Fully annotated reference manual - version 1.8.13.0

Loading...

Searching...

No Matches

Exposure Aggregation and XVA Calculation. More...

#include <orea/aggregation/postprocess.hpp>

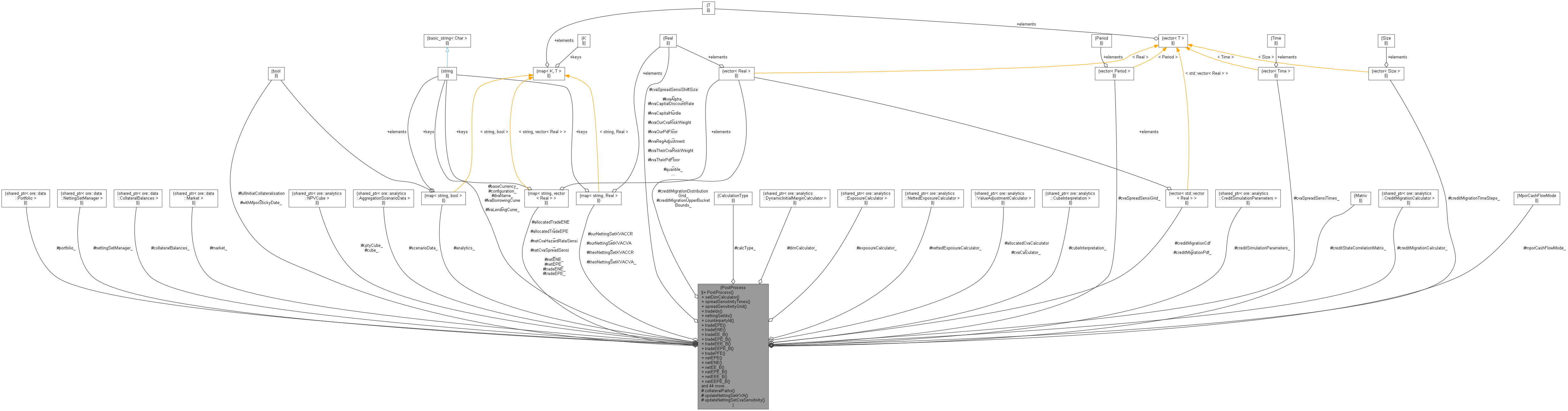

Collaboration diagram for PostProcess:

Collaboration diagram for PostProcess:Public Member Functions | |

| PostProcess (const QuantLib::ext::shared_ptr< Portfolio > &portfolio, const QuantLib::ext::shared_ptr< NettingSetManager > &nettingSetManager, const QuantLib::ext::shared_ptr< CollateralBalances > &collateralBalances, const QuantLib::ext::shared_ptr< Market > &market, const std::string &configuration, const QuantLib::ext::shared_ptr< NPVCube > &cube, const QuantLib::ext::shared_ptr< AggregationScenarioData > &scenarioData, const map< string, bool > &analytics, const string &baseCurrency, const string &allocationMethod, Real cvaMarginalAllocationLimit, Real quantile=0.95, const string &calculationType="Symmetric", const string &dvaName="", const string &fvaBorrowingCurve="", const string &fvaLendingCurve="", const QuantLib::ext::shared_ptr< DynamicInitialMarginCalculator > &dimCalculator=QuantLib::ext::shared_ptr< DynamicInitialMarginCalculator >(), const QuantLib::ext::shared_ptr< CubeInterpretation > &cubeInterpretation=QuantLib::ext::shared_ptr< CubeInterpretation >(), bool fullInitialCollateralisation=false, vector< Period > cvaSpreadSensiGrid={6 *Months, 1 *Years, 3 *Years, 5 *Years, 10 *Years}, Real cvaSpreadSensiShiftSize=0.0001, Real kvaCapitalDiscountRate=0.10, Real kvaAlpha=1.4, Real kvaRegAdjustment=12.5, Real kvaCapitalHurdle=0.012, Real kvaOurPdFloor=0.03, Real kvaTheirPdFloor=0.03, Real kvaOurCvaRiskWeight=0.05, Real kvaTheirCvaRiskWeight=0.05, const QuantLib::ext::shared_ptr< NPVCube > &cptyCube_=nullptr, const string &flipViewBorrowingCurvePostfix="_BORROW", const string &flipViewLendingCurvePostfix="_LEND", const QuantLib::ext::shared_ptr< CreditSimulationParameters > &creditSimulationParameters=nullptr, const std::vector< Real > &creditMigrationDistributionGrid={}, const std::vector< Size > &creditMigrationTimeSteps={}, const Matrix &creditStateCorrelationMatrix=Matrix(), bool withMporStickyDate=false, const MporCashFlowMode mporCashFlowMode=MporCashFlowMode::Unspecified) | |

