analytic piecewise constant time dependent Heston-model engine More...

#include <analyticptdhestonengine.hpp>

Inheritance diagram for AnalyticPTDHestonEngine:

Inheritance diagram for AnalyticPTDHestonEngine: Collaboration diagram for AnalyticPTDHestonEngine:

Collaboration diagram for AnalyticPTDHestonEngine:

Public Types | |

| enum | ComplexLogFormula { Gatheral , AndersenPiterbarg } |

| typedef AnalyticHestonEngine::Integration | Integration |

| Public Types inherited from Observer | |

| typedef set_type::iterator | iterator |

Public Member Functions | |

| AnalyticPTDHestonEngine (const ext::shared_ptr< PiecewiseTimeDependentHestonModel > &model, Real relTolerance, Size maxEvaluations) | |

| AnalyticPTDHestonEngine (const ext::shared_ptr< PiecewiseTimeDependentHestonModel > &model, Size integrationOrder=144) | |

| AnalyticPTDHestonEngine (const ext::shared_ptr< PiecewiseTimeDependentHestonModel > &model, ComplexLogFormula cpxLog, const Integration &itg, Real andersenPiterbargEpsilon=1e-8) | |

| void | calculate () const override |

| Size | numberOfEvaluations () const |

| std::complex< Real > | chF (const std::complex< Real > &z, Time t) const |

| std::complex< Real > | lnChF (const std::complex< Real > &z, Time t) const |

| Public Member Functions inherited from GenericModelEngine< PiecewiseTimeDependentHestonModel, VanillaOption::arguments, VanillaOption::results > | |

| GenericModelEngine (Handle< PiecewiseTimeDependentHestonModel > model=Handle< PiecewiseTimeDependentHestonModel >()) | |

| GenericModelEngine (const ext::shared_ptr< PiecewiseTimeDependentHestonModel > &model) | |

| Public Member Functions inherited from GenericEngine< ArgumentsType, ResultsType > | |

| PricingEngine::arguments * | getArguments () const override |

| const PricingEngine::results * | getResults () const override |

| void | reset () override |

| void | update () override |

| Public Member Functions inherited from PricingEngine | |

| ~PricingEngine () override=default | |

| virtual arguments * | getArguments () const =0 |

| virtual const results * | getResults () const =0 |

| virtual void | reset ()=0 |

| virtual void | calculate () const =0 |

| Public Member Functions inherited from Observable | |

| Observable ()=default | |

| Observable (const Observable &) | |

| Observable & | operator= (const Observable &) |

| Observable (Observable &&)=delete | |

| Observable & | operator= (Observable &&)=delete |

| virtual | ~Observable ()=default |

| void | notifyObservers () |

| Public Member Functions inherited from Observer | |

| Observer ()=default | |

| Observer (const Observer &) | |

| Observer & | operator= (const Observer &) |

| virtual | ~Observer () |

| std::pair< iterator, bool > | registerWith (const ext::shared_ptr< Observable > &) |

| void | registerWithObservables (const ext::shared_ptr< Observer > &) |

| Size | unregisterWith (const ext::shared_ptr< Observable > &) |

| void | unregisterWithAll () |

| virtual void | update ()=0 |

| virtual void | deepUpdate () |

Private Attributes | |

| Size | evaluations_ |

| const ComplexLogFormula | cpxLog_ |

| const ext::shared_ptr< Integration > | integration_ |

| const Real | andersenPiterbargEpsilon_ |

Additional Inherited Members | |

| Protected Attributes inherited from GenericModelEngine< PiecewiseTimeDependentHestonModel, VanillaOption::arguments, VanillaOption::results > | |

| Handle< PiecewiseTimeDependentHestonModel > | model_ |

| Protected Attributes inherited from GenericEngine< ArgumentsType, ResultsType > | |

| ArgumentsType | arguments_ |

| ResultsType | results_ |

Detailed Description

analytic piecewise constant time dependent Heston-model engine

References:

Heston, Steven L., 1993. A Closed-Form Solution for Options with Stochastic Volatility with Applications to Bond and Currency Options. The review of Financial Studies, Volume 6, Issue 2, 327-343.

