Cumulative normal distribution function. More...

#include <normaldistribution.hpp>

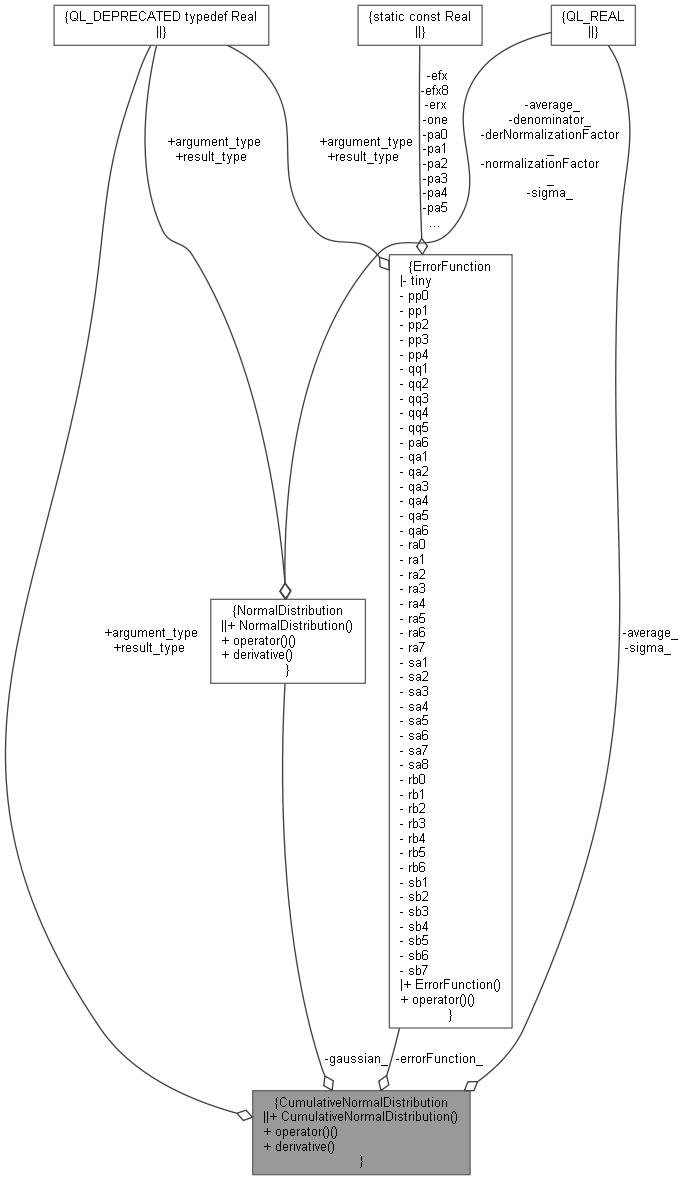

Collaboration diagram for CumulativeNormalDistribution:

Collaboration diagram for CumulativeNormalDistribution:

Public Member Functions | |

| CumulativeNormalDistribution (Real average=0.0, Real sigma=1.0) | |

| Real | operator() (Real x) const |

| Real | derivative (Real x) const |

Private Attributes | |

| Real | average_ |

| Real | sigma_ |

| NormalDistribution | gaussian_ |

| ErrorFunction | errorFunction_ |

Detailed Description

Cumulative normal distribution function.

Given x it provides an approximation to the integral of the gaussian normal distribution: formula here ...

For this implementation see M. Abramowitz and I. Stegun, Handbook of Mathematical Functions, Dover Publications, New York (1972)

Definition at line 68 of file normaldistribution.hpp.

Constructor & Destructor Documentation

◆ CumulativeNormalDistribution()

| CumulativeNormalDistribution | ( | Real | average = 0.0, |

| Real | sigma = 1.0 |

||

| ) |

Definition at line 287 of file normaldistribution.hpp.

Member Function Documentation

◆ operator()()

Definition at line 30 of file normaldistribution.cpp.

◆ derivative()

Member Data Documentation

◆ average_

|

private |

Definition at line 76 of file normaldistribution.hpp.

◆ sigma_

|

private |

Definition at line 76 of file normaldistribution.hpp.

◆ gaussian_

|

private |

Definition at line 77 of file normaldistribution.hpp.

◆ errorFunction_

|

private |

Definition at line 78 of file normaldistribution.hpp.