Rate helper for bootstrapping over Overnight Indexed Swap rates. More...

#include <oisratehelper.hpp>

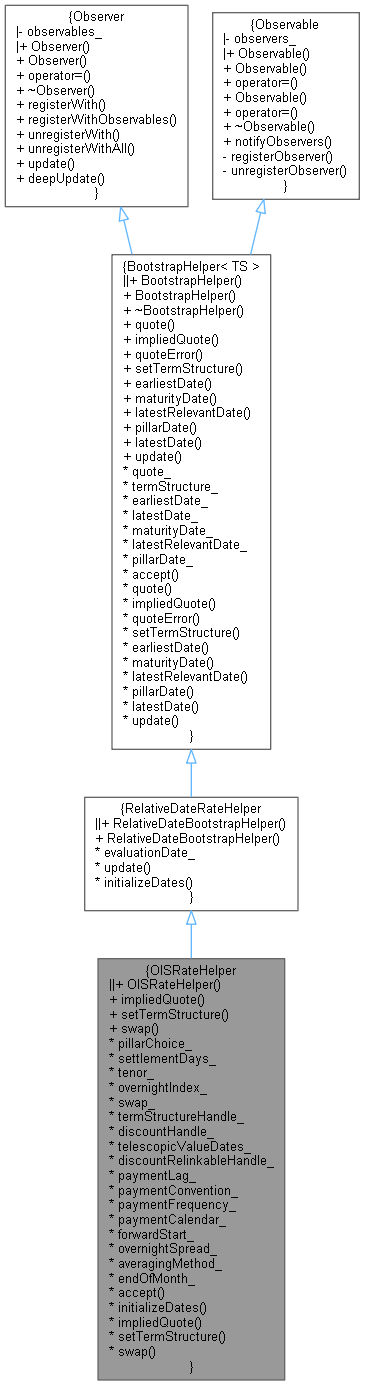

Inheritance diagram for OISRateHelper:

