One-factor Student t - Gaussian Copula. More...

#include <onefactorstudentcopula.hpp>

Inheritance diagram for OneFactorStudentGaussianCopula:

Inheritance diagram for OneFactorStudentGaussianCopula: Collaboration diagram for OneFactorStudentGaussianCopula:

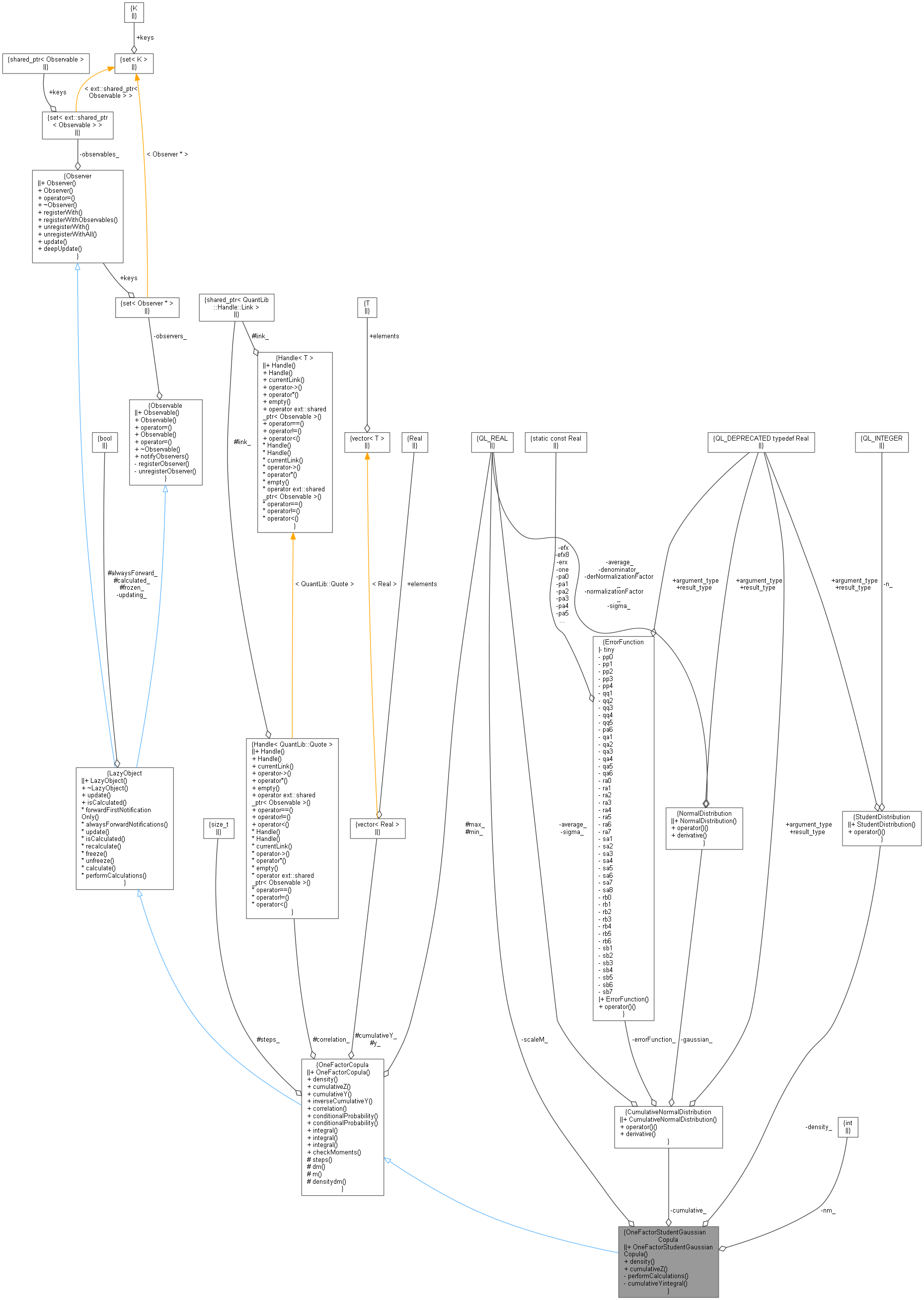

Collaboration diagram for OneFactorStudentGaussianCopula:

Public Member Functions | |

| OneFactorStudentGaussianCopula (const Handle< Quote > &correlation, int nm, Real maximum=10, Size integrationSteps=200) | |

| Real | density (Real m) const override |

| Density function of M. More... | |

| Real | cumulativeZ (Real z) const override |

| Cumulative distribution of Z. More... | |

| Public Member Functions inherited from OneFactorCopula | |

| OneFactorCopula (Handle< Quote > correlation, Real maximum=5.0, Size integrationSteps=50, Real minimum=-5.0) | |

| virtual Real | density (Real m) const =0 |

| Density function of M. More... | |

| virtual Real | cumulativeZ (Real z) const =0 |

| Cumulative distribution of Z. More... | |

| virtual Real | cumulativeY (Real y) const |

| Cumulative distribution of Y. More... | |

| virtual Real | inverseCumulativeY (Real p) const |

| Inverse cumulative distribution of Y. More... | |

| Real | correlation () const |

| Single correlation parameter. More... | |

| Real | conditionalProbability (Real prob, Real m) const |

| Conditional probability. More... | |

| std::vector< Real > | conditionalProbability (const std::vector< Real > &prob, Real m) const |