J. Gatheral, The Volatility Surface: A Practitioner's Guide, Wiley Finance

A. Elices, Models with time-dependent parameters using transform methods: application to Heston’s model, http://arxiv.org/pdf/0708.2020

Definition at line 52 of file analyticptdhestonengine.hpp.

Member Typedef Documentation

◆ Integration

Definition at line 58 of file analyticptdhestonengine.hpp.

Member Enumeration Documentation

◆ ComplexLogFormula

| enum ComplexLogFormula |

| Enumerator | |

|---|---|

| Gatheral | |

| AndersenPiterbarg | |

Definition at line 57 of file analyticptdhestonengine.hpp.

Constructor & Destructor Documentation

◆ AnalyticPTDHestonEngine() [1/3]

| AnalyticPTDHestonEngine | ( | const ext::shared_ptr< PiecewiseTimeDependentHestonModel > & | model, |

| Real | relTolerance, | ||

| Size | maxEvaluations | ||

| ) |

Definition at line 224 of file analyticptdhestonengine.cpp.

◆ AnalyticPTDHestonEngine() [2/3]

|

explicit |

Definition at line 211 of file analyticptdhestonengine.cpp.

◆ AnalyticPTDHestonEngine() [3/3]

| AnalyticPTDHestonEngine | ( | const ext::shared_ptr< PiecewiseTimeDependentHestonModel > & | model, |

| ComplexLogFormula | cpxLog, | ||

| const Integration & | itg, | ||

| Real | andersenPiterbargEpsilon = 1e-8 |

||

| ) |

Definition at line 237 of file analyticptdhestonengine.cpp.

Member Function Documentation

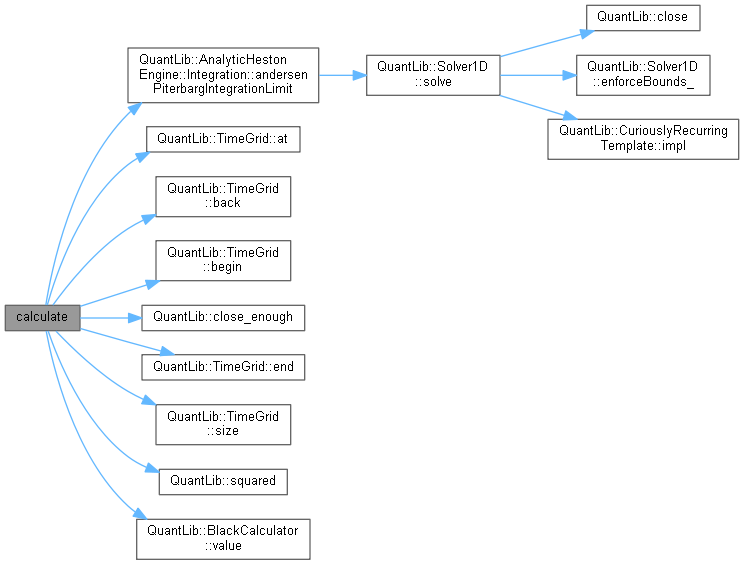

◆ calculate()

|

overridevirtual |

Implements PricingEngine.

Definition at line 252 of file analyticptdhestonengine.cpp.

Here is the call graph for this function:

◆ numberOfEvaluations()

| Size numberOfEvaluations | ( | ) | const |

Definition at line 408 of file analyticptdhestonengine.cpp.

◆ chF()

Definition at line 206 of file analyticptdhestonengine.cpp.

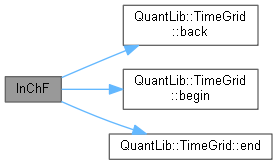

◆ lnChF()

Definition at line 155 of file analyticptdhestonengine.cpp.

Here is the call graph for this function:

Member Data Documentation

◆ evaluations_

|

mutableprivate |

Definition at line 94 of file analyticptdhestonengine.hpp.

◆ cpxLog_

|

private |

Definition at line 95 of file analyticptdhestonengine.hpp.

◆ integration_

|

private |

Definition at line 96 of file analyticptdhestonengine.hpp.

◆ andersenPiterbargEpsilon_

|

private |

Definition at line 97 of file analyticptdhestonengine.hpp.