Fully annotated reference manual - version 1.8.13.0

Loading...

Searching...

No Matches

Allow for interpretation of how data is stored within cube and AggregationScenarioData. More...

#include <orea/cube/cubeinterpretation.hpp>

Collaboration diagram for CubeInterpretation:

Collaboration diagram for CubeInterpretation:Public Member Functions | |

| CubeInterpretation (const bool storeFlows, const bool withCloseOutLag, const QuantLib::Handle< AggregationScenarioData > &aggregationScenarioData=QuantLib::Handle< AggregationScenarioData >(), const QuantLib::ext::shared_ptr< DateGrid > &dateGrid=nullptr, const Size storeCreditStateNPVs=0, const bool flipViewXVA=false) | |

| bool | storeFlows () const |

| inspectors More... | |

| bool | withCloseOutLag () const |

| const QuantLib::Handle< AggregationScenarioData > & | aggregationScenarioData () const |

| const QuantLib::ext::shared_ptr< DateGrid > & | dateGrid () const |

| Size | storeCreditStateNPVs () const |

| bool | flipViewXVA () const |

| Size | requiredNpvCubeDepth () const |

| npv cube depth that is at least required to work with this interpretation More... | |

| Size | defaultDateNpvIndex () const |

| indices in depth direction, might be Null<Size>() if not applicable More... | |

| Size | closeOutDateNpvIndex () const |

| Size | mporFlowsIndex () const |

| Size | creditStateNPVsIndex () const |

| Real | getGenericValue (const QuantLib::ext::shared_ptr< NPVCube > &cube, Size tradeIdx, Size dateIdx, Size sampleIdx, Size depth) const |

| Retrieve an arbitrary value from the Cube (user needs to know the precise location within depth axis) More... | |

| Real | getDefaultNpv (const QuantLib::ext::shared_ptr< NPVCube > &cube, Size tradeIdx, Size dateIdx, Size sampleIdx) const |

| Retrieve the default date NPV from the Cube. More... | |

| Real | getCloseOutNpv (const QuantLib::ext::shared_ptr< NPVCube > &cube, Size tradeIdx, Size dateIdx, Size sampleIdx) const |

| Retrieve the close-out date NPV from the Cube. More... | |

| Real | getMporPositiveFlows (const QuantLib::ext::shared_ptr< NPVCube > &cube, Size tradeIdx, Size dateIdx, Size sampleIdx) const |

| Retrieve the aggregate value of Margin Period of Risk positive cashflows from the Cube. More... | |

| Real | getMporNegativeFlows (const QuantLib::ext::shared_ptr< NPVCube > &cube, Size tradeIdx, Size dateIdx, Size sampleIdx) const |

| Retrieve the aggregate value of Margin Period of Risk negative cashflows from the Cube. More... | |

| Real | getMporFlows (const QuantLib::ext::shared_ptr< NPVCube > &cube, Size tradeIdx, Size dateIdx, Size sampleIdx) const |

| Retrieve the aggregate value of Margin Period of Risk cashflows from the Cube. More... | |

| Real | getDefaultAggregationScenarioData (const AggregationScenarioDataType &dataType, Size dateIdx, Size sampleIdx, const std::string &qualifier="") const |

| Retrieve a (default date) simulated risk factor value from AggregationScenarioData. More... | |

| Real | getCloseOutAggregationScenarioData (const AggregationScenarioDataType &dataType, Size dateIdx, Size sampleIdx, const std::string &qualifier="") const |

| Retrieve a (default date) simulated risk factor value from AggregationScenarioData. More... | |

| Size | getMporCalendarDays (const QuantLib::ext::shared_ptr< NPVCube > &cube, Size dateIdx) const |

| Number of Calendar Days between a given default date and corresponding close-out date. More... | |

Private Attributes | |

| bool | storeFlows_ |

| bool | withCloseOutLag_ |

| QuantLib::Handle< AggregationScenarioData > | aggregationScenarioData_ |

| QuantLib::ext::shared_ptr< DateGrid > | dateGrid_ |

| Size | storeCreditStateNPVs_ |

| bool | flipViewXVA_ |

| Size | requiredCubeDepth_ |

| Size | defaultDateNpvIndex_ = QuantLib::Null<Size>() |

| Size | closeOutDateNpvIndex_ = QuantLib::Null<Size>() |

| Size | mporFlowsIndex_ = QuantLib::Null<Size>() |

| Size | creditStateNPVsIndex_ = QuantLib::Null<Size>() |

Allow for interpretation of how data is stored within cube and AggregationScenarioData.

Definition at line 44 of file cubeinterpretation.hpp.

| CubeInterpretation | ( | const bool | storeFlows, |

| const bool | withCloseOutLag, | ||

| const QuantLib::Handle< AggregationScenarioData > & | aggregationScenarioData = QuantLib::Handle<AggregationScenarioData>(), |

||

| const QuantLib::ext::shared_ptr< DateGrid > & | dateGrid = nullptr, |

||

| const Size | storeCreditStateNPVs = 0, |

||

| const bool | flipViewXVA = false |

||

| ) |

Definition at line 26 of file cubeinterpretation.cpp.

| bool storeFlows | ( | ) | const |

| bool withCloseOutLag | ( | ) | const |

Definition at line 56 of file cubeinterpretation.cpp.

| const QuantLib::Handle< AggregationScenarioData > & aggregationScenarioData | ( | ) | const |

Definition at line 60 of file cubeinterpretation.cpp.

| const QuantLib::ext::shared_ptr< DateGrid > & dateGrid | ( | ) | const |

Definition at line 64 of file cubeinterpretation.cpp.

