Fully annotated reference manual - version 1.8.13.0

Loading...

Searching...

No Matches

#include <ored/marketdata/market.hpp>

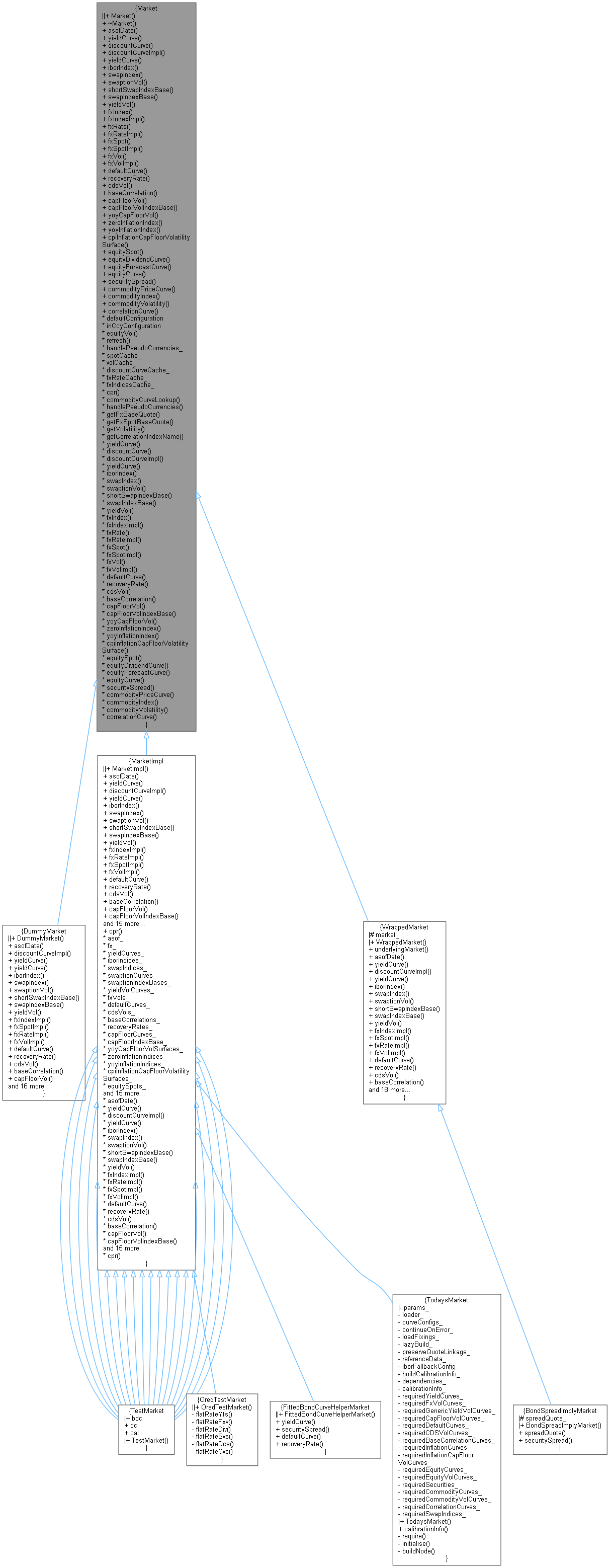

Inheritance diagram for Market: Collaboration diagram for Market:

Inheritance diagram for Market: Collaboration diagram for Market:Public Member Functions | |

| Market (const bool handlePseudoCurrencies) | |

| Constructor. More... | |

| virtual | ~Market () |

| Destructor. More... | |

| virtual Date | asofDate () const =0 |

| Get the asof Date. More... | |

Yield Curves | |

| virtual Handle< YieldTermStructure > | yieldCurve (const YieldCurveType &type, const string &name, const string &configuration=Market::defaultConfiguration) const =0 |

| Handle< YieldTermStructure > | discountCurve (const string &ccy, const string &configuration=Market::defaultConfiguration) const |

| virtual Handle< YieldTermStructure > | discountCurveImpl (const string &ccy, const string &configuration=Market::defaultConfiguration) const =0 |

| virtual Handle< YieldTermStructure > | yieldCurve (const string &name, const string &configuration=Market::defaultConfiguration) const =0 |

| virtual Handle< IborIndex > | iborIndex (const string &indexName, const string &configuration=Market::defaultConfiguration) const =0 |

| virtual Handle< SwapIndex > | swapIndex (const string &indexName, const string &configuration=Market::defaultConfiguration) const =0 |