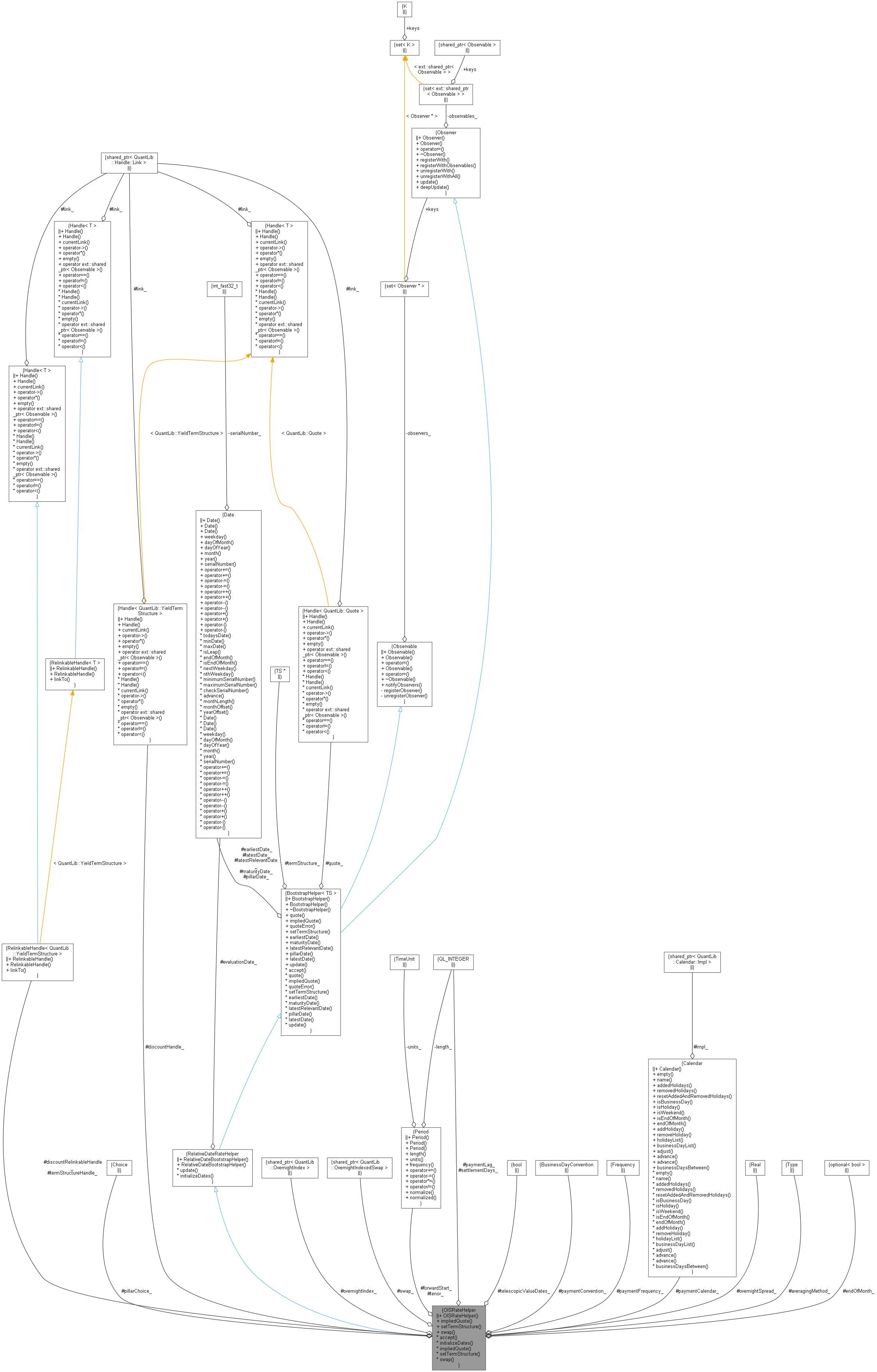

Inheritance diagram for OISRateHelper: Collaboration diagram for OISRateHelper:

Collaboration diagram for OISRateHelper:

Public Member Functions | |

| OISRateHelper (Natural settlementDays, const Period &tenor, const Handle< Quote > &fixedRate, const ext::shared_ptr< OvernightIndex > &overnightIndex, Handle< YieldTermStructure > discountingCurve={}, bool telescopicValueDates=false, Integer paymentLag=0, BusinessDayConvention paymentConvention=Following, Frequency paymentFrequency=Annual, Calendar paymentCalendar=Calendar(), const Period &forwardStart=0 *Days, const std::variant< Spread, Handle< Quote > > &overnightSpread=Spread(0.0), Pillar::Choice pillar=Pillar::LastRelevantDate, Date customPillarDate=Date(), RateAveraging::Type averagingMethod=RateAveraging::Compound, ext::optional< bool > endOfMonth=ext::nullopt, ext::optional< Frequency > fixedPaymentFrequency=ext::nullopt, Calendar fixedCalendar=Calendar(), Natural lookbackDays=Null< Natural >(), Natural lockoutDays=0, bool applyObservationShift=false, ext::shared_ptr< FloatingRateCouponPricer > pricer={}, DateGeneration::Rule rule=DateGeneration::Backward, Calendar overnightCalendar=Calendar()) | |

| OISRateHelper (const Date &startDate, const Date &endDate, const Handle< Quote > &fixedRate, const ext::shared_ptr< OvernightIndex > &overnightIndex, Handle< YieldTermStructure > discountingCurve={}, bool telescopicValueDates=false, Integer paymentLag=0, BusinessDayConvention paymentConvention=Following, Frequency paymentFrequency=Annual, Calendar paymentCalendar=Calendar(), const std::variant< Spread, Handle< Quote > > &overnightSpread=Spread(0.0), Pillar::Choice pillar=Pillar::LastRelevantDate, Date customPillarDate=Date(), RateAveraging::Type averagingMethod=RateAveraging::Compound, ext::optional< bool > endOfMonth=ext::nullopt, ext::optional< Frequency > fixedPaymentFrequency=ext::nullopt, Calendar fixedCalendar=Calendar(), Natural lookbackDays=Null< Natural >(), Natural lockoutDays=0, bool applyObservationShift=false, ext::shared_ptr< FloatingRateCouponPricer > pricer={}, DateGeneration::Rule rule=DateGeneration::Backward, Calendar overnightCalendar=Calendar()) | |

