Base class for cash flows. More...

#include <cashflow.hpp>

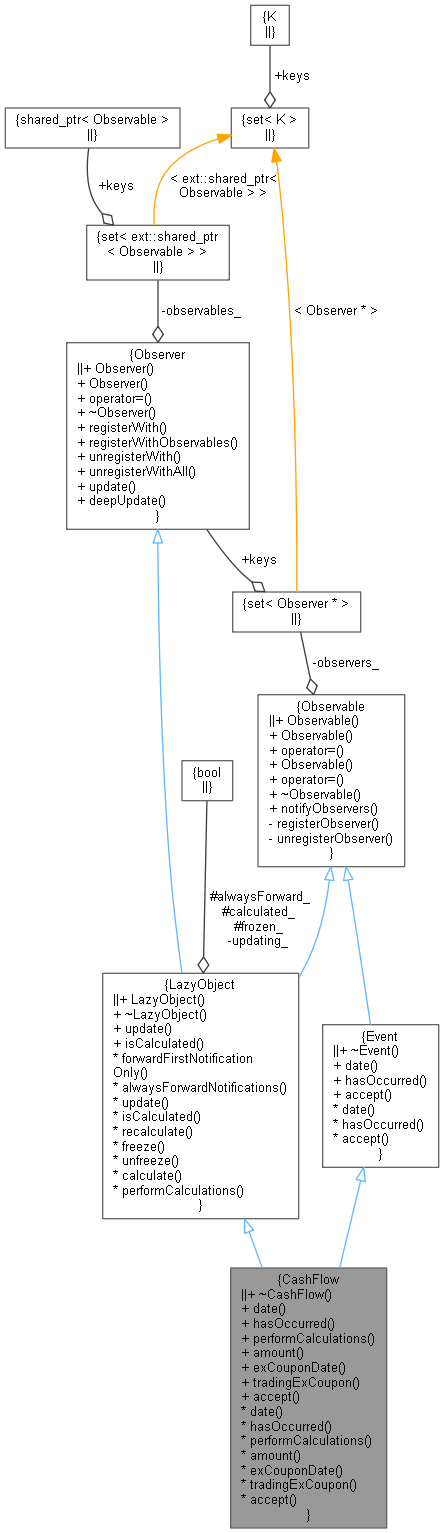

Inheritance diagram for CashFlow:

