Fully annotated reference manual - version 1.8.13.0

Loading...

Searching...

No Matches

Serializable portfolio. More...

#include <ored/portfolio/portfolio.hpp>

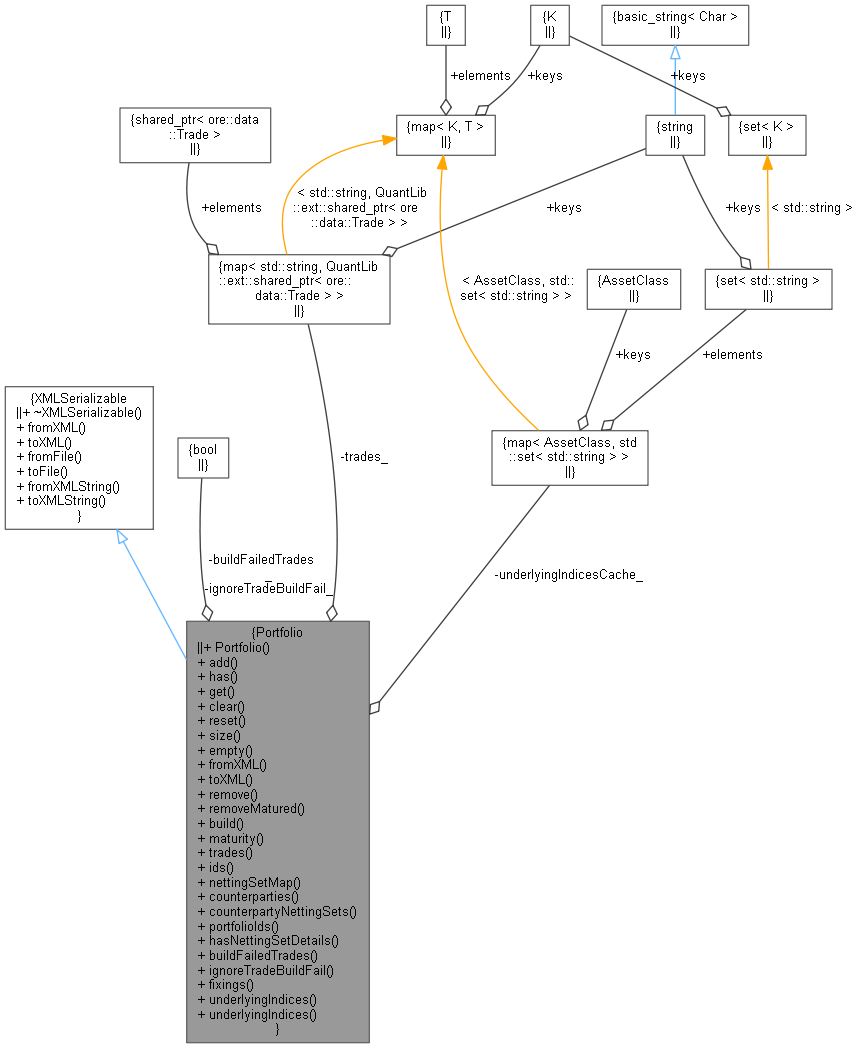

Inheritance diagram for Portfolio: Collaboration diagram for Portfolio:

Inheritance diagram for Portfolio: Collaboration diagram for Portfolio:Public Member Functions | |

| Portfolio (bool buildFailedTrades=true, bool ignoreTradeBuildFail=false) | |

| Default constructor. More... | |

| void | add (const QuantLib::ext::shared_ptr< Trade > &trade) |

| Add a trade to the portfolio. More... | |

| bool | has (const string &id) |

| Check if a trade id is already in the portfolio. More... | |

| QuantLib::ext::shared_ptr< Trade > | get (const std::string &id) const |

| void | clear () |

| Clear the portfolio. More... | |

| void | reset () |

| Reset all trade data. More... | |

| QuantLib::Size | size () const |

| Portfolio size. More... | |

| bool | empty () const |

| void | fromXML (XMLNode *node) override |

| XMLSerializable interface. More... | |

| XMLNode * | toXML (XMLDocument &doc) const override |

| bool | remove (const std::string &tradeID) |

| Remove specified trade from the portfolio. More... | |

| void | removeMatured (const QuantLib::Date &asof) |

| Remove matured trades from portfolio for a given date, each removal is logged with an Alert. More... | |