RateHelper interface | |

| Real | impliedQuote () const override |

| void | setTermStructure (YieldTermStructure *) override |

inspectors | |

| ext::shared_ptr< OvernightIndexedSwap > | swap () const |

| Public Member Functions inherited from RelativeDateBootstrapHelper< TS > | |

| RelativeDateBootstrapHelper (const std::variant< Spread, Handle< Quote > > "e, bool updateDates=true) | |

| void | update () override |

| Public Member Functions inherited from BootstrapHelper< TS > | |

| BootstrapHelper (const std::variant< Spread, Handle< Quote > > "e) | |

| ~BootstrapHelper () override=default | |

| const Handle< Quote > & | quote () const |

| Real | quoteError () const |

| virtual void | setTermStructure (TS *) |

| sets the term structure to be used for pricing More... | |

| virtual Date | earliestDate () const |

| earliest relevant date More... | |

| virtual Date | maturityDate () const |

| instrument's maturity date More... | |

| virtual Date | latestRelevantDate () const |

| latest relevant date More... | |

| virtual Date | pillarDate () const |

| pillar date More... | |

| virtual Date | latestDate () const |

| latest date More... | |

| Public Member Functions inherited from Observer | |

| Observer ()=default | |

| Observer (const Observer &) | |

| Observer & | operator= (const Observer &) |

| virtual | ~Observer () |

| std::pair< iterator, bool > | registerWith (const ext::shared_ptr< Observable > &) |

| void | registerWithObservables (const ext::shared_ptr< Observer > &) |

| Size | unregisterWith (const ext::shared_ptr< Observable > &) |

| void | unregisterWithAll () |

| virtual void | update ()=0 |

| virtual void | deepUpdate () |

| Public Member Functions inherited from Observable | |

| Observable ()=default | |

| Observable (const Observable &) | |

| Observable & | operator= (const Observable &) |

| Observable (Observable &&)=delete | |

| Observable & | operator= (Observable &&)=delete |

| virtual | ~Observable ()=default |

| void | notifyObservers () |

Additional Inherited Members | |

| Public Types inherited from Observer | |

| typedef set_type::iterator | iterator |

| Protected Member Functions inherited from RelativeDateBootstrapHelper< TS > | |

| Protected Attributes inherited from RelativeDateBootstrapHelper< TS > | |

| Date | evaluationDate_ |

| bool | updateDates_ |

| Protected Attributes inherited from BootstrapHelper< TS > | |

| Handle< Quote > | quote_ |

| TS * | termStructure_ |

| Date | earliestDate_ |

| Date | latestDate_ |

| Date | maturityDate_ |

| Date | latestRelevantDate_ |

| Date | pillarDate_ |

Detailed Description

Rate helper for bootstrapping over Overnight Indexed Swap rates.

Definition at line 38 of file oisratehelper.hpp.

Constructor & Destructor Documentation

◆ OISRateHelper() [1/2]

| OISRateHelper | ( | Natural | settlementDays, |

| const Period & | tenor, | ||

| const Handle< Quote > & | fixedRate, | ||

| const ext::shared_ptr< OvernightIndex > & | overnightIndex, | ||

| Handle< YieldTermStructure > | discountingCurve = {}, |

||

| bool | telescopicValueDates = false, |

||

| Integer | paymentLag = 0, |

||

| BusinessDayConvention | paymentConvention = Following, |

||

| Frequency | paymentFrequency = Annual, |

||

| Calendar | paymentCalendar = Calendar(), |

||

| const Period & | forwardStart = 0 * Days, |

||

| const std::variant< Spread, Handle< Quote > > & | overnightSpread = Spread(0.0), |

||

| Pillar::Choice | pillar = Pillar::LastRelevantDate, |

||

| Date | customPillarDate = Date(), |

||

| RateAveraging::Type | averagingMethod = RateAveraging::Compound, |

||

| ext::optional< bool > | endOfMonth = ext::nullopt, |

||

| ext::optional< Frequency > | fixedPaymentFrequency = ext::nullopt, |

||

| Calendar | fixedCalendar = Calendar(), |

||

| Natural | lookbackDays = Null<Natural>(), |

||

| Natural | lockoutDays = 0, |

||

| bool | applyObservationShift = false, |

||

| ext::shared_ptr< FloatingRateCouponPricer > | pricer = {}, |

||

| DateGeneration::Rule | rule = DateGeneration::Backward, |

||

| Calendar | overnightCalendar = Calendar() |

||

| ) |

◆ OISRateHelper() [2/2]