| Constructor. More... | |

| void | setDimCalculator (QuantLib::ext::shared_ptr< DynamicInitialMarginCalculator > dimCalculator) |

| const vector< Real > & | spreadSensitivityTimes () |

| const vector< Period > & | spreadSensitivityGrid () |

| const std::map< string, Size > | tradeIds () |

| Return list of Trade IDs in the portfolio. More... | |

| const std::map< string, Size > | nettingSetIds () |

| Return list of netting set IDs in the portfolio. More... | |

| const map< string, string > & | counterpartyId () |

| Return the map of counterparty Ids. More... | |

| const vector< Real > & | tradeEPE (const string &tradeId) |

| Return trade level Expected Positive Exposure evolution. More... | |

| const vector< Real > & | tradeENE (const string &tradeId) |

| Return trade level Expected Negative Exposure evolution. More... | |

| const vector< Real > & | tradeEE_B (const string &tradeId) |

| Return trade level Basel Expected Exposure evolution. More... | |

| const Real & | tradeEPE_B (const string &tradeId) |

| Return trade level Basel Expected Positive Exposure evolution. More... | |

| const vector< Real > & | tradeEEE_B (const string &tradeId) |

| Return trade level Effective Expected Exposure evolution. More... | |

| const Real & | tradeEEPE_B (const string &tradeId) |

| Return trade level Effective Expected Positive Exposure evolution. More... | |

| const vector< Real > & | tradePFE (const string &tradeId) |

| Return trade level Potential Future Exposure evolution. More... | |

| const vector< Real > & | netEPE (const string &nettingSetId) |

| Return Netting Set Expected Positive Exposure evolution. More... | |

| const vector< Real > & | netENE (const string &nettingSetId) |

| Return Netting Set Expected Negative Exposure evolution. More... | |

| const vector< Real > & | netEE_B (const string &nettingSetId) |

| Return Netting Set Basel Expected Exposure evolution. More... | |

| const Real & | netEPE_B (const string &nettingSetId) |

| Return Netting Set Basel Expected Positive Exposure evolution. More... | |

| const vector< Real > & | netEEE_B (const string &nettingSetId) |

| Return Netting Set Effective Expected Exposure evolution. More... | |

| const Real & | netEEPE_B (const string &nettingSetId) |

| Return Netting Set Effective Expected Positive Exposure evolution. More... | |

| const vector< Real > & | netPFE (const string &nettingSetId) |

| Return Netting Set Potential Future Exposure evolution. More... | |

| const vector< Real > & | expectedCollateral (const string &nettingSetId) |

| Return the netting set's expected collateral evolution. More... | |

| const vector< Real > & | colvaIncrements (const string &nettingSetId) |

| Return the netting set's expected COLVA increments through time. More... | |

| const vector< Real > & | collateralFloorIncrements (const string &nettingSetId) |

| Return the netting set's expected Collateral Floor increments through time. More... | |

| const vector< Real > & | allocatedTradeEPE (const string &tradeId) |

| Return the trade EPE, allocated down from the netting set level. More... | |

| const vector< Real > & | allocatedTradeENE (const string &tradeId) |

| Return trade ENE, allocated down from the netting set level. More... | |

| vector< Real > | netCvaHazardRateSensitivity (const string &nettingSetId) |

| Return Netting Set CVA Hazard Rate Sensitivity vector. More... | |

| vector< Real > | netCvaSpreadSensitivity (const string &nettingSetId) |

| Return Netting Set CVA Spread Sensitivity vector. More... | |

| const std::map< std::string, std::vector< QuantLib::Real > > & | netCvaSpreadSensitivity () const |

| Return Netting Set CVA Spread Sensitivity vector. More... | |

| Real | tradeCVA (const string &tradeId) |

| Return trade (stand-alone) CVA. More... | |

| Real | tradeDVA (const string &tradeId) |

| Return trade (stand-alone) DVA. More... | |

| Real | tradeMVA (const string &tradeId) |

| Return trade (stand-alone) MVA. More... | |

| Real | tradeFBA (const string &tradeId) |

| Return trade (stand-alone) FBA (Funding Benefit Adjustment) More... | |

| Real | tradeFCA (const string &tradeId) |

| Return trade (stand-alone) FCA (Funding Cost Adjustment) More... | |

| Real | tradeFBA_exOwnSP (const string &tradeId) |

| Return trade (stand-alone) FBA (Funding Benefit Adjustment) excluding own survival probability. More... | |