| void | build (const QuantLib::ext::shared_ptr< EngineFactory > &, const std::string &context="unspecified", const bool emitStructuredError=true) |

| Call build on all trades in the portfolio, the context is included in error messages. More... | |

| QuantLib::Date | maturity () const |

| Calculates the maturity of the portfolio. More... | |

| const std::map< std::string, QuantLib::ext::shared_ptr< Trade > > & | trades () const |

| Return the map tradeId -> trade. More... | |

| std::set< std::string > | ids () const |

| Build a set of tradeIds. More... | |

| std::map< std::string, std::string > | nettingSetMap () const |

| Build a map from trade Ids to NettingSet. More... | |

| std::set< std::string > | counterparties () const |

| Build a set of all counterparties in the portfolio. More... | |

| std::map< std::string, std::set< std::string > > | counterpartyNettingSets () const |

| Build a map from counterparty to NettingSet. More... | |

| std::set< std::string > | portfolioIds () const |

| Compute set of portfolios. More... | |

| bool | hasNettingSetDetails () const |

| Check if at least one trade in the portfolio uses the NettingSetDetails node, and not just NettingSetId. More... | |

| bool | buildFailedTrades () const |

| Does this portfolio build failed trades? More... | |

| bool | ignoreTradeBuildFail () const |

| Keep trade in the portfolio even after build fail. More... | |

| std::map< std::string, RequiredFixings::FixingDates > | fixings (const QuantLib::Date &settlementDate=QuantLib::Date()) const |

| std::map< AssetClass, std::set< std::string > > | underlyingIndices (const QuantLib::ext::shared_ptr< ReferenceDataManager > &referenceDataManager=nullptr) |

| std::set< std::string > | underlyingIndices (AssetClass assetClass, const QuantLib::ext::shared_ptr< ReferenceDataManager > &referenceDataManager=nullptr) |

| Public Member Functions inherited from XMLSerializable | |

| virtual | ~XMLSerializable () |

| virtual void | fromXML (XMLNode *node)=0 |

| virtual XMLNode * | toXML (XMLDocument &doc) const =0 |

| void | fromFile (const std::string &filename) |

| void | toFile (const std::string &filename) const |

| void | fromXMLString (const std::string &xml) |

| Parse from XML string. More... | |

| std::string | toXMLString () const |

| Parse from XML string. More... | |

Private Attributes | |

| bool | buildFailedTrades_ |

| bool | ignoreTradeBuildFail_ |

| std::map< std::string, QuantLib::ext::shared_ptr< Trade > > | trades_ |

| std::map< AssetClass, std::set< std::string > > | underlyingIndicesCache_ |

Serializable portfolio.

Definition at line 43 of file portfolio.hpp.

Default constructor.

Definition at line 46 of file portfolio.hpp.

| void add | ( | const QuantLib::ext::shared_ptr< Trade > & | trade | ) |

Add a trade to the portfolio.

Definition at line 186 of file portfolio.cpp.

Here is the call graph for this function: Here is the caller graph for this function:| bool has | ( | const string & | id | ) |

Check if a trade id is already in the portfolio.

Definition at line 192 of file portfolio.cpp.

Here is the caller graph for this function:| QuantLib::ext::shared_ptr< Trade > get | ( | const std::string & | id | ) | const |

Get a Trade with the given id from the portfolio

nullptr if no trade found with the given id Definition at line 194 of file portfolio.cpp.

Here is the caller graph for this function:| void clear | ( | ) |

Clear the portfolio.

Definition at line 39 of file portfolio.cpp.

Here is the caller graph for this function:| void reset | ( | ) |

| QuantLib::Size size | ( | ) | const |

Portfolio size.

Definition at line 68 of file portfolio.hpp.

Here is the caller graph for this function:| bool empty | ( | ) | const |

Definition at line 70 of file portfolio.hpp.

|

overridevirtual |

XMLSerializable interface.

Implements XMLSerializable.

Definition at line 50 of file portfolio.cpp.