Swaptions | |

| virtual Handle< SwaptionVolatilityStructure > | swaptionVol (const string &key, const string &configuration=Market::defaultConfiguration) const =0 |

| virtual string | shortSwapIndexBase (const string &key, const string &configuration=Market::defaultConfiguration) const =0 |

| virtual string | swapIndexBase (const string &key, const string &configuration=Market::defaultConfiguration) const =0 |

Yield volatilities | |

| virtual Handle< SwaptionVolatilityStructure > | yieldVol (const string &securityID, const string &configuration=Market::defaultConfiguration) const =0 |

Foreign Exchange | |

| QuantLib::Handle< QuantExt::FxIndex > | fxIndex (const string &fxIndex, const string &configuration=Market::defaultConfiguration) const |

| virtual QuantLib::Handle< QuantExt::FxIndex > | fxIndexImpl (const string &fxIndex, const string &configuration=Market::defaultConfiguration) const =0 |

| Handle< Quote > | fxRate (const string &ccypair, const string &configuration=Market::defaultConfiguration) const |

| virtual Handle< Quote > | fxRateImpl (const string &ccypair, const string &configuration=Market::defaultConfiguration) const =0 |

| Handle< Quote > | fxSpot (const string &ccypair, const string &configuration=Market::defaultConfiguration) const |

| virtual Handle< Quote > | fxSpotImpl (const string &ccypair, const string &configuration=Market::defaultConfiguration) const =0 |

| Handle< BlackVolTermStructure > | fxVol (const string &ccypair, const string &configuration=Market::defaultConfiguration) const |

| virtual Handle< BlackVolTermStructure > | fxVolImpl (const string &ccypair, const string &configuration=Market::defaultConfiguration) const =0 |

Default Curves and Recovery Rates | |

| virtual Handle< QuantExt::CreditCurve > | defaultCurve (const string &, const string &configuration=Market::defaultConfiguration) const =0 |

| virtual Handle< Quote > | recoveryRate (const string &, const string &configuration=Market::defaultConfiguration) const =0 |

(Index) CDS Option volatilities | |

| virtual Handle< QuantExt::CreditVolCurve > | cdsVol (const string &, const string &configuration=Market::defaultConfiguration) const =0 |

Base Correlation term structures | |

| virtual Handle< QuantExt::BaseCorrelationTermStructure > | baseCorrelation (const string &, const string &configuration=Market::defaultConfiguration) const =0 |

Stripped Cap/Floor volatilities i.e. caplet/floorlet volatilities | |

| virtual Handle< OptionletVolatilityStructure > | capFloorVol (const string &key, const string &configuration=Market::defaultConfiguration) const =0 |

| virtual std::pair< std::string, QuantLib::Period > | capFloorVolIndexBase (const string &key, const string &configuration=Market::defaultConfiguration) const =0 |