| Real | tradeFCA_exOwnSP (const string &tradeId) |

| Return trade (stand-alone) FCA (Funding Cost Adjustment) excluding own survival probability. More... | |

| Real | tradeFBA_exAllSP (const string &tradeId) |

| Return trade (stand-alone) FBA (Funding Benefit Adjustment) excluding both survival probabilities. More... | |

| Real | tradeFCA_exAllSP (const string &tradeId) |

| Return trade (stand-alone) FCA (Funding Cost Adjustment) excluding both survival probabilities. More... | |

| Real | allocatedTradeCVA (const string &tradeId) |

| Return allocated trade CVA (trade CVAs add up to netting set CVA) More... | |

| Real | allocatedTradeDVA (const string &tradeId) |

| Return allocated trade DVA (trade DVAs add up to netting set DVA) More... | |

| Real | nettingSetCVA (const string &nettingSetId) |

| Return netting set CVA. More... | |

| Real | nettingSetDVA (const string &nettingSetId) |

| Return netting set DVA. More... | |

| Real | nettingSetMVA (const string &nettingSetId) |

| Return netting set MVA. More... | |

| Real | nettingSetFBA (const string &nettingSetId) |

| Return netting set FBA. More... | |

| Real | nettingSetFCA (const string &nettingSetId) |

| Return netting set FCA. More... | |

| Real | nettingSetOurKVACCR (const string &nettingSetId) |

| Return netting set KVA-CCR. More... | |

| Real | nettingSetTheirKVACCR (const string &nettingSetId) |

| Return netting set KVA-CCR from counterparty perspective. More... | |

| Real | nettingSetOurKVACVA (const string &nettingSetId) |

| Return netting set KVA-CVA. More... | |

| Real | nettingSetTheirKVACVA (const string &nettingSetId) |

| Return netting set KVA-CVA from counterparty perspective. More... | |

| Real | nettingSetFBA_exOwnSP (const string &nettingSetId) |

| Return netting set FBA excluding own survival probability. More... | |

| Real | nettingSetFCA_exOwnSP (const string &nettingSetId) |

| Return netting set FCA excluding own survival probability. More... | |

| Real | nettingSetFBA_exAllSP (const string &nettingSetId) |

| Return netting set FBA excluding both survival probabilities. More... | |

| Real | nettingSetFCA_exAllSP (const string &nettingSetId) |

| Return netting set FCA excluding both survival probabilities. More... | |

| Real | nettingSetCOLVA (const string &nettingSetId) |

| Return netting set COLVA. More... | |

| Real | nettingSetCollateralFloor (const string &nettingSetId) |

| Return netting set Collateral Floor value. More... | |

| const QuantLib::ext::shared_ptr< NPVCube > & | cube () |

| Inspector for the input NPV cube (by trade, time, scenario) More... | |

| const QuantLib::ext::shared_ptr< NPVCube > & | cptyCube () |

| Inspector for the input Cpty cube (by name, time, scenario) More... | |

| const QuantLib::ext::shared_ptr< NPVCube > & | netCube () |

| Return the for the input NPV cube after netting and collateral (by netting set, time, scenario) More... | |

| void | exportDimEvolution (ore::data::Report &dimEvolutionReport) |

| Return the dynamic initial margin cube (regression approach) More... | |

| void | exportDimRegression (const std::string &nettingSet, const std::vector< Size > &timeSteps, const std::vector< QuantLib::ext::shared_ptr< ore::data::Report > > &dimRegReports) |

| Write DIM as a function of sample netting set NPV for a given time step. More... | |

| QuantLib::Real | cvaSpreadSensiShiftSize () |

| get the cvaSpreadSensiShiftSize More... | |

| const std::vector< Real > & | creditMigrationUpperBucketBounds () const |

| get the credit migration pnl distributions for each time step More... | |

| const std::vector< std::vector< Real > > & | creditMigrationCdf () const |

| const std::vector< std::vector< Real > > & | creditMigrationPdf () const |

Protected Member Functions | |

| QuantLib::ext::shared_ptr< vector< QuantLib::ext::shared_ptr< CollateralAccount > > > | collateralPaths (const string &nettingSetId, const QuantLib::ext::shared_ptr< NettingSetManager > &nettingSetManager, const QuantLib::ext::shared_ptr< Market > &market, const std::string &configuration, const QuantLib::ext::shared_ptr< AggregationScenarioData > &scenarioData, Size dates, Size samples, const vector< vector< Real > > &nettingSetValue, Real nettingSetValueToday, const Date &nettingSetMaturity) |

| Helper function to return the collateral account evolution for a given netting set. More... | |

| void | updateNettingSetKVA () |

| void | updateNettingSetCvaSensitivity () |

Exposure Aggregation and XVA Calculation.

