#include <distribution.hpp>

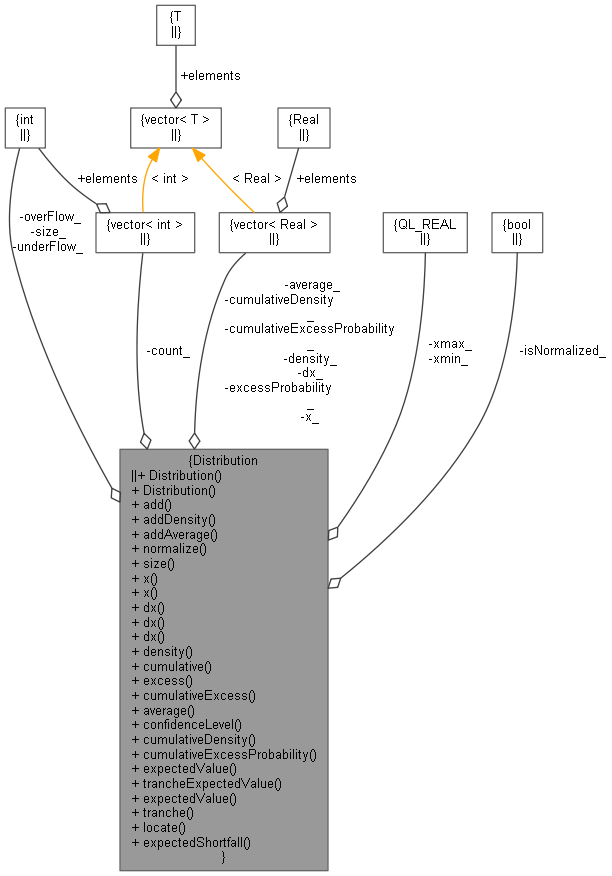

Collaboration diagram for Distribution:

Collaboration diagram for Distribution:

Public Member Functions | |

| Distribution (int nBuckets, Real xmin, Real xmax) | |

| Distribution ()=default | |

| void | add (Real value) |

| void | addDensity (int bucket, Real value) |

| void | addAverage (int bucket, Real value) |

| void | normalize () |

| Size | size () const |

| Real | x (Size k) |

| std::vector< Real > & | x () |

| Real | dx (Size k) |

| std::vector< Real > & | dx () |

| Real | dx (Real x) |

| Real | density (Size k) |

| Real | cumulative (Size k) |

| Real | excess (Size k) |

| Real | cumulativeExcess (Size k) |

| Real | average (Size k) |

| Real | confidenceLevel (Real quantil) |

| Real | cumulativeDensity (Real x) |

| Real | cumulativeExcessProbability (Real a, Real b) |

| Real | expectedValue () |

| Real | trancheExpectedValue (Real a, Real d) |

| template<class F > | |

| Real | expectedValue (F &f) |

| void | tranche (Real attachmentPoint, Real detachmentPoint) |

| int | locate (Real x) |

| Real | expectedShortfall (Real percValue) |

Private Attributes | |

| int | size_ |

| Real | xmin_ |

| Real | xmax_ |

| std::vector< int > | count_ |

| std::vector< Real > | x_ |

| std::vector< Real > | dx_ |

| std::vector< Real > | density_ |

| std::vector< Real > | cumulativeDensity_ |

| std::vector< Real > | excessProbability_ |

| std::vector< Real > | cumulativeExcessProbability_ |

| std::vector< Real > | average_ |

| int | overFlow_ |

| int | underFlow_ |

| bool | isNormalized_ |

Friends | |

| class | ManipulateDistribution |

Detailed Description

Definition at line 37 of file distribution.hpp.

Constructor & Destructor Documentation

◆ Distribution() [1/2]

| Distribution | ( | int | nBuckets, |

| Real | xmin, | ||

| Real | xmax | ||

| ) |

Definition at line 33 of file distribution.cpp.

◆ Distribution() [2/2]

|

default |

Member Function Documentation

◆ add()

| void add | ( | Real | value | ) |

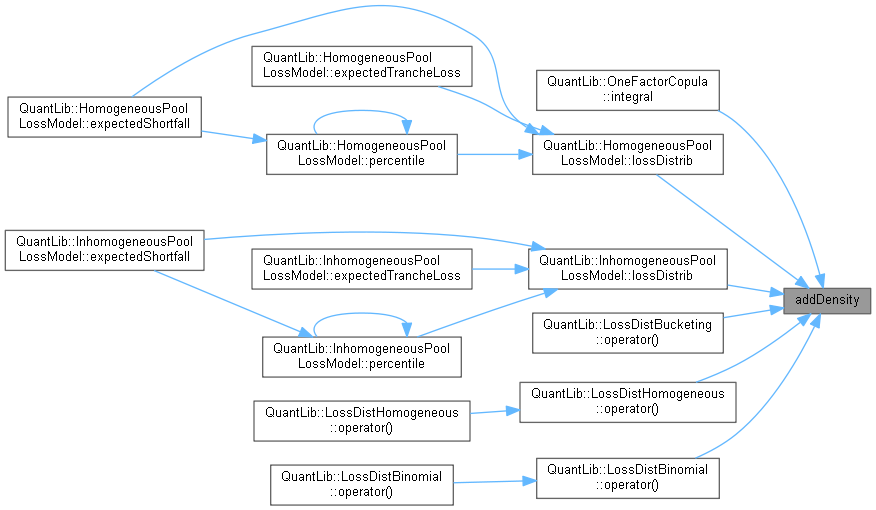

◆ addDensity()

| void addDensity | ( | int | bucket, |

| Real | value | ||

| ) |

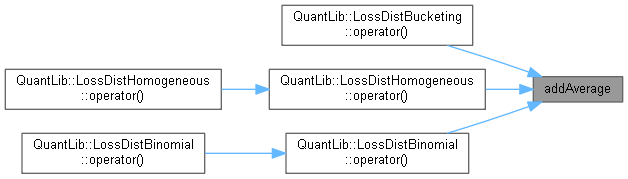

◆ addAverage()

| void addAverage | ( | int | bucket, |

| Real | value | ||

| ) |

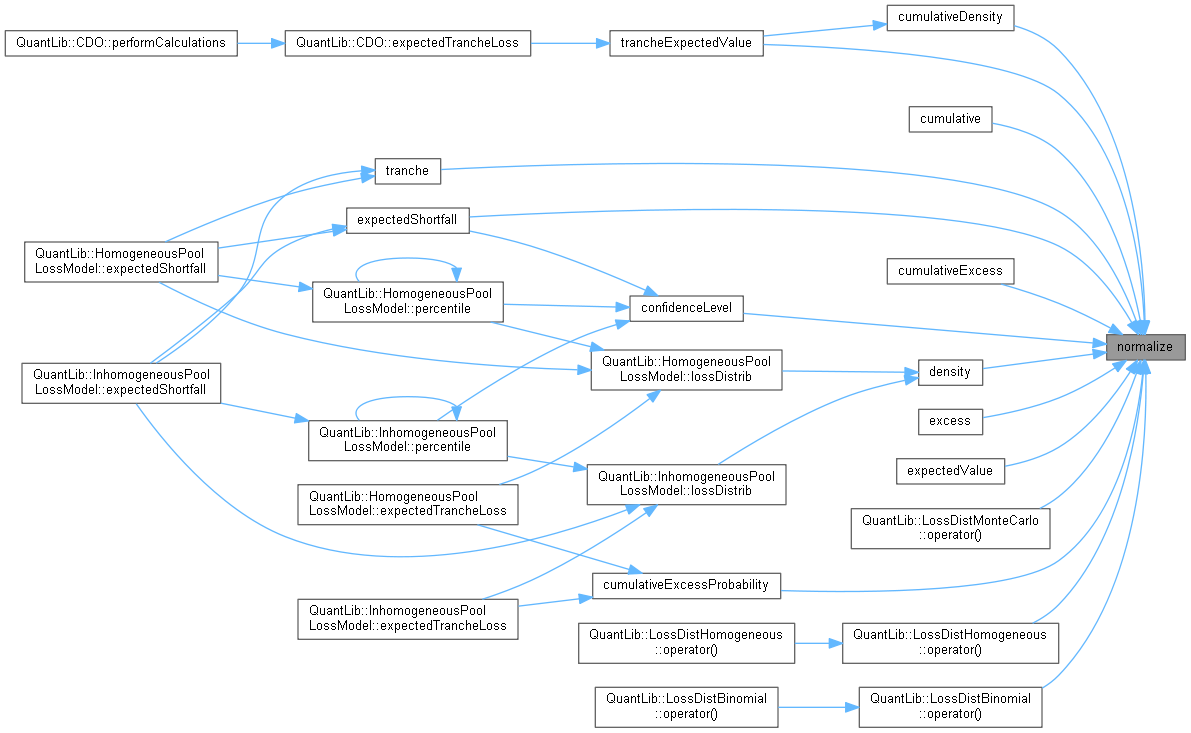

◆ normalize()

| void normalize | ( | ) |

◆ size()

| Size size | ( | ) | const |

◆ x() [1/2]

Definition at line 50 of file distribution.hpp.