Stripped YoY Inflation Cap/Floor volatilities i.e. caplet/floorlet volatilities | |

| virtual Handle< QuantExt::YoYOptionletVolatilitySurface > | yoyCapFloorVol (const string &indexName, const string &configuration=Market::defaultConfiguration) const =0 |

| virtual Handle< ZeroInflationIndex > | zeroInflationIndex (const string &indexName, const string &configuration=Market::defaultConfiguration) const =0 |

| Inflation Indexes. More... | |

| virtual Handle< YoYInflationIndex > | yoyInflationIndex (const string &indexName, const string &configuration=Market::defaultConfiguration) const =0 |

| virtual Handle< CPIVolatilitySurface > | cpiInflationCapFloorVolatilitySurface (const string &indexName, const string &configuration=Market::defaultConfiguration) const =0 |

| CPI Inflation Cap Floor Volatility Surfaces. More... | |

Equity curves | |

| virtual Handle< Quote > | equitySpot (const string &eqName, const string &configuration=Market::defaultConfiguration) const =0 |

| virtual Handle< YieldTermStructure > | equityDividendCurve (const string &eqName, const string &configuration=Market::defaultConfiguration) const =0 |

| virtual Handle< YieldTermStructure > | equityForecastCurve (const string &eqName, const string &configuration=Market::defaultConfiguration) const =0 |

| virtual Handle< QuantExt::EquityIndex2 > | equityCurve (const string &eqName, const string &configuration=Market::defaultConfiguration) const =0 |

BondSpreads | |

| virtual Handle< Quote > | securitySpread (const string &securityID, const string &configuration=Market::defaultConfiguration) const =0 |