This class aggregates NPV cube data, computes exposure statistics and various XVAs, all at trade and netting set level:

1) Exposures

2) Dynamic Initial Margin via regression

3) XVAs:

4) Allocation from netting set to trade level such that allocated contributions add up to the netting set

All analytics are precomputed when the class constructor is called. A number of inspectors described below then return the individual analytics results.

Note:

Definition at line 93 of file postprocess.hpp.

| PostProcess | ( | const QuantLib::ext::shared_ptr< Portfolio > & | portfolio, |

| const QuantLib::ext::shared_ptr< NettingSetManager > & | nettingSetManager, | ||

| const QuantLib::ext::shared_ptr< CollateralBalances > & | collateralBalances, | ||

| const QuantLib::ext::shared_ptr< Market > & | market, | ||

| const std::string & | configuration, | ||

| const QuantLib::ext::shared_ptr< NPVCube > & | cube, | ||

| const QuantLib::ext::shared_ptr< AggregationScenarioData > & | scenarioData, | ||

| const map< string, bool > & | analytics, | ||

| const string & | baseCurrency, | ||

| const string & | allocationMethod, | ||

| Real | cvaMarginalAllocationLimit, | ||

| Real | quantile = 0.95, |

||

| const string & | calculationType = "Symmetric", |

||

| const string & | dvaName = "", |

||

| const string & | fvaBorrowingCurve = "", |

||

| const string & | fvaLendingCurve = "", |

||

| const QuantLib::ext::shared_ptr< DynamicInitialMarginCalculator > & | dimCalculator = QuantLib::ext::shared_ptr<DynamicInitialMarginCalculator>(), |

||

| const QuantLib::ext::shared_ptr< CubeInterpretation > & | cubeInterpretation = QuantLib::ext::shared_ptr<CubeInterpretation>(), |

||

| bool | fullInitialCollateralisation = false, |

||

| vector< Period > | cvaSpreadSensiGrid = {6 * Months, 1 * Years, 3 * Years, 5 * Years, 10 * Years}, |

||

| Real | cvaSpreadSensiShiftSize = 0.0001, |

||

| Real | kvaCapitalDiscountRate = 0.10, |

||

| Real | kvaAlpha = 1.4, |

||

| Real | kvaRegAdjustment = 12.5, |

||

| Real | kvaCapitalHurdle = 0.012, |

||

| Real | kvaOurPdFloor = 0.03, |

||

| Real | kvaTheirPdFloor = 0.03, |

||

| Real | kvaOurCvaRiskWeight = 0.05, |

||

| Real | kvaTheirCvaRiskWeight = 0.05, |

||

| const QuantLib::ext::shared_ptr< NPVCube > & | cptyCube_ = nullptr, |

||

| const string & | flipViewBorrowingCurvePostfix = "_BORROW", |

||

| const string & | flipViewLendingCurvePostfix = "_LEND", |

||

| const QuantLib::ext::shared_ptr< CreditSimulationParameters > & | creditSimulationParameters = nullptr, |

||

| const std::vector< Real > & | creditMigrationDistributionGrid = {}, |

||

| const std::vector< Size > & | creditMigrationTimeSteps = {}, |

||

| const Matrix & | creditStateCorrelationMatrix = Matrix(), |

||

| bool | withMporStickyDate = false, |

||

| const MporCashFlowMode | mporCashFlowMode = MporCashFlowMode::Unspecified |

||

| ) |

Constructor.