| Size storeCreditStateNPVs | ( | ) | const |

Definition at line 58 of file cubeinterpretation.cpp.

| bool flipViewXVA | ( | ) | const |

Definition at line 66 of file cubeinterpretation.cpp.

| Size requiredNpvCubeDepth | ( | ) | const |

npv cube depth that is at least required to work with this interpretation

Definition at line 68 of file cubeinterpretation.cpp.

| Size defaultDateNpvIndex | ( | ) | const |

indices in depth direction, might be Null<Size>() if not applicable

Definition at line 70 of file cubeinterpretation.cpp.

| Size closeOutDateNpvIndex | ( | ) | const |

Definition at line 71 of file cubeinterpretation.cpp.

| Size mporFlowsIndex | ( | ) | const |

Definition at line 72 of file cubeinterpretation.cpp.

| Size creditStateNPVsIndex | ( | ) | const |

Definition at line 73 of file cubeinterpretation.cpp.

| Real getGenericValue | ( | const QuantLib::ext::shared_ptr< NPVCube > & | cube, |

| Size | tradeIdx, | ||

| Size | dateIdx, | ||

| Size | sampleIdx, | ||

| Size | depth | ||

| ) | const |

Retrieve an arbitrary value from the Cube (user needs to know the precise location within depth axis)

Definition at line 75 of file cubeinterpretation.cpp.

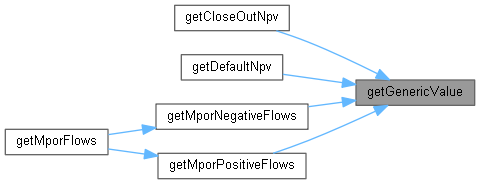

Here is the caller graph for this function:| Real getDefaultNpv | ( | const QuantLib::ext::shared_ptr< NPVCube > & | cube, |

| Size | tradeIdx, | ||

| Size | dateIdx, | ||

| Size | sampleIdx | ||

| ) | const |

Retrieve the default date NPV from the Cube.

Definition at line 84 of file cubeinterpretation.cpp.

Here is the call graph for this function:| Real getCloseOutNpv | ( | const QuantLib::ext::shared_ptr< NPVCube > & | cube, |

| Size | tradeIdx, | ||

| Size | dateIdx, | ||

| Size | sampleIdx | ||

| ) | const |

Retrieve the close-out date NPV from the Cube.

Definition at line 89 of file cubeinterpretation.cpp.

Here is the call graph for this function:| Real getMporPositiveFlows | ( | const QuantLib::ext::shared_ptr< NPVCube > & | cube, |

| Size | tradeIdx, | ||

| Size | dateIdx, | ||

| Size | sampleIdx | ||

| ) | const |

Retrieve the aggregate value of Margin Period of Risk positive cashflows from the Cube.

Definition at line 98 of file cubeinterpretation.cpp.

Here is the call graph for this function: Here is the caller graph for this function:| Real getMporNegativeFlows | ( | const QuantLib::ext::shared_ptr< NPVCube > & | cube, |

| Size | tradeIdx, | ||

| Size | dateIdx, | ||

| Size | sampleIdx | ||

| ) | const |

Retrieve the aggregate value of Margin Period of Risk negative cashflows from the Cube.

Definition at line 112 of file cubeinterpretation.cpp.

Here is the call graph for this function: Here is the caller graph for this function:| Real getMporFlows | ( | const QuantLib::ext::shared_ptr< NPVCube > & | cube, |

| Size | tradeIdx, | ||

| Size | dateIdx, | ||

| Size | sampleIdx | ||

| ) | const |

Retrieve the aggregate value of Margin Period of Risk cashflows from the Cube.

Definition at line 126 of file cubeinterpretation.cpp.

Here is the call graph for this function:| Real getDefaultAggregationScenarioData | ( | const AggregationScenarioDataType & | dataType, |

| Size | dateIdx, | ||

| Size | sampleIdx, | ||

| const std::string & | qualifier = "" |

||

| ) | const |

Retrieve a (default date) simulated risk factor value from AggregationScenarioData.

Definition at line 131 of file cubeinterpretation.cpp.

Here is the caller graph for this function:| Real getCloseOutAggregationScenarioData | ( | const AggregationScenarioDataType & | dataType, |

| Size | dateIdx, | ||

| Size | sampleIdx, | ||

| const std::string & | qualifier = "" |

||

| ) | const |

Retrieve a (default date) simulated risk factor value from AggregationScenarioData.

Definition at line 138 of file cubeinterpretation.cpp.

Here is the call graph for this function: Here is the caller graph for this function:| Size getMporCalendarDays | ( | const QuantLib::ext::shared_ptr< NPVCube > & | cube, |

| Size | dateIdx | ||

| ) | const |

Number of Calendar Days between a given default date and corresponding close-out date.

Definition at line 152 of file cubeinterpretation.cpp.

|

private |

Definition at line 101 of file cubeinterpretation.hpp.

|

private |

Definition at line 102 of file cubeinterpretation.hpp.

|

private |

Definition at line 103 of file cubeinterpretation.hpp.

|

private |

Definition at line 104 of file cubeinterpretation.hpp.

|

private |

Definition at line 105 of file cubeinterpretation.hpp.

|

private |

Definition at line 106 of file cubeinterpretation.hpp.

|

private |

Definition at line 108 of file cubeinterpretation.hpp.

|

private |

Definition at line 109 of file cubeinterpretation.hpp.

|

private |

Definition at line 110 of file cubeinterpretation.hpp.

|

private |

Definition at line 111 of file cubeinterpretation.hpp.

|

private |

Definition at line 112 of file cubeinterpretation.hpp.