Commodity price curves and indices | |

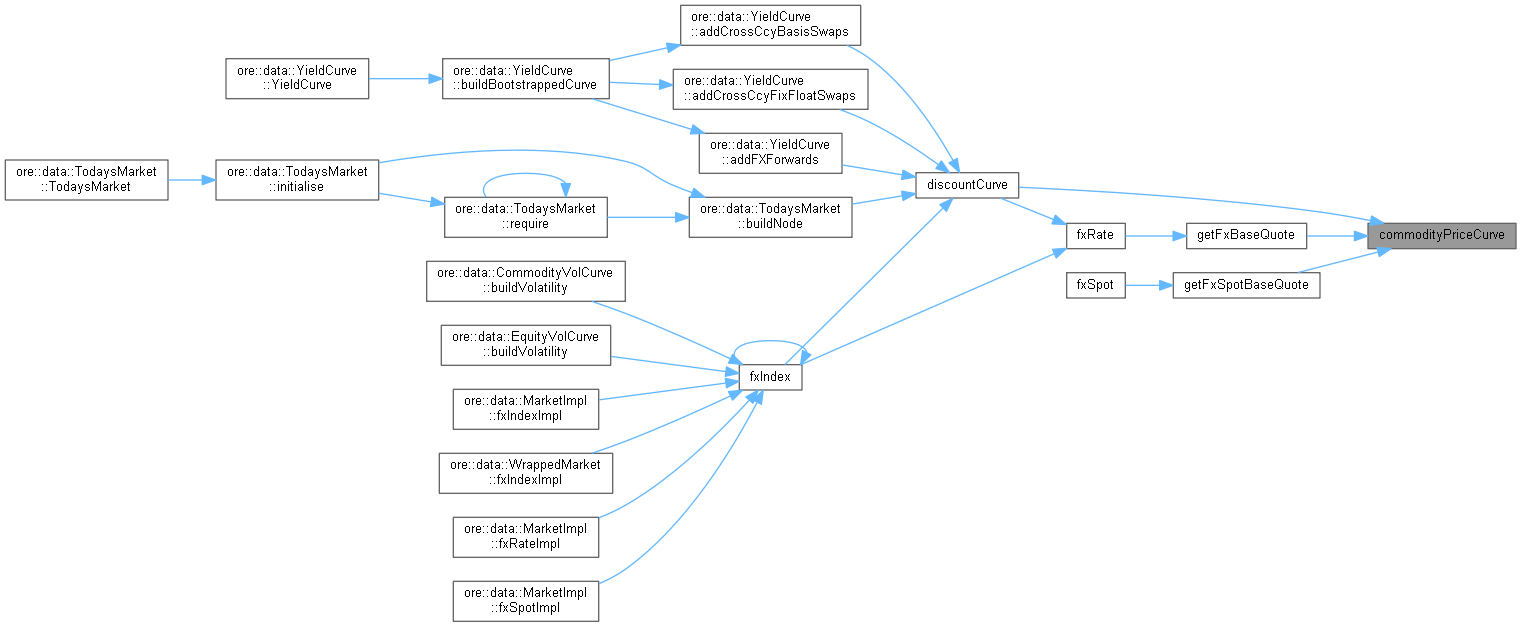

| virtual QuantLib::Handle< QuantExt::PriceTermStructure > | commodityPriceCurve (const std::string &commodityName, const std::string &configuration=Market::defaultConfiguration) const =0 |

| virtual QuantLib::Handle< QuantExt::CommodityIndex > | commodityIndex (const std::string &commodityName, const std::string &configuration=Market::defaultConfiguration) const =0 |

Commodity volatility | |

| virtual QuantLib::Handle< QuantLib::BlackVolTermStructure > | commodityVolatility (const std::string &commodityName, const std::string &configuration=Market::defaultConfiguration) const =0 |

Correlation | |

| virtual QuantLib::Handle< QuantExt::CorrelationTermStructure > | correlationCurve (const std::string &index1, const std::string &index2, const std::string &configuration=Market::defaultConfiguration) const =0 |

Equity volatilities | |

| static const string | defaultConfiguration = "default" |

| Default configuration label. More... | |

| static const string | inCcyConfiguration = "inccy" |

| InCcy configuration label. More... | |

| virtual Handle< BlackVolTermStructure > | equityVol (const string &eqName, const string &configuration=Market::defaultConfiguration) const =0 |