◆ x() [2/2]

| std::vector< Real > & x | ( | ) |

◆ dx() [1/3]

◆ dx() [2/3]

| std::vector< Real > & dx | ( | ) |

Definition at line 53 of file distribution.hpp.

◆ dx() [3/3]

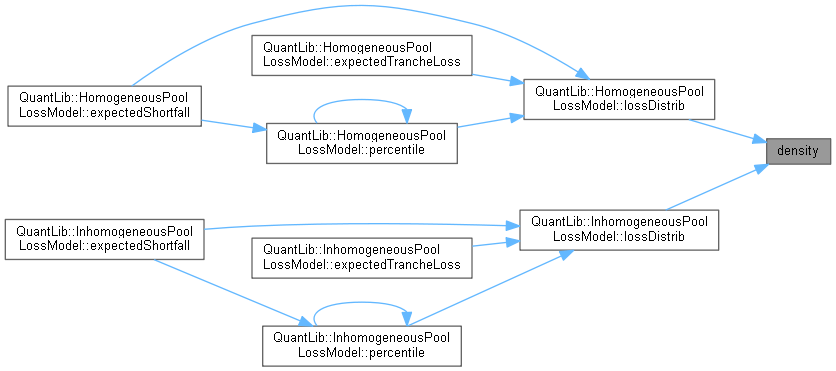

◆ density()

Definition at line 56 of file distribution.hpp.

Here is the call graph for this function: Here is the caller graph for this function:

Here is the caller graph for this function:

◆ cumulative()

◆ excess()

◆ cumulativeExcess()

◆ average()

Definition at line 72 of file distribution.hpp.

◆ confidenceLevel()

Definition at line 151 of file distribution.cpp.

Here is the call graph for this function: Here is the caller graph for this function:

Here is the caller graph for this function:

◆ cumulativeDensity()

Definition at line 220 of file distribution.cpp.

Here is the call graph for this function: Here is the caller graph for this function:

Here is the caller graph for this function:

◆ cumulativeExcessProbability()

Definition at line 204 of file distribution.cpp.

Here is the call graph for this function: Here is the caller graph for this function:

Here is the caller graph for this function:

◆ expectedValue() [1/2]

| Real expectedValue | ( | ) |

◆ trancheExpectedValue()

Definition at line 174 of file distribution.cpp.

Here is the call graph for this function: Here is the caller graph for this function:

Here is the caller graph for this function:

◆ expectedValue() [2/2]

◆ tranche()

Transform the loss distribution into the tranche loss distribution for losses L_T = min(L,D) - min(L,A). The effects are: 1) shift the distribution to the left by A, then 2) cut off at D-A, Pr(L_T > D-A) = 0 3) ensure Pr(L_T >= 0) = 1, i.e. a density spike at L_T = 0

Definition at line 236 of file distribution.cpp.

Here is the call graph for this function: Here is the caller graph for this function:

Here is the caller graph for this function:

◆ locate()

| int locate | ( | Real | x | ) |

Definition at line 55 of file distribution.cpp.

Here is the call graph for this function: Here is the caller graph for this function:

Here is the caller graph for this function:

◆ expectedShortfall()

Definition at line 328 of file distribution.cpp.

Here is the call graph for this function: Here is the caller graph for this function:

Here is the caller graph for this function:

Friends And Related Function Documentation

◆ ManipulateDistribution

|

friend |

Definition at line 39 of file distribution.hpp.

Member Data Documentation

◆ size_

|

private |

Definition at line 110 of file distribution.hpp.

◆ xmin_

|

private |

Definition at line 111 of file distribution.hpp.

◆ xmax_

|

private |

Definition at line 111 of file distribution.hpp.

◆ count_

|

private |

Definition at line 112 of file distribution.hpp.

◆ x_

|

private |

Definition at line 115 of file distribution.hpp.

◆ dx_

|

private |

Definition at line 115 of file distribution.hpp.

◆ density_

|

private |

Definition at line 120 of file distribution.hpp.

◆ cumulativeDensity_

|

private |

Definition at line 120 of file distribution.hpp.

◆ excessProbability_

|

private |

Definition at line 121 of file distribution.hpp.

◆ cumulativeExcessProbability_

|

private |

Definition at line 121 of file distribution.hpp.

◆ average_

|

private |

Definition at line 123 of file distribution.hpp.

◆ overFlow_

|

private |

Definition at line 125 of file distribution.hpp.

◆ underFlow_

|

private |

Definition at line 125 of file distribution.hpp.

◆ isNormalized_

|

private |

Definition at line 126 of file distribution.hpp.