Here is the call graph for this function:

|

overridevirtual |

Implements XMLSerializable.

Definition at line 99 of file portfolio.cpp.

Here is the call graph for this function:| bool remove | ( | const std::string & | tradeID | ) |

Remove specified trade from the portfolio.

Definition at line 106 of file portfolio.cpp.

| void removeMatured | ( | const QuantLib::Date & | asof | ) |

Remove matured trades from portfolio for a given date, each removal is logged with an Alert.

Definition at line 111 of file portfolio.cpp.

Here is the call graph for this function:| void build | ( | const QuantLib::ext::shared_ptr< EngineFactory > & | engineFactory, |

| const std::string & | context = "unspecified", |

||

| const bool | emitStructuredError = true |

||

| ) |

Call build on all trades in the portfolio, the context is included in error messages.

Definition at line 122 of file portfolio.cpp.

Here is the call graph for this function: Here is the caller graph for this function:| Date maturity | ( | ) | const |

Calculates the maturity of the portfolio.

Definition at line 147 of file portfolio.cpp.

| const std::map< std::string, QuantLib::ext::shared_ptr< Trade > > & trades | ( | ) | const |

Return the map tradeId -> trade.

Definition at line 162 of file portfolio.cpp.

Here is the caller graph for this function:| set< string > ids | ( | ) | const |

Build a set of tradeIds.

Definition at line 155 of file portfolio.cpp.

Here is the call graph for this function: Here is the caller graph for this function:| map< string, string > nettingSetMap | ( | ) | const |

Build a map from trade Ids to NettingSet.

Definition at line 164 of file portfolio.cpp.

Here is the call graph for this function: Here is the caller graph for this function:| std::set< std::string > counterparties | ( | ) | const |

Build a set of all counterparties in the portfolio.

Definition at line 171 of file portfolio.cpp.

Here is the call graph for this function: Here is the caller graph for this function:| map< string, set< string > > counterpartyNettingSets | ( | ) | const |

Build a map from counterparty to NettingSet.

Definition at line 178 of file portfolio.cpp.

Here is the call graph for this function:| std::set< std::string > portfolioIds | ( | ) | const |

Compute set of portfolios.

Definition at line 202 of file portfolio.cpp.

Here is the call graph for this function: Here is the caller graph for this function:| bool hasNettingSetDetails | ( | ) | const |

Check if at least one trade in the portfolio uses the NettingSetDetails node, and not just NettingSetId.

Definition at line 210 of file portfolio.cpp.

Here is the call graph for this function: Here is the caller graph for this function:| bool buildFailedTrades | ( | ) | const |

Does this portfolio build failed trades?

Definition at line 111 of file portfolio.hpp.

Here is the caller graph for this function:| bool ignoreTradeBuildFail | ( | ) | const |

Keep trade in the portfolio even after build fail.

Definition at line 114 of file portfolio.hpp.

Here is the caller graph for this function:| map< string, RequiredFixings::FixingDates > fixings | ( | const QuantLib::Date & | settlementDate = QuantLib::Date() | ) | const |

Return the fixings that will be requested in order to price every Trade in this Portfolio given the settlementDate. The map key is the ORE name of the index and the map value is the set of fixing dates.

Definition at line 220 of file portfolio.cpp.

Here is the call graph for this function: Here is the caller graph for this function:| std::map< AssetClass, std::set< std::string > > underlyingIndices | ( | const QuantLib::ext::shared_ptr< ReferenceDataManager > & | referenceDataManager = nullptr | ) |

Returns the names of the underlying instruments for each asset class

Definition at line 234 of file portfolio.cpp.

Here is the call graph for this function: Here is the caller graph for this function:| std::set< std::string > underlyingIndices | ( | AssetClass | assetClass, |

| const QuantLib::ext::shared_ptr< ReferenceDataManager > & | referenceDataManager = nullptr |

||

| ) |

Definition at line 258 of file portfolio.cpp.

Here is the call graph for this function:

|

private |

Definition at line 132 of file portfolio.hpp.

|

private |

Definition at line 132 of file portfolio.hpp.

|

private |

Definition at line 133 of file portfolio.hpp.

|

private |

Definition at line 134 of file portfolio.hpp.