| virtual void | refresh (const string &) |

| Refresh term structures for a given configuration. More... | |

Conditional Prepayment Rates | |

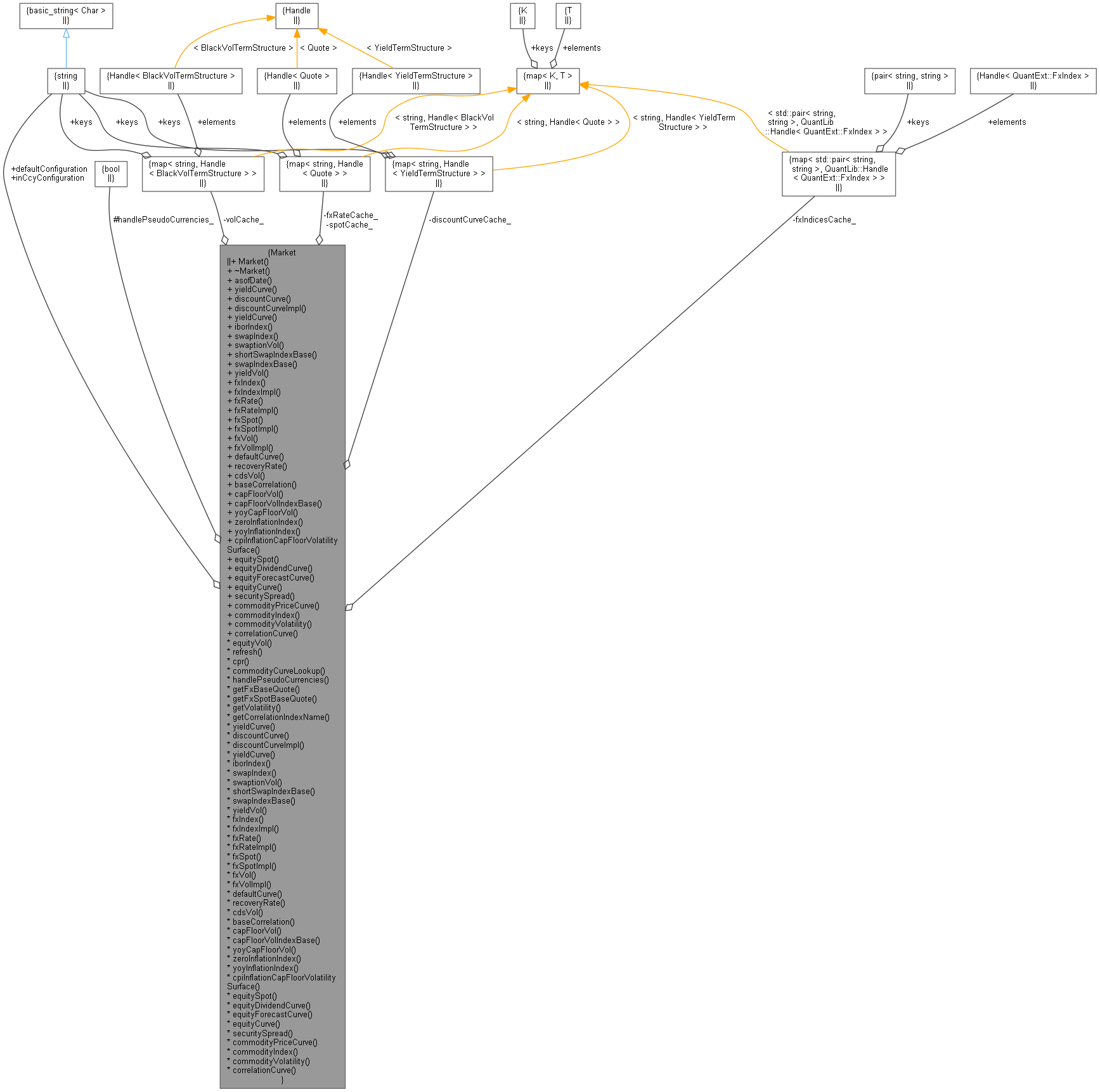

| bool | handlePseudoCurrencies_ = false |

| std::map< string, Handle< Quote > > | spotCache_ |

| std::map< string, Handle< BlackVolTermStructure > > | volCache_ |

| std::map< string, Handle< YieldTermStructure > > | discountCurveCache_ |

| std::map< string, Handle< Quote > > | fxRateCache_ |

| std::map< std::pair< string, string >, QuantLib::Handle< QuantExt::FxIndex > > | fxIndicesCache_ |

| virtual Handle< Quote > | cpr (const string &securityID, const string &configuration=Market::defaultConfiguration) const =0 |