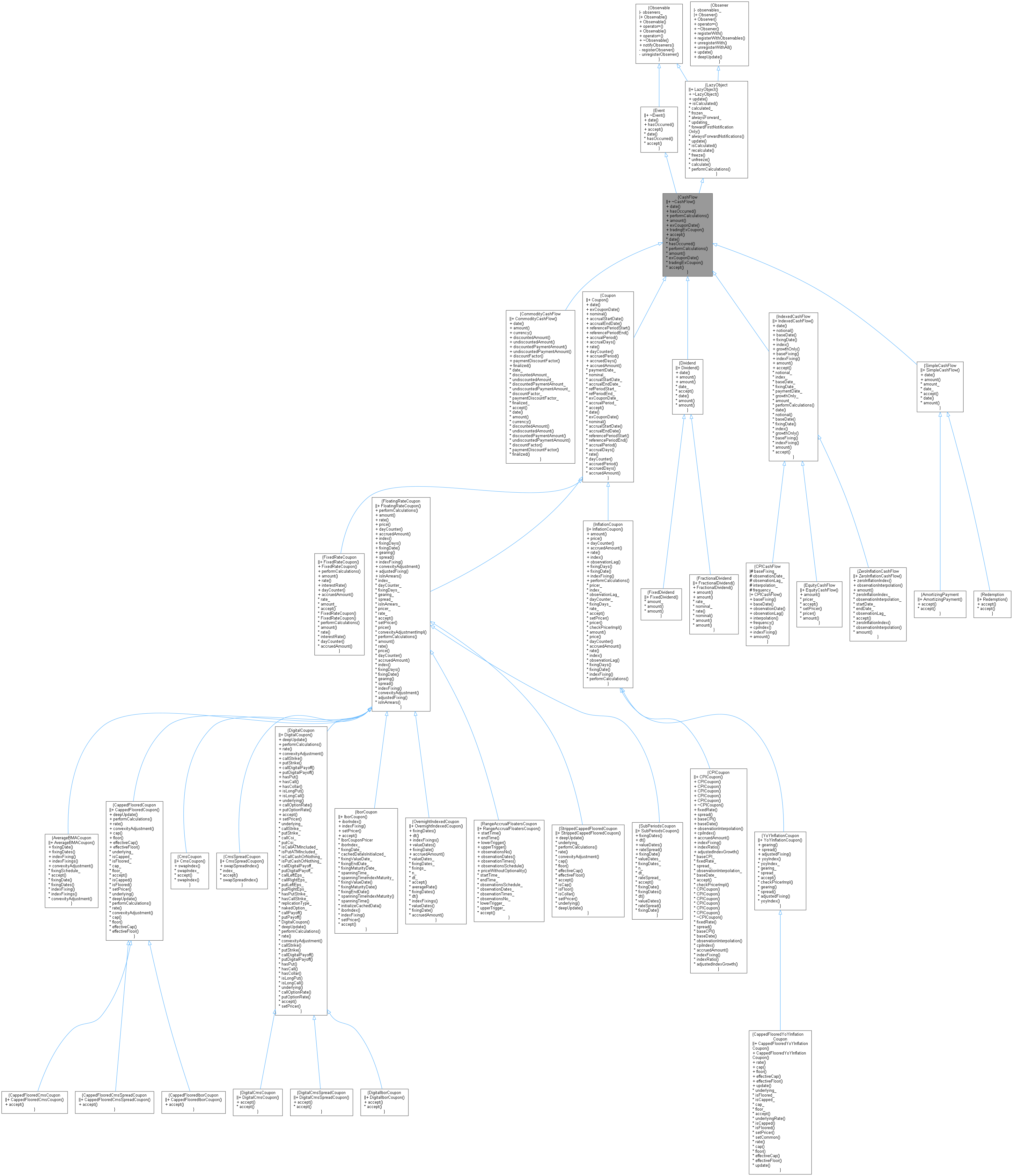

Inheritance diagram for CashFlow: Collaboration diagram for CashFlow:

Collaboration diagram for CashFlow:

Public Member Functions | |

| ~CashFlow () override=default | |

Event interface | |

| Date | date () const override=0 |

| bool | hasOccurred (const Date &refDate=Date(), ext::optional< bool > includeRefDate=ext::nullopt) const override |

| returns true if an event has already occurred before a date More... | |

LazyObject interface | |

| void | performCalculations () const override |

CashFlow interface | |

| virtual Real | amount () const =0 |

| returns the amount of the cash flow More... | |

| virtual Date | exCouponDate () const |

| returns the date that the cash flow trades exCoupon More... | |

| bool | tradingExCoupon (const Date &refDate=Date()) const |

| returns true if the cashflow is trading ex-coupon on the refDate More... | |

Visitability | |

| void | accept (AcyclicVisitor &) override |

| Public Member Functions inherited from Event | |

| ~Event () override=default | |

| Public Member Functions inherited from Observable | |

| Observable ()=default | |

| Observable (const Observable &) | |

| Observable & | operator= (const Observable &) |

| Observable (Observable &&)=delete | |

| Observable & | operator= (Observable &&)=delete |

| virtual | ~Observable ()=default |

| void | notifyObservers () |

| Public Member Functions inherited from LazyObject | |

| LazyObject () | |

| ~LazyObject () override=default | |

| void | update () override |

| bool | isCalculated () const |

| void | forwardFirstNotificationOnly () |

| void | alwaysForwardNotifications () |

| void | recalculate () |

| void | freeze () |

| void | unfreeze () |

| Public Member Functions inherited from Observer | |

| Observer ()=default | |

| Observer (const Observer &) | |

| Observer & | operator= (const Observer &) |

| virtual | ~Observer () |

| std::pair< iterator, bool > | registerWith (const ext::shared_ptr< Observable > &) |

| void | registerWithObservables (const ext::shared_ptr< Observer > &) |

| Size | unregisterWith (const ext::shared_ptr< Observable > &) |

| void | unregisterWithAll () |

| virtual void | update ()=0 |

| virtual void | deepUpdate () |

Additional Inherited Members | |

| Public Types inherited from Observer | |

| typedef set_type::iterator | iterator |

| Protected Member Functions inherited from LazyObject | |

| virtual void | calculate () const |

| Protected Attributes inherited from LazyObject | |

| bool | calculated_ = false |

| bool | frozen_ = false |

| bool | alwaysForward_ |

Detailed Description

Base class for cash flows.

This class is purely virtual and acts as a base class for the actual cash flow implementations.

Definition at line 40 of file cashflow.hpp.