| Vector of conditional probabilities. More... | |

| Real | integral (Real p) const |

| template<class F > | |

| Real | integral (const F &f, std::vector< Real > &probabilities) const |

| template<class F > | |

| Distribution | integral (const F &f, const std::vector< Real > &nominals, const std::vector< Real > &probabilities) const |

| int | checkMoments (Real tolerance) const |

| Public Member Functions inherited from LazyObject | |

| LazyObject () | |

| ~LazyObject () override=default | |

| void | update () override |

| bool | isCalculated () const |

| void | forwardFirstNotificationOnly () |

| void | alwaysForwardNotifications () |

| void | recalculate () |

| void | freeze () |

| void | unfreeze () |

| Public Member Functions inherited from Observable | |

| Observable ()=default | |

| Observable (const Observable &) | |

| Observable & | operator= (const Observable &) |

| Observable (Observable &&)=delete | |

| Observable & | operator= (Observable &&)=delete |

| virtual | ~Observable ()=default |

| void | notifyObservers () |

| Public Member Functions inherited from Observer | |

| Observer ()=default | |

| Observer (const Observer &) | |

| Observer & | operator= (const Observer &) |

| virtual | ~Observer () |

| std::pair< iterator, bool > | registerWith (const ext::shared_ptr< Observable > &) |

| void | registerWithObservables (const ext::shared_ptr< Observer > &) |

| Size | unregisterWith (const ext::shared_ptr< Observable > &) |

| void | unregisterWithAll () |

| virtual void | update ()=0 |

| virtual void | deepUpdate () |

Private Member Functions | |

| void | performCalculations () const override |

| Observer interface. More... | |

| Real | cumulativeYintegral (Real y) const |

Private Attributes | |

| StudentDistribution | density_ |

| CumulativeNormalDistribution | cumulative_ |

| int | nm_ |

| Real | scaleM_ |

Additional Inherited Members | |

| Public Types inherited from Observer | |

| typedef set_type::iterator | iterator |

| Protected Member Functions inherited from OneFactorCopula | |

| Size | steps () const |

| Real | dm (Size i) const |

| Real | m (Size i) const |

| Real | densitydm (Size i) const |

| Protected Member Functions inherited from LazyObject | |

| virtual void | calculate () const |

| Protected Attributes inherited from OneFactorCopula | |

| Handle< Quote > | correlation_ |

| Real | max_ |

| Size | steps_ |

| Real | min_ |

| std::vector< Real > | y_ |

| std::vector< Real > | cumulativeY_ |

| Protected Attributes inherited from LazyObject | |

| bool | calculated_ = false |

| bool | frozen_ = false |

| bool | alwaysForward_ |

Detailed Description

One-factor Student t - Gaussian Copula.

The copula model

\[ Y_i = a_i\,M+\sqrt{1-a_i^2}\:Z_i \]

is specified here by setting the probability density functions for \( Z_i \) ( \( D_Z \)) to a Gaussian and for \( M \) ( \( D_M \)) to a Student t-distribution with \( N_m \) degrees of freedom.

The variance of the Student t-distribution with \( \nu \) degrees of freedom is \( \nu / (\nu - 2) \). Since the copula approach requires zero mean and unit variance distributions, \( M \) is scaled by \( \sqrt{(N_m - 2) / N_m}. \)

Definition at line 161 of file onefactorstudentcopula.hpp.

Constructor & Destructor Documentation

◆ OneFactorStudentGaussianCopula()

| OneFactorStudentGaussianCopula | ( | const Handle< Quote > & | correlation, |

| int | nm, | ||

| Real | maximum = 10, |

||

| Size | integrationSteps = 200 |

||

| ) |

Definition at line 191 of file onefactorstudentcopula.cpp.

Here is the call graph for this function:

Member Function Documentation

◆ density()

Density function of M.

Derived classes must override this method and ensure zero mean and unit variance.

Implements OneFactorCopula.

Definition at line 187 of file onefactorstudentcopula.hpp.

Here is the call graph for this function:

◆ cumulativeZ()

Cumulative distribution of Z.

Derived classes must override this method and ensure zero mean and unit variance.

Implements OneFactorCopula.

Definition at line 191 of file onefactorstudentcopula.hpp.

◆ performCalculations()

|

overrideprivatevirtual |

Observer interface.

Implements LazyObject.

Definition at line 207 of file onefactorstudentcopula.cpp.

Here is the call graph for this function:

◆ cumulativeYintegral()

Definition at line 227 of file onefactorstudentcopula.cpp.

Here is the call graph for this function: Here is the caller graph for this function:

Here is the caller graph for this function:

Member Data Documentation

◆ density_

|

private |

Definition at line 175 of file onefactorstudentcopula.hpp.

◆ cumulative_

|

private |

Definition at line 176 of file onefactorstudentcopula.hpp.

◆ nm_

|

private |

Definition at line 177 of file onefactorstudentcopula.hpp.

◆ scaleM_

|

private |

Definition at line 179 of file onefactorstudentcopula.hpp.