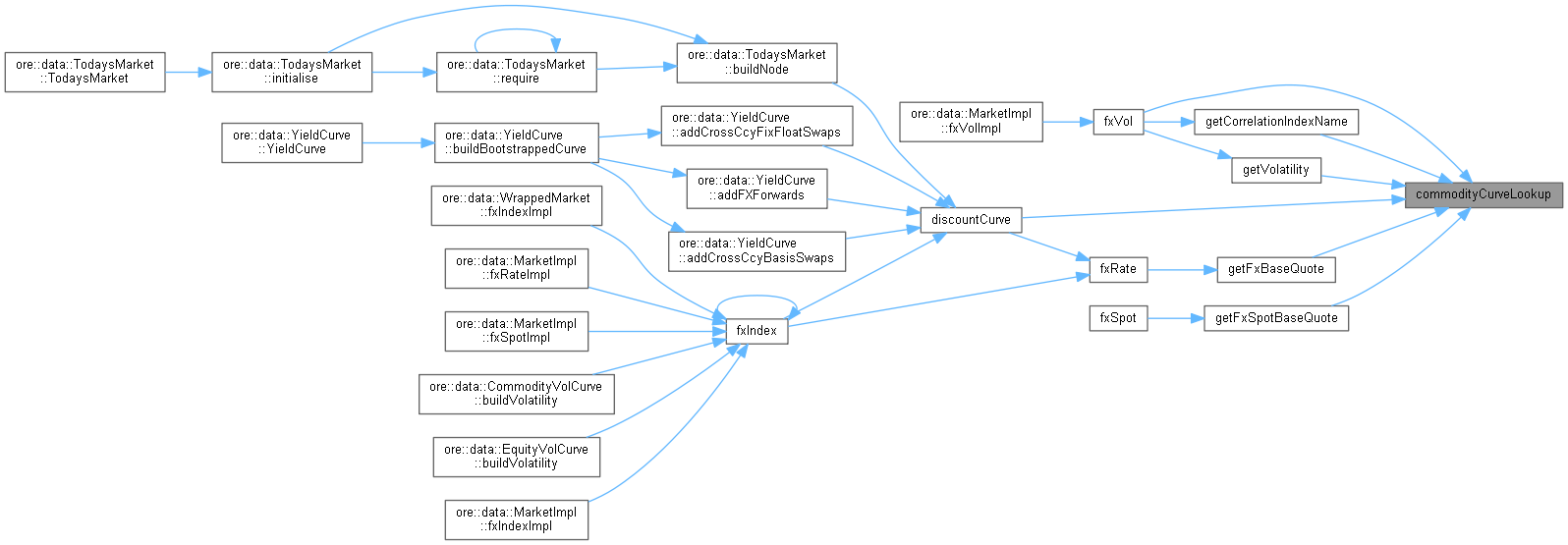

| string | commodityCurveLookup (const string &pm) const |

| bool | handlePseudoCurrencies () const |

| Handle< Quote > | getFxBaseQuote (const string &ccy, const string &config) const |

| Handle< Quote > | getFxSpotBaseQuote (const string &ccy, const string &config) const |

| Handle< BlackVolTermStructure > | getVolatility (const string &ccy, const string &config) const |

| string | getCorrelationIndexName (const string &ccy) const |

Base class for central repositories containing all term structure objects needed in instrument pricing.

Definition at line 163 of file market.hpp.

Constructor.

Definition at line 166 of file market.hpp.

|

virtual |

|

pure virtual |

Get the asof Date.

Implemented in DummyMarket, MarketImpl, and WrappedMarket.

Here is the caller graph for this function:

|

pure virtual |

Implemented in DummyMarket, MarketImpl, and WrappedMarket.

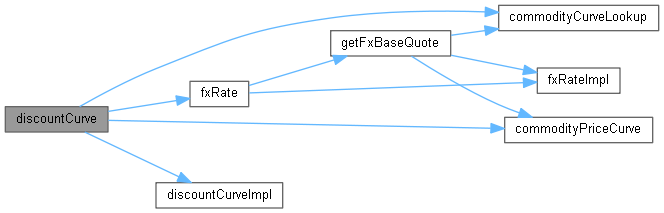

| Handle< YieldTermStructure > discountCurve | ( | const string & | ccy, |

| const string & | configuration = Market::defaultConfiguration |

||

| ) | const |

Definition at line 351 of file market.cpp.

Here is the call graph for this function: Here is the caller graph for this function:

|

pure virtual |

Implemented in MarketImpl, WrappedMarket, and DummyMarket.

Here is the caller graph for this function:

|

pure virtual |

Implemented in DummyMarket, FittedBondCurveHelperMarket, MarketImpl, and WrappedMarket.

|

pure virtual |

Implemented in DummyMarket, MarketImpl, and WrappedMarket.

|

pure virtual |

Implemented in DummyMarket, MarketImpl, and WrappedMarket.

|

pure virtual |

Implemented in DummyMarket, MarketImpl, and WrappedMarket.

|

pure virtual |

Implemented in DummyMarket, WrappedMarket, and MarketImpl.

|

pure virtual |

Implemented in DummyMarket, WrappedMarket, and MarketImpl.

|

pure virtual |

Implemented in DummyMarket, MarketImpl, and WrappedMarket.