Constructor & Destructor Documentation

◆ ~CashFlow()

|

overridedefault |

Member Function Documentation

◆ date()

|

overridepure virtual |

- Note

- This is inherited from the event class

Implements Event.

Implemented in Coupon, Dividend, IndexedCashFlow, SimpleCashFlow, and CommodityCashFlow.

Here is the caller graph for this function:

◆ hasOccurred()

|

overridevirtual |

returns true if an event has already occurred before a date

overloads Event::hasOccurred in order to take Settings::includeTodaysCashflows in account

Reimplemented from Event.

Definition at line 27 of file cashflow.cpp.

Here is the call graph for this function: Here is the caller graph for this function:

Here is the caller graph for this function:

◆ performCalculations()

|

overridevirtual |

This method must implement any calculations which must be (re)done in order to calculate the desired results.

Implements LazyObject.

Reimplemented in CappedFlooredCoupon, DigitalCoupon, FixedRateCoupon, FloatingRateCoupon, IndexedCashFlow, InflationCoupon, and StrippedCappedFlooredCoupon.

Definition at line 56 of file cashflow.hpp.

◆ amount()

|

pure virtual |

returns the amount of the cash flow

- Note

- The amount is not discounted, i.e., it is the actual amount paid at the cash flow date.

Implemented in FixedDividend, FractionalDividend, EquityCashFlow, FixedRateCoupon, FloatingRateCoupon, IndexedCashFlow, InflationCoupon, SimpleCashFlow, CommodityCashFlow, and Dividend.

Here is the caller graph for this function:

◆ exCouponDate()

|

virtual |

returns the date that the cash flow trades exCoupon

Reimplemented in Coupon.

Definition at line 66 of file cashflow.hpp.

Here is the caller graph for this function:

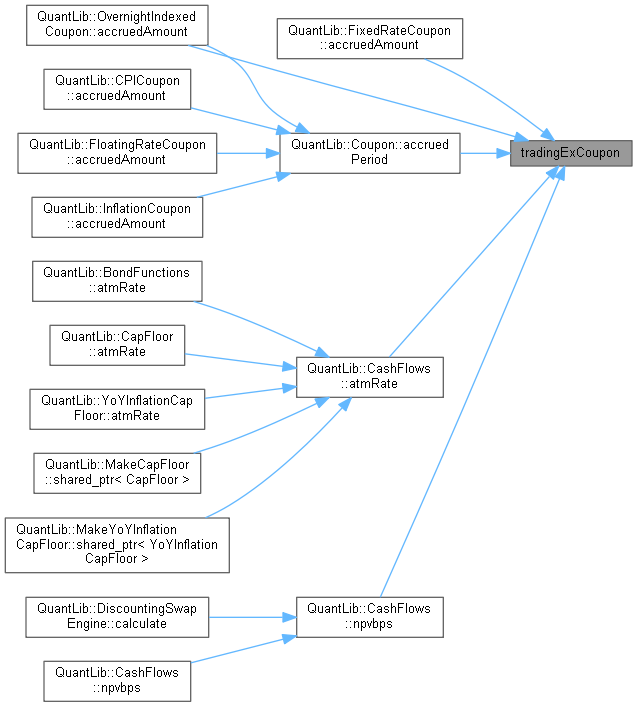

◆ tradingExCoupon()

returns true if the cashflow is trading ex-coupon on the refDate

Definition at line 51 of file cashflow.cpp.

Here is the call graph for this function: Here is the caller graph for this function:

Here is the caller graph for this function:

◆ accept()

|

overridevirtual |

Reimplemented from Event.

Reimplemented in AverageBMACoupon, CappedFlooredCoupon, CmsCoupon, Coupon, CPICoupon, DigitalCmsCoupon, DigitalCoupon, DigitalIborCoupon, Dividend, EquityCashFlow, FixedRateCoupon, FloatingRateCoupon, IborCoupon, IndexedCashFlow, InflationCoupon, MultipleResetsCoupon, OvernightIndexedCoupon, RangeAccrualFloatersCoupon, SimpleCashFlow, Redemption, AmortizingPayment, YoYInflationCoupon, ZeroInflationCashFlow, CommodityCashFlow, CmsSpreadCoupon, DigitalCmsSpreadCoupon, StrippedCappedFlooredCoupon, CappedFlooredIborCoupon, CappedFlooredCmsCoupon, CappedFlooredYoYInflationCoupon, and CappedFlooredCmsSpreadCoupon.

Definition at line 63 of file cashflow.cpp.

Here is the call graph for this function: Here is the caller graph for this function:

Here is the caller graph for this function: