const |

value dates for the rates to be compounded

Definition at line 77 of file overnightindexedcoupon.hpp.

Here is the caller graph for this function:

◆ interestDates()

| const std::vector< Date > & interestDates | ( | ) | const |

interest dates for the rates to be compounded

Definition at line 79 of file overnightindexedcoupon.hpp.

Here is the caller graph for this function:

◆ averagingMethod()

| RateAveraging::Type averagingMethod | ( | ) | const |

averaging method

Definition at line 81 of file overnightindexedcoupon.hpp.

Here is the caller graph for this function:

◆ lockoutDays()

| Natural lockoutDays | ( | ) | const |

lockout days

Definition at line 83 of file overnightindexedcoupon.hpp.

Here is the caller graph for this function:

◆ applyObservationShift()

| bool applyObservationShift | ( | ) | const |

apply observation shift

Definition at line 85 of file overnightindexedcoupon.hpp.

Here is the caller graph for this function:

◆ fixingDate()

|

overridevirtual |

the date when the coupon is fully determined

Reimplemented from FloatingRateCoupon.

Definition at line 90 of file overnightindexedcoupon.hpp.

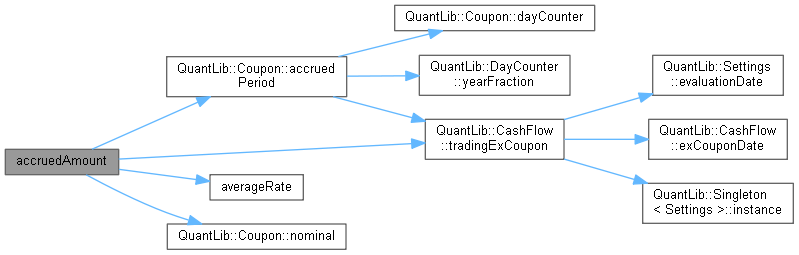

◆ accruedAmount()

accrued amount at the given date

Reimplemented from FloatingRateCoupon.

Definition at line 187 of file overnightindexedcoupon.cpp.

Here is the call graph for this function:

◆ accept()

|

overridevirtual |

Reimplemented from FloatingRateCoupon.

Definition at line 216 of file overnightindexedcoupon.cpp.

Here is the call graph for this function:

◆ canApplyTelescopicFormula()

| bool canApplyTelescopicFormula | ( | ) | const |

Definition at line 103 of file overnightindexedcoupon.hpp.

Here is the caller graph for this function:

◆ averageRate()

Definition at line 199 of file overnightindexedcoupon.cpp.

Here is the caller graph for this function:

Member Data Documentation

◆ valueDates_

|

private |

Definition at line 109 of file overnightindexedcoupon.hpp.

◆ interestDates_

|

private |

Definition at line 109 of file overnightindexedcoupon.hpp.

◆ fixingDates_

|

private |

Definition at line 109 of file overnightindexedcoupon.hpp.

◆ fixings_

|

mutableprivate |

Definition at line 110 of file overnightindexedcoupon.hpp.

◆ n_

|

private |

Definition at line 111 of file overnightindexedcoupon.hpp.

◆ dt_

|

private |

Definition at line 112 of file overnightindexedcoupon.hpp.

◆ averagingMethod_

|

private |

Definition at line 113 of file overnightindexedcoupon.hpp.

◆ lockoutDays_

|

private |

Definition at line 114 of file overnightindexedcoupon.hpp.

◆ applyObservationShift_

|

private |

Definition at line 115 of file overnightindexedcoupon.hpp.