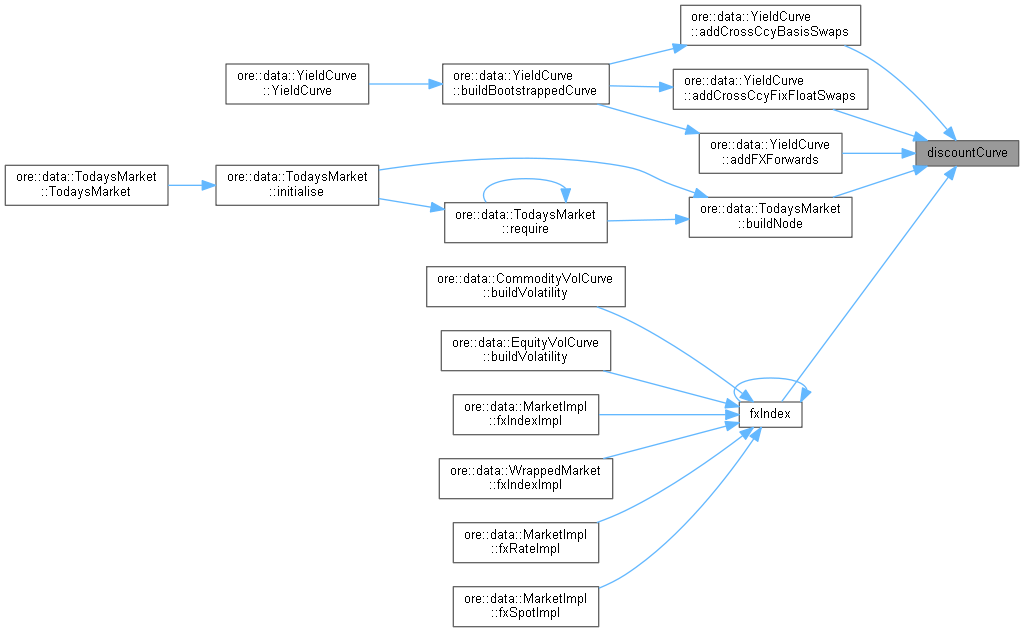

| QuantLib::Handle< QuantExt::FxIndex > fxIndex | ( | const string & | fxIndex, |

| const string & | configuration = Market::defaultConfiguration |

||

| ) | const |

Definition at line 151 of file market.cpp.

Here is the call graph for this function: Here is the caller graph for this function:

|

pure virtual |

Implemented in MarketImpl, WrappedMarket, and DummyMarket.

Here is the caller graph for this function:| Handle< Quote > fxRate | ( | const string & | ccypair, |

| const string & | configuration = Market::defaultConfiguration |

||

| ) | const |

Definition at line 216 of file market.cpp.

Here is the call graph for this function: Here is the caller graph for this function:

|

pure virtual |

Implemented in DummyMarket, MarketImpl, and WrappedMarket.

Here is the caller graph for this function:| Handle< Quote > fxSpot | ( | const string & | ccypair, |

| const string & | configuration = Market::defaultConfiguration |

||

| ) | const |

Definition at line 241 of file market.cpp.

Here is the call graph for this function:

|

pure virtual |

Implemented in DummyMarket, MarketImpl, and WrappedMarket.

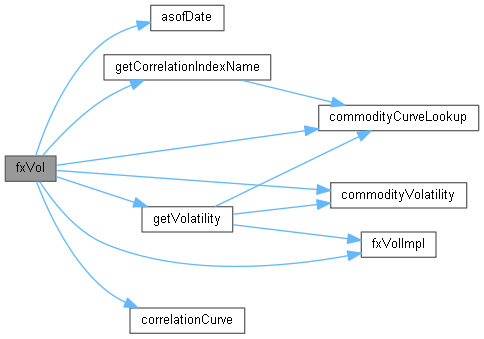

Here is the caller graph for this function:| Handle< BlackVolTermStructure > fxVol | ( | const string & | ccypair, |

| const string & | configuration = Market::defaultConfiguration |

||

| ) | const |

Definition at line 287 of file market.cpp.

Here is the call graph for this function: Here is the caller graph for this function:

|

pure virtual |

Implemented in DummyMarket, MarketImpl, and WrappedMarket.

Here is the caller graph for this function:

|

pure virtual |

Implemented in DummyMarket, FittedBondCurveHelperMarket, MarketImpl, and WrappedMarket.

|

pure virtual |

Implemented in DummyMarket, FittedBondCurveHelperMarket, MarketImpl, and WrappedMarket.

|

pure virtual |

Implemented in DummyMarket, MarketImpl, and WrappedMarket.

|

pure virtual |

Implemented in DummyMarket, MarketImpl, and WrappedMarket.

|

pure virtual |

Implemented in DummyMarket, MarketImpl, and WrappedMarket.

|

pure virtual |

Implemented in DummyMarket, MarketImpl, and WrappedMarket.

|

pure virtual |

Implemented in DummyMarket, WrappedMarket, and MarketImpl.

|

pure virtual |

Inflation Indexes.

Implemented in DummyMarket, MarketImpl, and WrappedMarket.

|

pure virtual |

Implemented in DummyMarket, MarketImpl, and WrappedMarket.

|

pure virtual |

CPI Inflation Cap Floor Volatility Surfaces.

Implemented in DummyMarket, MarketImpl, and WrappedMarket.

|

pure virtual |

Implemented in DummyMarket, MarketImpl, and WrappedMarket.

|

pure virtual |

Implemented in DummyMarket, MarketImpl, and WrappedMarket.

|

pure virtual |

Implemented in DummyMarket, MarketImpl, and WrappedMarket.

|

pure virtual |

Implemented in DummyMarket, MarketImpl, and WrappedMarket.

|

pure virtual |

Implemented in DummyMarket, MarketImpl, and WrappedMarket.

|

virtual |

Refresh term structures for a given configuration.

Reimplemented in MarketImpl, and WrappedMarket.

Definition at line 293 of file market.hpp.

|

pure virtual |

Implemented in DummyMarket, BondSpreadImplyMarket, FittedBondCurveHelperMarket, MarketImpl, and WrappedMarket.

|

pure virtual |

Implemented in DummyMarket, WrappedMarket, and MarketImpl.

Here is the caller graph for this function:

|

pure virtual |

Implemented in DummyMarket, MarketImpl, and WrappedMarket.

|

pure virtual |

Implemented in DummyMarket, WrappedMarket, and MarketImpl.

Here is the caller graph for this function:

|

pure virtual |

Implemented in DummyMarket, WrappedMarket, and MarketImpl.

Here is the caller graph for this function:

|

pure virtual |

Implemented in DummyMarket, MarketImpl, and WrappedMarket.

| string commodityCurveLookup | ( | const string & | pm | ) | const |

Definition at line 112 of file market.cpp.

Here is the caller graph for this function:| bool handlePseudoCurrencies | ( | ) | const |

Definition at line 339 of file market.hpp.

|

private |

Definition at line 120 of file market.cpp.

Here is the call graph for this function: Here is the caller graph for this function:

|

private |

Definition at line 135 of file market.cpp.

Here is the call graph for this function: Here is the caller graph for this function:

|

private |

Definition at line 266 of file market.cpp.

Here is the call graph for this function: Here is the caller graph for this function:

|

private |

Definition at line 275 of file market.cpp.

Here is the call graph for this function: Here is the caller graph for this function:

|

static |

Default configuration label.

Definition at line 296 of file market.hpp.

|

static |

InCcy configuration label.

Definition at line 299 of file market.hpp.

|

protected |

Definition at line 342 of file market.hpp.

|

mutableprivate |

Definition at line 346 of file market.hpp.

|

mutableprivate |

Definition at line 347 of file market.hpp.

|

mutableprivate |

Definition at line 348 of file market.hpp.

|

mutableprivate |

Definition at line 350 of file market.hpp.

|

mutableprivate |

Definition at line 351 of file market.hpp.