| OISRateHelper | ( | const Date & | startDate, |

| const Date & | endDate, | ||

| const Handle< Quote > & | fixedRate, | ||

| const ext::shared_ptr< OvernightIndex > & | overnightIndex, | ||

| Handle< YieldTermStructure > | discountingCurve = {}, |

||

| bool | telescopicValueDates = false, |

||

| Integer | paymentLag = 0, |

||

| BusinessDayConvention | paymentConvention = Following, |

||

| Frequency | paymentFrequency = Annual, |

||

| Calendar | paymentCalendar = Calendar(), |

||

| const std::variant< Spread, Handle< Quote > > & | overnightSpread = Spread(0.0), |

||

| Pillar::Choice | pillar = Pillar::LastRelevantDate, |

||

| Date | customPillarDate = Date(), |

||

| RateAveraging::Type | averagingMethod = RateAveraging::Compound, |

||

| ext::optional< bool > | endOfMonth = ext::nullopt, |

||

| ext::optional< Frequency > | fixedPaymentFrequency = ext::nullopt, |

||

| Calendar | fixedCalendar = Calendar(), |

||

| Natural | lookbackDays = Null<Natural>(), |

||

| Natural | lockoutDays = 0, |

||

| bool | applyObservationShift = false, |

||

| ext::shared_ptr< FloatingRateCouponPricer > | pricer = {}, |

||

| DateGeneration::Rule | rule = DateGeneration::Backward, |

||

| Calendar | overnightCalendar = Calendar() |

||

| ) |

Member Function Documentation

◆ impliedQuote()

|

overridevirtual |

Implements BootstrapHelper< TS >.

Definition at line 205 of file oisratehelper.cpp.

◆ setTermStructure()

|

override |

◆ swap()

| ext::shared_ptr< OvernightIndexedSwap > swap | ( | ) | const |

Definition at line 99 of file oisratehelper.hpp.

◆ accept()

|

overridevirtual |

Reimplemented from BootstrapHelper< TS >.

Definition at line 219 of file oisratehelper.cpp.

Here is the call graph for this function:

◆ initialize()

|

protected |

Definition at line 102 of file oisratehelper.cpp.

