|

| | BlackStyleSwaptionEngine (Handle< YieldTermStructure > discountCurve, Volatility vol, const DayCounter &dc=Actual365Fixed(), Real displacement=0.0, CashAnnuityModel model=DiscountCurve) |

| |

| | BlackStyleSwaptionEngine (Handle< YieldTermStructure > discountCurve, const Handle< Quote > &vol, const DayCounter &dc=Actual365Fixed(), Real displacement=0.0, CashAnnuityModel model=DiscountCurve) |

| |

| | BlackStyleSwaptionEngine (Handle< YieldTermStructure > discountCurve, Handle< SwaptionVolatilityStructure > vol, CashAnnuityModel model=DiscountCurve) |

| |

| void | calculate () const override |

| |

| Handle< YieldTermStructure > | termStructure () |

| |

| Handle< SwaptionVolatilityStructure > | volatility () |

| |

| PricingEngine::arguments * | getArguments () const override |

| |

| const PricingEngine::results * | getResults () const override |

| |

| void | reset () override |

| |

| void | update () override |

| |

| | ~PricingEngine () override=default |

| |

| virtual arguments * | getArguments () const =0 |

| |

| virtual const results * | getResults () const =0 |

| |

| virtual void | reset ()=0 |

| |

| virtual void | calculate () const =0 |

| |

| | Observable ()=default |

| |

| | Observable (const Observable &) |

| |

| Observable & | operator= (const Observable &) |

| |

| | Observable (Observable &&)=delete |

| |

| Observable & | operator= (Observable &&)=delete |

| |

| virtual | ~Observable ()=default |

| |

| void | notifyObservers () |

| |

| | Observer ()=default |

| |

| | Observer (const Observer &) |

| |

| Observer & | operator= (const Observer &) |

| |

| virtual | ~Observer () |

| |

| std::pair< iterator, bool > | registerWith (const ext::shared_ptr< Observable > &) |