| portfolio | Trade portfolio to identify e.g. netting set, maturity, break dates for each trade |

| nettingSetManager | Netting set manager to access CSA details for each netting set |

| collateralBalances | Collateral balances (VM, IM, IA) |

| market | Market data object to access e.g. discounting and funding curves |

| configuration | Market configuration to use |

| cube | Input NPV Cube |

| scenarioData | Subset of simulated market data, index fixings and FX spot rates, associated with the NPV cube |

| analytics | Selection of analytics to be produced |

| baseCurrency | Expression currency for all results |

| allocationMethod | Method to be used for Exposure/XVA allocation down to trade level |

| cvaMarginalAllocationLimit | Cutoff parameter for the marginal allocation method below which we switch to equal distribution |

| quantile | Quantile for Potential Future Exposure output |

| calculationType | Collateral calculation type to be used, see class CollateralExposureHelper |

| dvaName | Credit curve name to be used for "our" credit risk in DVA calculations |

| fvaBorrowingCurve | Borrowing curve name to be used in FVA calculations |

| fvaLendingCurve | Lending curve name to be used in FVA calculations |

| dimCalculator | Dynamic Initial Margin Calculator |

| cubeInterpretation | Interpreter for cube storage (where to find which data items) |

| fullInitialCollateralisation | Assume t=0 collateral balance equals NPV (set to 0 if false) |

| cvaSpreadSensiGrid | CVA spread sensitivity grid |

| cvaSpreadSensiShiftSize | CVA spread sensitivity shift size |

| kvaCapitalDiscountRate | own capital discounting rate for discounting expected capital for KVA |

| kvaAlpha | alpha to adjust EEPE to give EAD for risk capital |

| kvaRegAdjustment | regulatory adjustment, 1/min cap requirement |

| kvaCapitalHurdle | Cost of Capital for KVA = regulatory adjustment x capital hurdle |

| kvaOurPdFloor | Our KVA PD floor |

| kvaTheirPdFloor | Their KVA PD floor |

| kvaOurCvaRiskWeight | Our KVA CVA Risk Weight |

| kvaTheirCvaRiskWeight | Their KVA CVA Risk Weight, |

| cptyCube_ | Input Counterparty Cube |

| flipViewBorrowingCurvePostfix | Postfix for flipView borrowing curve for fva |

| flipViewLendingCurvePostfix | Postfix for flipView lending curve for fva |

| creditSimulationParameters | Credit simulation parameters |

| creditMigrationDistributionGrid | Credit simulation distribution grid |

| creditMigrationTimeSteps | Credit simulation time steps |

| creditStateCorrelationMatrix | Credit State correlation matrix |

| withMporStickyDate | If set to true, cash flows in the margin period of risk are ignored in the collateral modelling |

| mporCashFlowMode | Treatment of cash flows over the margin period of risk |

Definition at line 55 of file postprocess.cpp.

Here is the call graph for this function:| void setDimCalculator | ( | QuantLib::ext::shared_ptr< DynamicInitialMarginCalculator > | dimCalculator | ) |

Definition at line 174 of file postprocess.hpp.

| const vector< Real > & spreadSensitivityTimes | ( | ) |

Definition at line 178 of file postprocess.hpp.

| const vector< Period > & spreadSensitivityGrid | ( | ) |

Definition at line 179 of file postprocess.hpp.

| const std::map< string, Size > tradeIds | ( | ) |

Return list of Trade IDs in the portfolio.

Definition at line 182 of file postprocess.hpp.

Here is the call graph for this function: Here is the caller graph for this function:| const std::map< string, Size > nettingSetIds | ( | ) |

Return list of netting set IDs in the portfolio.

Definition at line 186 of file postprocess.hpp.

Here is the call graph for this function: Here is the caller graph for this function:| const map< string, string > & counterpartyId | ( | ) |

Return the map of counterparty Ids.

Definition at line 190 of file postprocess.hpp.

Here is the caller graph for this function:| const vector< Real > & tradeEPE | ( | const string & | tradeId | ) |

Return trade level Expected Positive Exposure evolution.

Definition at line 594 of file postprocess.cpp.

| const vector< Real > & tradeENE | ( | const string & | tradeId | ) |

Return trade level Expected Negative Exposure evolution.

Definition at line 599 of file postprocess.cpp.

| const vector< Real > & tradeEE_B | ( | const string & | tradeId | ) |

Return trade level Basel Expected Exposure evolution.

Definition at line 604 of file postprocess.cpp.

| const Real & tradeEPE_B | ( | const string & | tradeId | ) |

Return trade level Basel Expected Positive Exposure evolution.

Definition at line 608 of file postprocess.cpp.

| const vector< Real > & tradeEEE_B | ( | const string & | tradeId | ) |

Return trade level Effective Expected Exposure evolution.

Definition at line 612 of file postprocess.cpp.

| const Real & tradeEEPE_B | ( | const string & | tradeId | ) |

Return trade level Effective Expected Positive Exposure evolution.

Definition at line 616 of file postprocess.cpp.

| const vector< Real > & tradePFE | ( | const string & | tradeId | ) |

Return trade level Potential Future Exposure evolution.

Definition at line 620 of file postprocess.cpp.

| const vector< Real > & netEPE | ( | const string & | nettingSetId | ) |

Return Netting Set Expected Positive Exposure evolution.

Definition at line 624 of file postprocess.cpp.

| const vector< Real > & netENE | ( | const string & | nettingSetId | ) |

Return Netting Set Expected Negative Exposure evolution.

Definition at line 630 of file postprocess.cpp.

| const vector< Real > & netEE_B | ( | const string & | nettingSetId | ) |

Return Netting Set Basel Expected Exposure evolution.

Definition at line 650 of file postprocess.cpp.

| const Real & netEPE_B | ( | const string & | nettingSetId | ) |

Return Netting Set Basel Expected Positive Exposure evolution.

Definition at line 654 of file postprocess.cpp.

| const vector< Real > & netEEE_B | ( | const string & | nettingSetId | ) |

Return Netting Set Effective Expected Exposure evolution.

Definition at line 658 of file postprocess.cpp.

| const Real & netEEPE_B | ( | const string & | nettingSetId | ) |

Return Netting Set Effective Expected Positive Exposure evolution.

Definition at line 662 of file postprocess.cpp.

| const vector< Real > & netPFE | ( | const string & | nettingSetId | ) |

Return Netting Set Potential Future Exposure evolution.

Definition at line 666 of file postprocess.cpp.

| const vector< Real > & expectedCollateral | ( | const string & | nettingSetId | ) |

Return the netting set's expected collateral evolution.

Definition at line 670 of file postprocess.cpp.

| const vector< Real > & colvaIncrements | ( | const string & | nettingSetId | ) |

Return the netting set's expected COLVA increments through time.

Definition at line 674 of file postprocess.cpp.

| const vector< Real > & collateralFloorIncrements | ( | const string & | nettingSetId | ) |

Return the netting set's expected Collateral Floor increments through time.

Definition at line 678 of file postprocess.cpp.

| const vector< Real > & allocatedTradeEPE | ( | const string & | tradeId | ) |

Return the trade EPE, allocated down from the netting set level.

Definition at line 682 of file postprocess.cpp.

| const vector< Real > & allocatedTradeENE | ( | const string & | tradeId | ) |

Return trade ENE, allocated down from the netting set level.

Definition at line 688 of file postprocess.cpp.

| vector< Real > netCvaHazardRateSensitivity | ( | const string & | nettingSetId | ) |

Return Netting Set CVA Hazard Rate Sensitivity vector.

Definition at line 636 of file postprocess.cpp.

| vector< Real > netCvaSpreadSensitivity | ( | const string & | nettingSetId | ) |

Return Netting Set CVA Spread Sensitivity vector.

Definition at line 643 of file postprocess.cpp.

| const std::map< std::string, std::vector< QuantLib::Real > > & netCvaSpreadSensitivity | ( | ) | const |

| Real tradeCVA | ( | const string & | tradeId | ) |

Return trade (stand-alone) CVA.

Definition at line 694 of file postprocess.cpp.

| Real tradeDVA | ( | const string & | tradeId | ) |

Return trade (stand-alone) DVA.

Definition at line 698 of file postprocess.cpp.

| Real tradeMVA | ( | const string & | tradeId | ) |

Return trade (stand-alone) MVA.

Definition at line 702 of file postprocess.cpp.

| Real tradeFBA | ( | const string & | tradeId | ) |

Return trade (stand-alone) FBA (Funding Benefit Adjustment)

Definition at line 706 of file postprocess.cpp.

| Real tradeFCA | ( | const string & | tradeId | ) |

Return trade (stand-alone) FCA (Funding Cost Adjustment)

Definition at line 710 of file postprocess.cpp.

| Real tradeFBA_exOwnSP | ( | const string & | tradeId | ) |

Return trade (stand-alone) FBA (Funding Benefit Adjustment) excluding own survival probability.

Definition at line 714 of file postprocess.cpp.

| Real tradeFCA_exOwnSP | ( | const string & | tradeId | ) |

Return trade (stand-alone) FCA (Funding Cost Adjustment) excluding own survival probability.

Definition at line 718 of file postprocess.cpp.

| Real tradeFBA_exAllSP | ( | const string & | tradeId | ) |

Return trade (stand-alone) FBA (Funding Benefit Adjustment) excluding both survival probabilities.

Definition at line 722 of file postprocess.cpp.

| Real tradeFCA_exAllSP | ( | const string & | tradeId | ) |

Return trade (stand-alone) FCA (Funding Cost Adjustment) excluding both survival probabilities.

Definition at line 726 of file postprocess.cpp.

| Real allocatedTradeCVA | ( | const string & | tradeId | ) |

Return allocated trade CVA (trade CVAs add up to netting set CVA)

Definition at line 793 of file postprocess.cpp.

| Real allocatedTradeDVA | ( | const string & | tradeId | ) |

Return allocated trade DVA (trade DVAs add up to netting set DVA)

Definition at line 797 of file postprocess.cpp.

| Real nettingSetCVA | ( | const string & | nettingSetId | ) |

Return netting set CVA.

Definition at line 730 of file postprocess.cpp.

| Real nettingSetDVA | ( | const string & | nettingSetId | ) |

Return netting set DVA.

Definition at line 734 of file postprocess.cpp.

| Real nettingSetMVA | ( | const string & | nettingSetId | ) |

Return netting set MVA.

Definition at line 738 of file postprocess.cpp.

| Real nettingSetFBA | ( | const string & | nettingSetId | ) |

Return netting set FBA.

Definition at line 743 of file postprocess.cpp.

| Real nettingSetFCA | ( | const string & | nettingSetId | ) |

Return netting set FCA.

Definition at line 748 of file postprocess.cpp.

| Real nettingSetOurKVACCR | ( | const string & | nettingSetId | ) |

Return netting set KVA-CCR.

Definition at line 753 of file postprocess.cpp.

| Real nettingSetTheirKVACCR | ( | const string & | nettingSetId | ) |

Return netting set KVA-CCR from counterparty perspective.

Definition at line 759 of file postprocess.cpp.

| Real nettingSetOurKVACVA | ( | const string & | nettingSetId | ) |

Return netting set KVA-CVA.

Definition at line 765 of file postprocess.cpp.

| Real nettingSetTheirKVACVA | ( | const string & | nettingSetId | ) |

Return netting set KVA-CVA from counterparty perspective.

Definition at line 771 of file postprocess.cpp.

| Real nettingSetFBA_exOwnSP | ( | const string & | nettingSetId | ) |

Return netting set FBA excluding own survival probability.

Definition at line 777 of file postprocess.cpp.

| Real nettingSetFCA_exOwnSP | ( | const string & | nettingSetId | ) |

Return netting set FCA excluding own survival probability.

Definition at line 781 of file postprocess.cpp.

| Real nettingSetFBA_exAllSP | ( | const string & | nettingSetId | ) |

Return netting set FBA excluding both survival probabilities.

Definition at line 785 of file postprocess.cpp.

| Real nettingSetFCA_exAllSP | ( | const string & | nettingSetId | ) |

Return netting set FCA excluding both survival probabilities.

Definition at line 789 of file postprocess.cpp.

| Real nettingSetCOLVA | ( | const string & | nettingSetId | ) |

Return netting set COLVA.

Definition at line 801 of file postprocess.cpp.

| Real nettingSetCollateralFloor | ( | const string & | nettingSetId | ) |

Return netting set Collateral Floor value.

Definition at line 805 of file postprocess.cpp.

| const QuantLib::ext::shared_ptr< NPVCube > & cube | ( | ) |

Inspector for the input NPV cube (by trade, time, scenario)

Definition at line 297 of file postprocess.hpp.

Here is the caller graph for this function:| const QuantLib::ext::shared_ptr< NPVCube > & cptyCube | ( | ) |

Inspector for the input Cpty cube (by name, time, scenario)

Definition at line 299 of file postprocess.hpp.

| const QuantLib::ext::shared_ptr< NPVCube > & netCube | ( | ) |

Return the for the input NPV cube after netting and collateral (by netting set, time, scenario)

Definition at line 301 of file postprocess.hpp.

Here is the caller graph for this function:| void exportDimEvolution | ( | ore::data::Report & | dimEvolutionReport | ) |

Return the dynamic initial margin cube (regression approach)

Write average (over samples) DIM evolution through time for all netting sets

Definition at line 809 of file postprocess.cpp.

| void exportDimRegression | ( | const std::string & | nettingSet, |

| const std::vector< Size > & | timeSteps, | ||

| const std::vector< QuantLib::ext::shared_ptr< ore::data::Report > > & | dimRegReports | ||

| ) |

Write DIM as a function of sample netting set NPV for a given time step.

Definition at line 813 of file postprocess.cpp.

| QuantLib::Real cvaSpreadSensiShiftSize | ( | ) |

| const std::vector< Real > & creditMigrationUpperBucketBounds | ( | ) | const |

get the credit migration pnl distributions for each time step

Definition at line 314 of file postprocess.hpp.

| const std::vector< std::vector< Real > > & creditMigrationCdf | ( | ) | const |

Definition at line 315 of file postprocess.hpp.

| const std::vector< std::vector< Real > > & creditMigrationPdf | ( | ) | const |

Definition at line 316 of file postprocess.hpp.

|

protected |

Helper function to return the collateral account evolution for a given netting set.

|

protected |

Definition at line 335 of file postprocess.cpp.

Here is the call graph for this function: Here is the caller graph for this function:

|

protected |

Definition at line 545 of file postprocess.cpp.

Here is the call graph for this function: Here is the caller graph for this function:

|

protected |

Definition at line 330 of file postprocess.hpp.

|

protected |

Definition at line 331 of file postprocess.hpp.

|

protected |

Definition at line 332 of file postprocess.hpp.

|

protected |

Definition at line 333 of file postprocess.hpp.

|

protected |

Definition at line 334 of file postprocess.hpp.

|

protected |

Definition at line 335 of file postprocess.hpp.

|

protected |

Definition at line 336 of file postprocess.hpp.

|

protected |

Definition at line 337 of file postprocess.hpp.

|

protected |

Definition at line 338 of file postprocess.hpp.

|

protected |

Definition at line 340 of file postprocess.hpp.

|

protected |

Definition at line 340 of file postprocess.hpp.

|

protected |

Definition at line 341 of file postprocess.hpp.

|

protected |

Definition at line 341 of file postprocess.hpp.

|

protected |

Definition at line 342 of file postprocess.hpp.

|

protected |

Definition at line 342 of file postprocess.hpp.

|

protected |

Definition at line 343 of file postprocess.hpp.

|

protected |

Definition at line 343 of file postprocess.hpp.

|

protected |

Definition at line 343 of file postprocess.hpp.

|

protected |

Definition at line 343 of file postprocess.hpp.

|

protected |

Definition at line 344 of file postprocess.hpp.

|

protected |

Definition at line 344 of file postprocess.hpp.

|

protected |

Definition at line 348 of file postprocess.hpp.

|

protected |

Definition at line 349 of file postprocess.hpp.

|

protected |

Definition at line 350 of file postprocess.hpp.

|

protected |

Definition at line 351 of file postprocess.hpp.

|

protected |

Definition at line 352 of file postprocess.hpp.

|

protected |

Definition at line 353 of file postprocess.hpp.

|

protected |

Definition at line 355 of file postprocess.hpp.

|

protected |

Definition at line 356 of file postprocess.hpp.

|

protected |

Definition at line 357 of file postprocess.hpp.

|

protected |

Definition at line 358 of file postprocess.hpp.

|

protected |

Definition at line 359 of file postprocess.hpp.

|

protected |

Definition at line 360 of file postprocess.hpp.

|

protected |

Definition at line 361 of file postprocess.hpp.

|

protected |

Definition at line 362 of file postprocess.hpp.

|

protected |

Definition at line 363 of file postprocess.hpp.

|

protected |

Definition at line 364 of file postprocess.hpp.

|

protected |

Definition at line 365 of file postprocess.hpp.

|

protected |

Definition at line 366 of file postprocess.hpp.

|

protected |

Definition at line 367 of file postprocess.hpp.

|

protected |

Definition at line 368 of file postprocess.hpp.

|

protected |

Definition at line 369 of file postprocess.hpp.

|

protected |

Definition at line 370 of file postprocess.hpp.

|

protected |

Definition at line 371 of file postprocess.hpp.

|

protected |

Definition at line 372 of file postprocess.hpp.

|

protected |

Definition at line 374 of file postprocess.hpp.

|

protected |

Definition at line 375 of file postprocess.hpp.

|

protected |

Definition at line 376 of file postprocess.hpp.

|

protected |

Definition at line 377 of file postprocess.hpp.

|

protected |

Definition at line 378 of file postprocess.hpp.

|

protected |

Definition at line 379 of file postprocess.hpp.

|

protected |

Definition at line 380 of file postprocess.hpp.

|

protected |

Definition at line 381 of file postprocess.hpp.

|

protected |

Definition at line 382 of file postprocess.hpp.

|

protected |

Definition at line 383 of file postprocess.hpp.