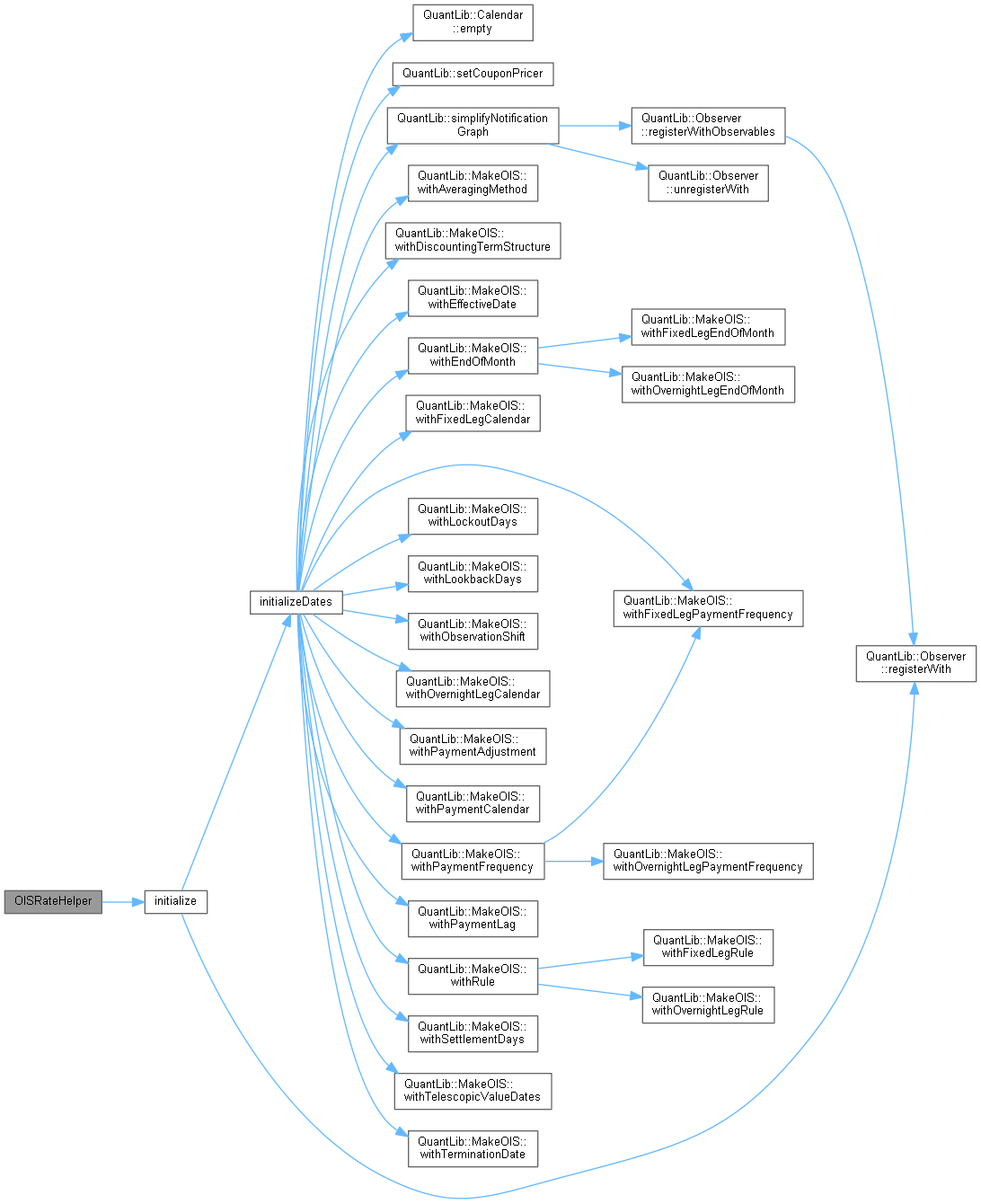

Here is the call graph for this function: Here is the caller graph for this function:

Here is the caller graph for this function:

◆ initializeDates()

|

overrideprotectedvirtual |

Implements RelativeDateBootstrapHelper< TS >.

Definition at line 119 of file oisratehelper.cpp.

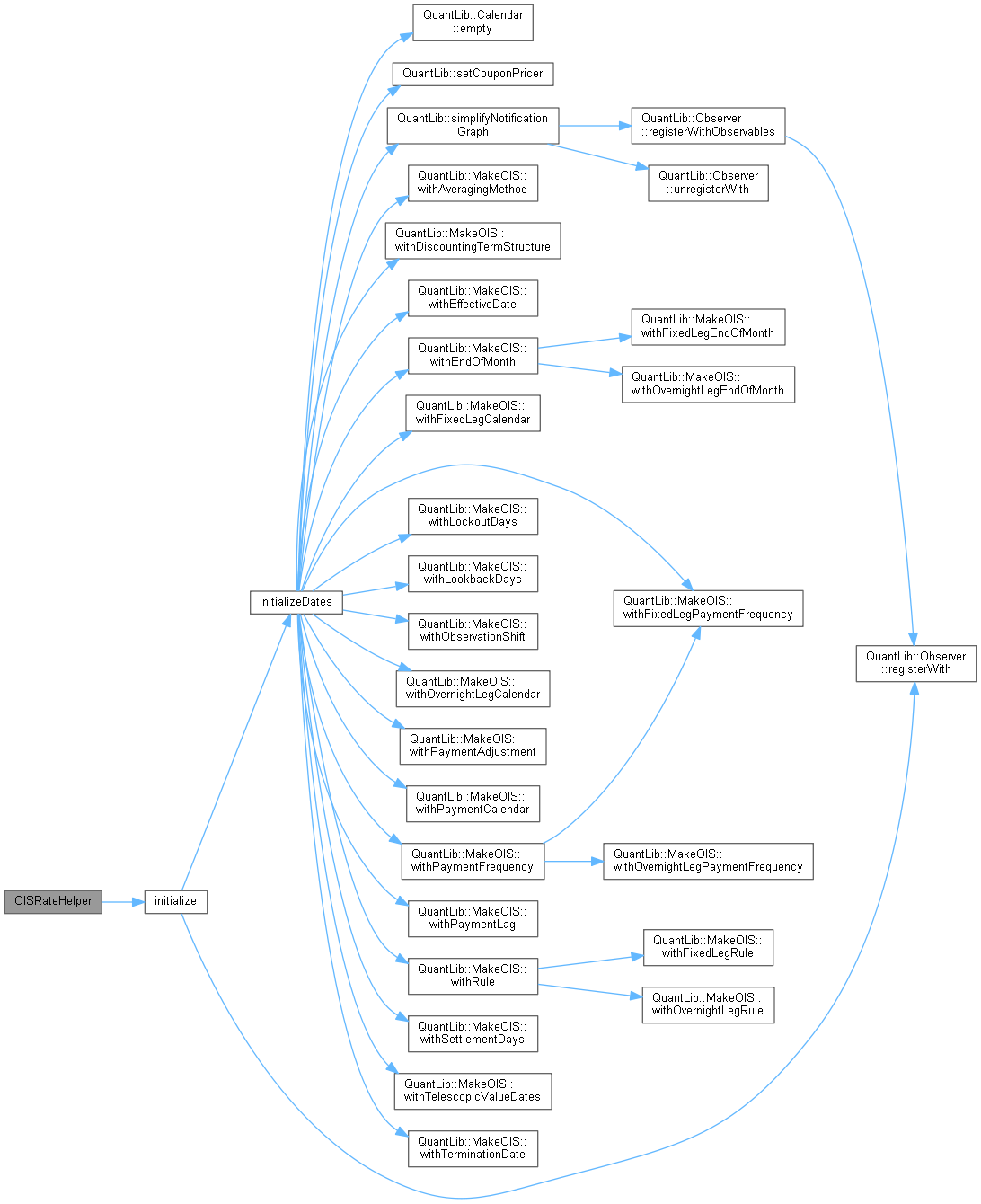

Here is the call graph for this function: Here is the caller graph for this function:

Here is the caller graph for this function:

Member Data Documentation

◆ settlementDays_

|

protected |

Definition at line 110 of file oisratehelper.hpp.

◆ tenor_

|

protected |

Definition at line 111 of file oisratehelper.hpp.

◆ startDate_

|

protected |

Definition at line 112 of file oisratehelper.hpp.

◆ endDate_

|

protected |

Definition at line 112 of file oisratehelper.hpp.

◆ overnightIndex_

|

protected |

Definition at line 113 of file oisratehelper.hpp.

◆ swap_

|

protected |

Definition at line 115 of file oisratehelper.hpp.

◆ termStructureHandle_

|

protected |

Definition at line 116 of file oisratehelper.hpp.

◆ discountHandle_

|

protected |

Definition at line 118 of file oisratehelper.hpp.

◆ telescopicValueDates_

|

protected |

Definition at line 119 of file oisratehelper.hpp.

◆ discountRelinkableHandle_

|

protected |

Definition at line 120 of file oisratehelper.hpp.

◆ paymentLag_

|

protected |

Definition at line 122 of file oisratehelper.hpp.

◆ paymentConvention_

|

protected |

Definition at line 123 of file oisratehelper.hpp.

◆ paymentFrequency_

|

protected |

Definition at line 124 of file oisratehelper.hpp.

◆ paymentCalendar_

|

protected |

Definition at line 125 of file oisratehelper.hpp.

◆ forwardStart_

|

protected |

Definition at line 126 of file oisratehelper.hpp.

◆ overnightSpread_

Definition at line 127 of file oisratehelper.hpp.

◆ pillarChoice_

|

protected |

Definition at line 128 of file oisratehelper.hpp.

◆ averagingMethod_

|

protected |

Definition at line 129 of file oisratehelper.hpp.

◆ endOfMonth_

|

protected |

Definition at line 130 of file oisratehelper.hpp.

◆ fixedPaymentFrequency_

|

protected |

Definition at line 131 of file oisratehelper.hpp.

◆ fixedCalendar_

|

protected |

Definition at line 132 of file oisratehelper.hpp.

◆ overnightCalendar_

|

protected |

Definition at line 133 of file oisratehelper.hpp.

◆ lookbackDays_

|

protected |

Definition at line 134 of file oisratehelper.hpp.

◆ lockoutDays_

|

protected |

Definition at line 135 of file oisratehelper.hpp.

◆ applyObservationShift_

|

protected |

Definition at line 136 of file oisratehelper.hpp.

◆ pricer_

|

protected |

Definition at line 137 of file oisratehelper.hpp.

◆ rule_

|

protected |

Definition at line 138 of file oisratehelper.hpp.