Discount curve fitted to a set of fixed-coupon bonds. More...

#include <fittedbonddiscountcurve.hpp>

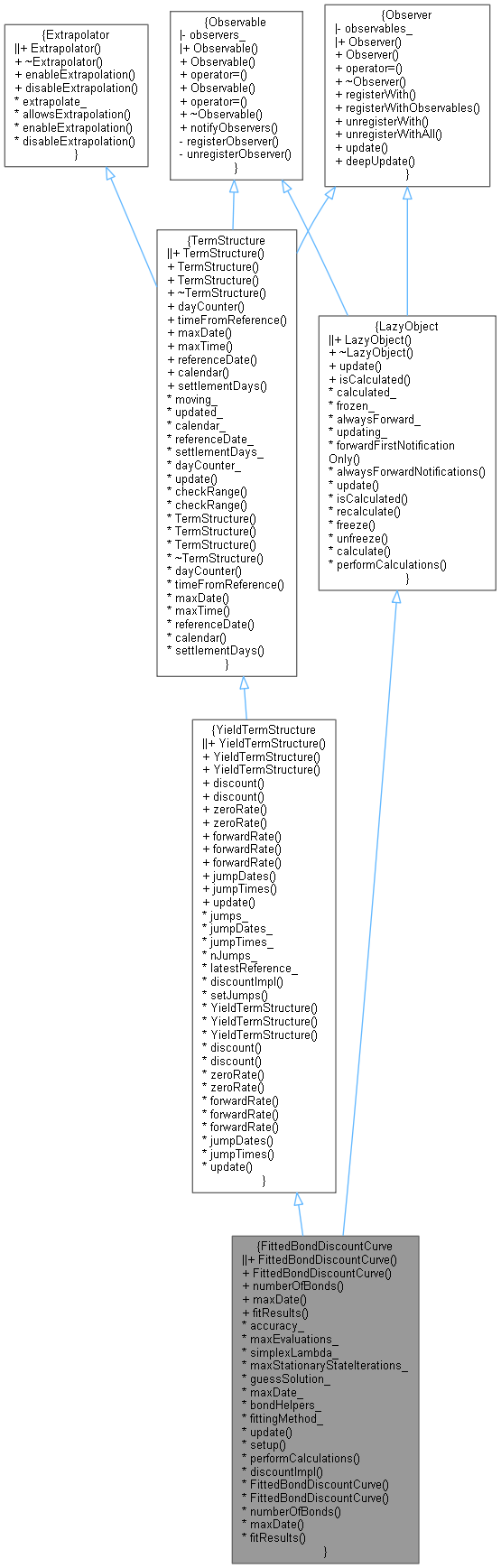

Inheritance diagram for FittedBondDiscountCurve:

Inheritance diagram for FittedBondDiscountCurve: Collaboration diagram for FittedBondDiscountCurve:

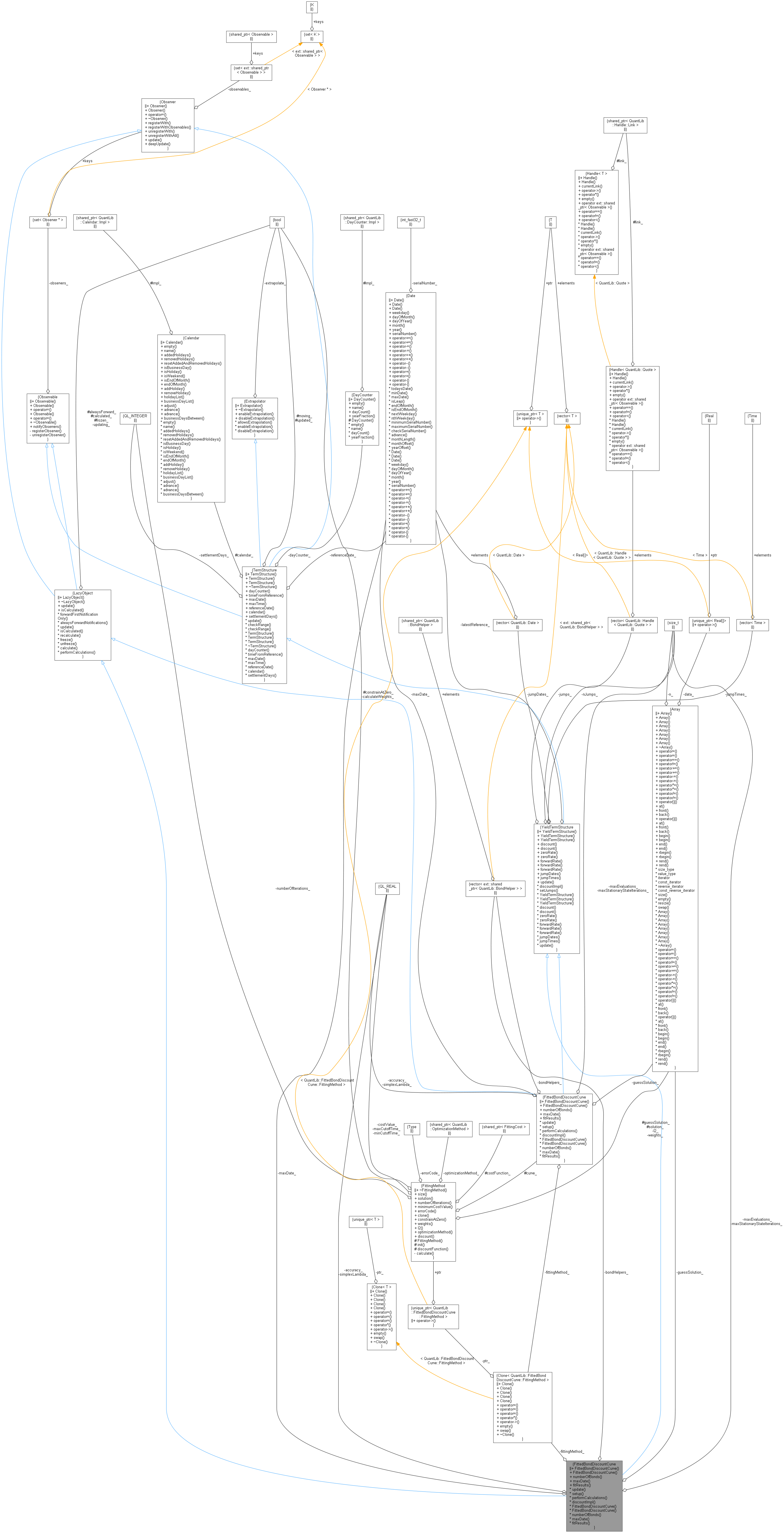

Collaboration diagram for FittedBondDiscountCurve:

Classes | |

| class | FittingMethod |

| Base fitting method used to construct a fitted bond discount curve. More... | |

Public Member Functions | |

Constructors | |

| FittedBondDiscountCurve (Natural settlementDays, const Calendar &calendar, std::vector< ext::shared_ptr< BondHelper > > bonds, const DayCounter &dayCounter, const FittingMethod &fittingMethod, Real accuracy=1.0e-10, Size maxEvaluations=10000, Array guess=Array(), Real simplexLambda=1.0, Size maxStationaryStateIterations=100) | |

| reference date based on current evaluation date More... | |

| FittedBondDiscountCurve (const Date &referenceDate, std::vector< ext::shared_ptr< BondHelper > > bonds, const DayCounter &dayCounter, const FittingMethod &fittingMethod, Real accuracy=1.0e-10, Size maxEvaluations=10000, Array guess=Array(), Real simplexLambda=1.0, Size maxStationaryStateIterations=100) | |

| curve reference date fixed for life of curve More... | |

| FittedBondDiscountCurve (Natural settlementDays, const Calendar &calendar, const FittingMethod &fittingMethod, Array parameters, Date maxDate, const DayCounter &dayCounter) | |

| don't fit, use precalculated parameters More... | |

| FittedBondDiscountCurve (const Date &referenceDate, const FittingMethod &fittingMethod, Array parameters, Date maxDate, const DayCounter &dayCounter) | |

| don't fit, use precalculated parameters More... | |

Inspectors | |

| Size | numberOfBonds () const |

| total number of bonds used to fit the yield curve More... | |

| Date | maxDate () const override |

| the latest date for which the curve can return values More... | |

| const FittingMethod & | fitResults () const |

| class holding the results of the fit More... | |

Other utilities | |

| void | resetGuess (const Array &guess) |

| Public Member Functions inherited from YieldTermStructure | |

| YieldTermStructure (const DayCounter &dc=DayCounter()) | |

| YieldTermStructure (const Date &referenceDate, const Calendar &cal=Calendar(), const DayCounter &dc=DayCounter(), std::vector< Handle< Quote > > jumps={}, const std::vector< Date > &jumpDates={}) | |

| YieldTermStructure (Natural settlementDays, const Calendar &cal, const DayCounter &dc=DayCounter(), std::vector< Handle< Quote > > jumps={}, const std::vector< Date > &jumpDates={}) | |

| DiscountFactor | discount (const Date &d, bool extrapolate=false) const |

| DiscountFactor | discount (Time t, bool extrapolate=false) const |

| InterestRate | zeroRate (const Date &d, const DayCounter &resultDayCounter, Compounding comp, Frequency freq=Annual, bool extrapolate=false) const |

| InterestRate | zeroRate (Time t, Compounding comp, Frequency freq=Annual, bool extrapolate=false) const |

| InterestRate | forwardRate (const Date &d1, const Date &d2, const DayCounter &resultDayCounter, Compounding comp, Frequency freq=Annual, bool extrapolate=false) const |

| InterestRate | forwardRate (const Date &d, const Period &p, const DayCounter &resultDayCounter, Compounding comp, Frequency freq=Annual, bool extrapolate=false) const |

| InterestRate | forwardRate (Time t1, Time t2, Compounding comp, Frequency freq=Annual, bool extrapolate=false) const |

| const std::vector< Date > & | jumpDates () const |

| const std::vector< Time > & | jumpTimes () const |

| void | update () override |

| Public Member Functions inherited from TermStructure | |

| TermStructure (DayCounter dc=DayCounter()) | |

| default constructor More... | |

| TermStructure (const Date &referenceDate, Calendar calendar=Calendar(), DayCounter dc=DayCounter()) | |

| initialize with a fixed reference date More... | |

| TermStructure (Natural settlementDays, Calendar, DayCounter dc=DayCounter()) | |

| calculate the reference date based on the global evaluation date More... | |

| ~TermStructure () override=default | |

| virtual DayCounter | dayCounter () const |

| the day counter used for date/time conversion More... | |

| Time | timeFromReference (const Date &date) const |

| date/time conversion More... | |

| virtual Time | maxTime () const |

| the latest time for which the curve can return values More... | |

| virtual const Date & | referenceDate () const |

| the date at which discount = 1.0 and/or variance = 0.0 More... | |

| virtual Calendar | calendar () const |

| the calendar used for reference and/or option date calculation More... | |

| virtual Natural | settlementDays () const |

| the settlementDays used for reference date calculation More... | |

| Public Member Functions inherited from Observer | |

| Observer ()=default | |

| Observer (const Observer &) | |

| Observer & | operator= (const Observer &) |

| virtual | ~Observer () |

| std::pair< iterator, bool > | registerWith (const ext::shared_ptr< Observable > &) |

| void | registerWithObservables (const ext::shared_ptr< Observer > &) |

| Size | unregisterWith (const ext::shared_ptr< Observable > &) |

| void | unregisterWithAll () |

| virtual void | update ()=0 |

| virtual void | deepUpdate () |

| Public Member Functions inherited from Observable | |

| Observable ()=default | |

| Observable (const Observable &) | |

| Observable & | operator= (const Observable &) |

| Observable (Observable &&)=delete | |

| Observable & | operator= (Observable &&)=delete |

| virtual | ~Observable ()=default |

| void | notifyObservers () |

| Public Member Functions inherited from Extrapolator | |

| Extrapolator ()=default | |

| virtual | ~Extrapolator ()=default |

| void | enableExtrapolation (bool b=true) |

| enable extrapolation in subsequent calls More... | |

| void | disableExtrapolation (bool b=true) |

| disable extrapolation in subsequent calls More... | |

| bool | allowsExtrapolation () const |

| tells whether extrapolation is enabled More... | |

| Public Member Functions inherited from LazyObject | |

| LazyObject () | |

| ~LazyObject () override=default | |

| bool | isCalculated () const |

| void | forwardFirstNotificationOnly () |

| void | alwaysForwardNotifications () |

| void | recalculate () |

| void | freeze () |

| void | unfreeze () |

Observer interface | |

| Real | accuracy_ |

| Size | maxEvaluations_ |

| Real | simplexLambda_ |

| Size | maxStationaryStateIterations_ |

| Array | guessSolution_ |

| Date | maxDate_ |

| std::vector< ext::shared_ptr< BondHelper > > | bondHelpers_ |

| Clone< FittingMethod > | fittingMethod_ |

| void | update () override |

| void | setup () |

| void | performCalculations () const override |

| DiscountFactor | discountImpl (Time) const override |

| discount factor calculation More... | |

Additional Inherited Members | |

| Public Types inherited from Observer | |

| typedef set_type::iterator | iterator |

| Protected Member Functions inherited from YieldTermStructure | |

| Protected Member Functions inherited from TermStructure | |

| void | checkRange (const Date &d, bool extrapolate) const |

| date-range check More... | |

| void | checkRange (Time t, bool extrapolate) const |

| time-range check More... | |

| Protected Member Functions inherited from LazyObject | |

| virtual void | calculate () const |

| Protected Attributes inherited from TermStructure | |

| bool | moving_ = false |

| bool | updated_ = true |

| Calendar | calendar_ |

| Protected Attributes inherited from LazyObject | |

| bool | calculated_ = false |

| bool | frozen_ = false |

| bool | alwaysForward_ |

Detailed Description

Discount curve fitted to a set of fixed-coupon bonds.

This class fits a discount function \( d(t) \) over a set of bonds, using a user defined fitting method. The discount function is fit in such a way so that all cashflows of all input bonds, when discounted using \( d(t) \), will reproduce the set of input bond prices in an optimized sense. Minimized price errors are weighted by the inverse of their respective bond duration.

The FittedBondDiscountCurve class acts as a generic wrapper, while its inner class FittingMethod provides the implementation details. Developers thus need only derive new fitting methods from the latter.

- Warning:

- The method can be slow if there are many bonds to fit. Speed also depends on the particular choice of fitting method chosen and its convergence properties under optimization. See also todo list for BondDiscountCurveFittingMethod.

Definition at line 81 of file fittedbonddiscountcurve.hpp.

Constructor & Destructor Documentation

◆ FittedBondDiscountCurve() [1/4]

| FittedBondDiscountCurve | ( | Natural | settlementDays, |

| const Calendar & | calendar, | ||

| std::vector< ext::shared_ptr< BondHelper > > | bonds, | ||

| const DayCounter & | dayCounter, | ||

| const FittingMethod & | fittingMethod, | ||

| Real | accuracy = 1.0e-10, |

||

| Size | maxEvaluations = 10000, |

||

| Array | guess = Array(), |

||

| Real | simplexLambda = 1.0, |

||

| Size | maxStationaryStateIterations = 100 |

||

| ) |

reference date based on current evaluation date

Definition at line 49 of file fittedbonddiscountcurve.cpp.

Here is the call graph for this function:

◆ FittedBondDiscountCurve() [2/4]

| FittedBondDiscountCurve | ( | const Date & | referenceDate, |

| std::vector< ext::shared_ptr< BondHelper > > | bonds, | ||

| const DayCounter & | dayCounter, | ||

| const FittingMethod & | fittingMethod, | ||

| Real | accuracy = 1.0e-10, |

||

| Size | maxEvaluations = 10000, |

||

| Array | guess = Array(), |

||

| Real | simplexLambda = 1.0, |

||

| Size | maxStationaryStateIterations = 100 |

||

| ) |

curve reference date fixed for life of curve

Definition at line 69 of file fittedbonddiscountcurve.cpp.

Here is the call graph for this function:

◆ FittedBondDiscountCurve() [3/4]

| FittedBondDiscountCurve | ( | Natural | settlementDays, |

| const Calendar & | calendar, | ||

| const FittingMethod & | fittingMethod, | ||

| Array | parameters, | ||

| Date | maxDate, | ||

| const DayCounter & | dayCounter | ||

| ) |

don't fit, use precalculated parameters

Definition at line 88 of file fittedbonddiscountcurve.cpp.

Here is the call graph for this function:

◆ FittedBondDiscountCurve() [4/4]

| FittedBondDiscountCurve | ( | const Date & | referenceDate, |

| const FittingMethod & | fittingMethod, | ||

| Array | parameters, | ||

| Date | maxDate, | ||

| const DayCounter & | dayCounter | ||

| ) |

don't fit, use precalculated parameters

Definition at line 103 of file fittedbonddiscountcurve.cpp.

Here is the call graph for this function:

Member Function Documentation

◆ numberOfBonds()

| Size numberOfBonds | ( | ) | const |

total number of bonds used to fit the yield curve

Definition at line 288 of file fittedbonddiscountcurve.hpp.

◆ maxDate()

|

overridevirtual |

the latest date for which the curve can return values

Implements TermStructure.

Definition at line 292 of file fittedbonddiscountcurve.hpp.

Here is the call graph for this function:

◆ fitResults()

| const FittedBondDiscountCurve::FittingMethod & fitResults | ( | ) | const |

class holding the results of the fit

Definition at line 298 of file fittedbonddiscountcurve.hpp.

Here is the call graph for this function:

◆ resetGuess()

| void resetGuess | ( | const Array & | guess | ) |

This allows to try out multiple guesses and avoid local minima

Definition at line 118 of file fittedbonddiscountcurve.cpp.

Here is the call graph for this function:

◆ update()

|

overridevirtual |

This method must be implemented in derived classes. An instance of Observer does not call this method directly: instead, it will be called by the observables the instance registered with when they need to notify any changes.

Reimplemented from LazyObject.

Definition at line 303 of file fittedbonddiscountcurve.hpp.

Here is the call graph for this function: Here is the caller graph for this function:

Here is the caller graph for this function:

◆ setup()

|

private |

Definition at line 308 of file fittedbonddiscountcurve.hpp.

Here is the call graph for this function: Here is the caller graph for this function:

Here is the caller graph for this function:

◆ performCalculations()

|

overrideprivatevirtual |

This method must implement any calculations which must be (re)done in order to calculate the desired results.

Implements LazyObject.

Definition at line 125 of file fittedbonddiscountcurve.cpp.

Here is the call graph for this function:

◆ discountImpl()

|

overrideprivatevirtual |

discount factor calculation

Implements YieldTermStructure.

Definition at line 313 of file fittedbonddiscountcurve.hpp.

Here is the call graph for this function:

Member Data Documentation

◆ accuracy_

|

private |

Definition at line 153 of file fittedbonddiscountcurve.hpp.

◆ maxEvaluations_

|

private |

Definition at line 155 of file fittedbonddiscountcurve.hpp.

◆ simplexLambda_

|

private |

Definition at line 157 of file fittedbonddiscountcurve.hpp.

◆ maxStationaryStateIterations_

|

private |

Definition at line 159 of file fittedbonddiscountcurve.hpp.

◆ guessSolution_

|

private |

Definition at line 161 of file fittedbonddiscountcurve.hpp.

◆ maxDate_

|

mutableprivate |

Definition at line 162 of file fittedbonddiscountcurve.hpp.

◆ bondHelpers_

|

private |

Definition at line 163 of file fittedbonddiscountcurve.hpp.

◆ fittingMethod_

|

private |

Definition at line 164 of file fittedbonddiscountcurve.hpp.