| |

| void | registerWithObservables (const ext::shared_ptr< Observer > &) |

| |

| Size | unregisterWith (const ext::shared_ptr< Observable > &) |

| |

| void | unregisterWithAll () |

| |

| virtual void | update ()=0 |

| |

| virtual void | deepUpdate () |

| |

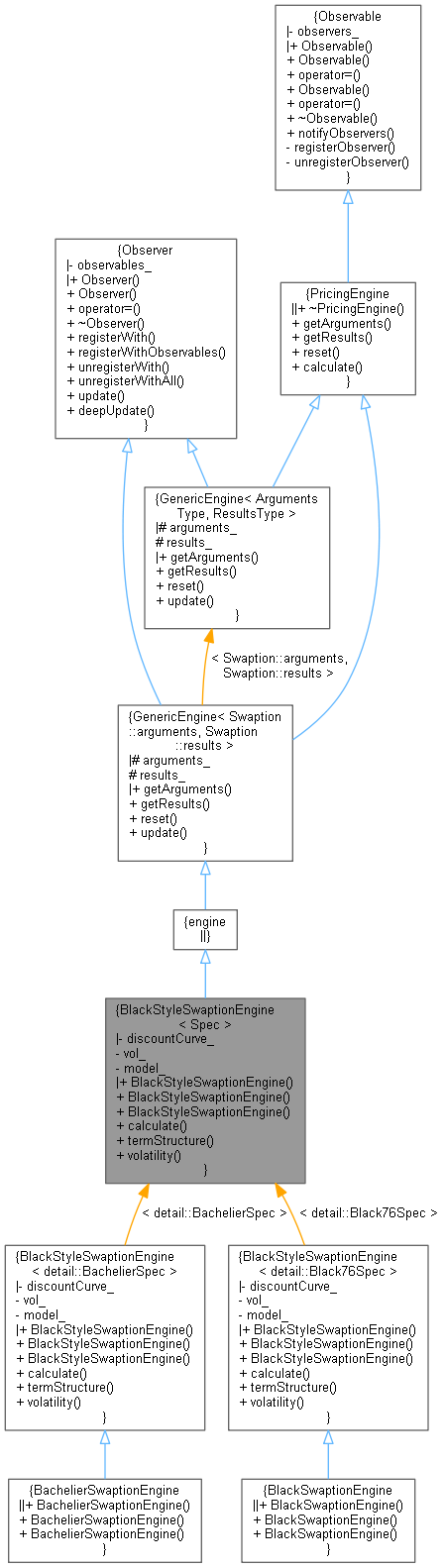

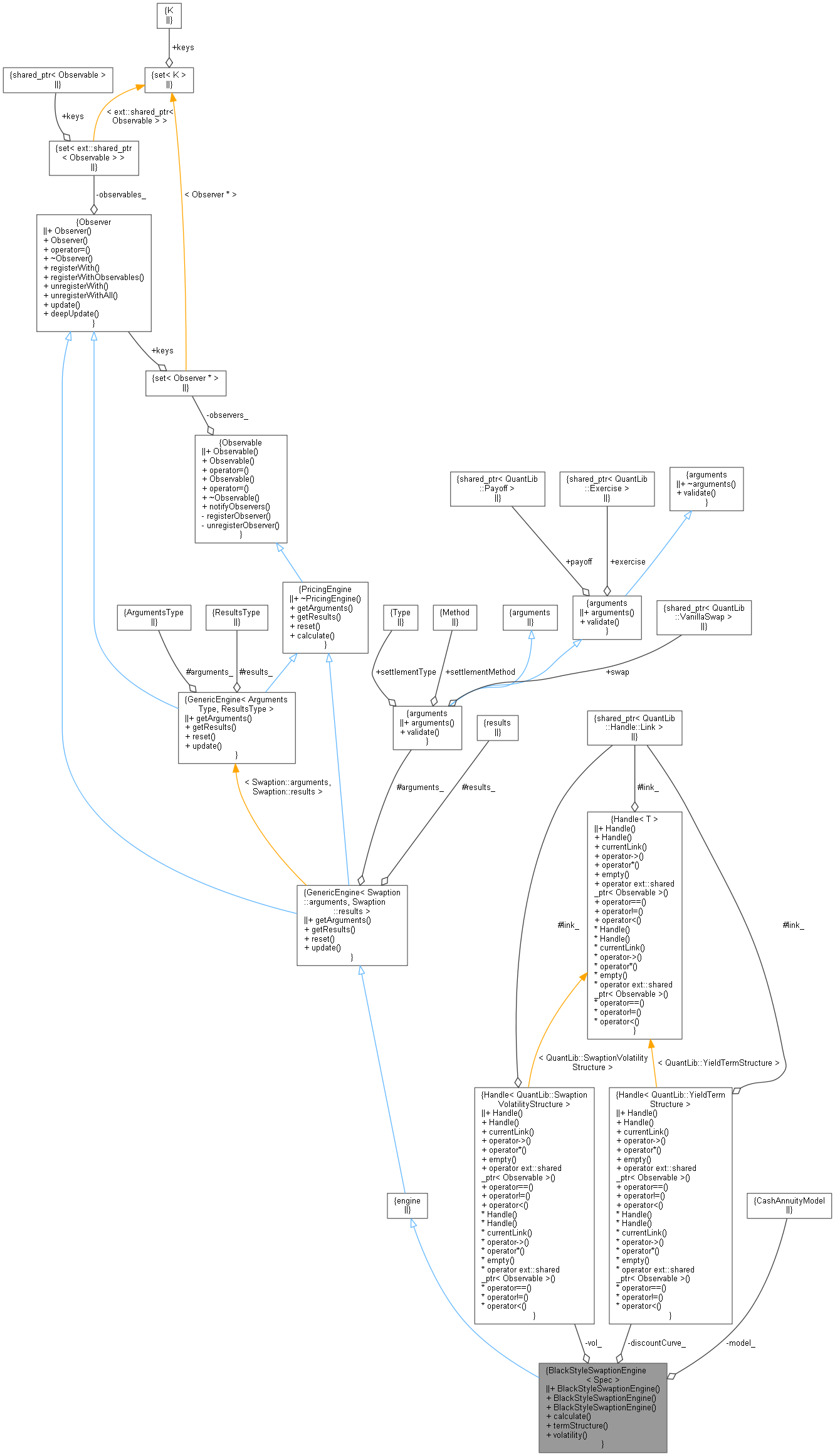

template<class Spec>

class QuantLib::detail::BlackStyleSwaptionEngine< Spec >

Generic Black-style-formula swaption engine This is the base class for the Black and Bachelier swaption engines

Definition at line 54 of file blackswaptionengine.hpp.

Inheritance diagram for BlackStyleSwaptionEngine< Spec >:

Inheritance diagram for BlackStyleSwaptionEngine< Spec >: