Forward rate agreement (FRA) class More...

#include <forwardrateagreement.hpp>

Inheritance diagram for ForwardRateAgreement:

Inheritance diagram for ForwardRateAgreement: Collaboration diagram for ForwardRateAgreement:

Collaboration diagram for ForwardRateAgreement:

Public Member Functions | |

| ForwardRateAgreement (const ext::shared_ptr< IborIndex > &index, const Date &valueDate, Position::Type type, Rate strikeForwardRate, Real notionalAmount, Handle< YieldTermStructure > discountCurve={}) | |

| ForwardRateAgreement (const ext::shared_ptr< IborIndex > &index, const Date &valueDate, const Date &maturityDate, Position::Type type, Rate strikeForwardRate, Real notionalAmount, Handle< YieldTermStructure > discountCurve={}) | |

| Public Member Functions inherited from Instrument | |

| Instrument () | |

| Real | NPV () const |

| returns the net present value of the instrument. More... | |

| Real | errorEstimate () const |

| returns the error estimate on the NPV when available. More... | |

| const Date & | valuationDate () const |

| returns the date the net present value refers to. More... | |

| template<typename T > | |

| T | result (const std::string &tag) const |

| returns any additional result returned by the pricing engine. More... | |

| const std::map< std::string, ext::any > & | additionalResults () const |

| returns all additional result returned by the pricing engine. More... | |

| void | setPricingEngine (const ext::shared_ptr< PricingEngine > &) |

| set the pricing engine to be used. More... | |

| virtual void | setupArguments (PricingEngine::arguments *) const |

| virtual void | fetchResults (const PricingEngine::results *) const |

| Public Member Functions inherited from LazyObject | |

| LazyObject () | |

| ~LazyObject () override=default | |

| void | update () override |

| bool | isCalculated () const |

| void | forwardFirstNotificationOnly () |

| void | alwaysForwardNotifications () |

| void | recalculate () |

| void | freeze () |

| void | unfreeze () |

| Public Member Functions inherited from Observable | |

| Observable ()=default | |

| Observable (const Observable &) | |

| Observable & | operator= (const Observable &) |

| Observable (Observable &&)=delete | |

| Observable & | operator= (Observable &&)=delete |

| virtual | ~Observable ()=default |

| void | notifyObservers () |

| Public Member Functions inherited from Observer | |

| Observer ()=default | |

| Observer (const Observer &) | |

| Observer & | operator= (const Observer &) |

| virtual | ~Observer () |

| std::pair< iterator, bool > | registerWith (const ext::shared_ptr< Observable > &) |

| void | registerWithObservables (const ext::shared_ptr< Observer > &) |

| Size | unregisterWith (const ext::shared_ptr< Observable > &) |

| void | unregisterWithAll () |

| virtual void | update ()=0 |

| virtual void | deepUpdate () |

Calculations | |

| Position::Type | fraType_ |

| InterestRate | forwardRate_ |

| aka FRA rate (the market forward rate) More... | |

| InterestRate | strikeForwardRate_ |

| aka FRA fixing rate, contract rate More... | |

| Real | notionalAmount_ |

| ext::shared_ptr< IborIndex > | index_ |

| bool | useIndexedCoupon_ |

| DayCounter | dayCounter_ |

| Calendar | calendar_ |

| BusinessDayConvention | businessDayConvention_ |

| Date | valueDate_ |

| the valueDate is the date the underlying index starts accruing and the FRA is settled. More... | |

| Date | maturityDate_ |

| maturityDate of the underlying index; not the date the FRA is settled. More... | |

| Handle< YieldTermStructure > | discountCurve_ |

| Real | amount_ |

| bool | isExpired () const override |

| A FRA expires/settles on the value date. More... | |

| Real | amount () const |

| The payoff on the value date. More... | |

| const Calendar & | calendar () const |

| BusinessDayConvention | businessDayConvention () const |

| const DayCounter & | dayCounter () const |

| Handle< YieldTermStructure > | discountCurve () const |

| term structure relevant to the contract (e.g. repo curve) More... | |

| Date | fixingDate () const |

| InterestRate | forwardRate () const |

| Returns the relevant forward rate associated with the FRA term. More... | |

| void | setupExpired () const override |

| void | performCalculations () const override |

| void | calculateForwardRate () const |

| void | calculateAmount () const |

Additional Inherited Members | |

| Public Types inherited from Observer | |

| typedef set_type::iterator | iterator |

| Protected Member Functions inherited from Instrument | |

| void | calculate () const override |

| Protected Member Functions inherited from LazyObject | |

| Protected Attributes inherited from Instrument | |

| Real | NPV_ |

| Real | errorEstimate_ |

| Date | valuationDate_ |

| std::map< std::string, ext::any > | additionalResults_ |

| ext::shared_ptr< PricingEngine > | engine_ |

| Protected Attributes inherited from LazyObject | |

| bool | calculated_ = false |

| bool | frozen_ = false |

| bool | alwaysForward_ |

Detailed Description

Forward rate agreement (FRA) class

- Unlike the forward contract conventions on carryable financial assets (stocks, bonds, commodities), the valueDate for a FRA is taken to be the day when the forward loan or deposit begins and when full settlement takes place (based on the NPV of the contract on that date). maturityDate is the date when the forward loan or deposit ends. In fact, the FRA settles and expires on the valueDate, not on the (later) maturityDate. It follows that (maturityDate - valueDate) is the tenor/term of the underlying loan or deposit

- Choose position type = Long for an "FRA purchase" (future long loan, short deposit [borrower])

- Choose position type = Short for an "FRA sale" (future short loan, long deposit [lender])

Example: valuation of a forward-rate agreement

- Warning:

- This class still needs to be rigorously tested

- Examples

- FRA.cpp.

Definition at line 66 of file forwardrateagreement.hpp.

Constructor & Destructor Documentation

◆ ForwardRateAgreement() [1/2]

| ForwardRateAgreement | ( | const ext::shared_ptr< IborIndex > & | index, |

| const Date & | valueDate, | ||

| Position::Type | type, | ||

| Rate | strikeForwardRate, | ||

| Real | notionalAmount, | ||

| Handle< YieldTermStructure > | discountCurve = {} |

||

| ) |

When using this constructor, the forward rate will be forecast by the passed index. This corresponds to useIndexedCoupon=true in the FraRateHelper class.

Definition at line 28 of file forwardrateagreement.cpp.

◆ ForwardRateAgreement() [2/2]

| ForwardRateAgreement | ( | const ext::shared_ptr< IborIndex > & | index, |

| const Date & | valueDate, | ||

| const Date & | maturityDate, | ||

| Position::Type | type, | ||

| Rate | strikeForwardRate, | ||

| Real | notionalAmount, | ||

| Handle< YieldTermStructure > | discountCurve = {} |

||

| ) |

When using this constructor, a par-rate approximation will be used, i.e., the forward rate will be forecast from value date to maturity date by the forecast curve contained in the index. This corresponds to useIndexedCoupon=false in the FraRateHelper class.

Definition at line 39 of file forwardrateagreement.cpp.

Here is the call graph for this function:

Member Function Documentation

◆ isExpired()

|

overridevirtual |

A FRA expires/settles on the value date.

Implements Instrument.

Definition at line 70 of file forwardrateagreement.cpp.

Here is the call graph for this function:

◆ amount()

| Real amount | ( | ) | const |

The payoff on the value date.

- Examples

- FRA.cpp.

Definition at line 74 of file forwardrateagreement.cpp.

Here is the call graph for this function:

◆ calendar()

| const Calendar & calendar | ( | ) | const |

Definition at line 142 of file forwardrateagreement.hpp.

◆ businessDayConvention()

| BusinessDayConvention businessDayConvention | ( | ) | const |

Definition at line 144 of file forwardrateagreement.hpp.

◆ dayCounter()

| const DayCounter & dayCounter | ( | ) | const |

Definition at line 148 of file forwardrateagreement.hpp.

◆ discountCurve()

| Handle< YieldTermStructure > discountCurve | ( | ) | const |

term structure relevant to the contract (e.g. repo curve)

Definition at line 150 of file forwardrateagreement.hpp.

◆ fixingDate()

| Date fixingDate | ( | ) | const |

◆ forwardRate()

| InterestRate forwardRate | ( | ) | const |

Returns the relevant forward rate associated with the FRA term.

- Examples

- FRA.cpp.

Definition at line 79 of file forwardrateagreement.cpp.

Here is the call graph for this function:

◆ setupExpired()

|

overrideprotectedvirtual |

This method must leave the instrument in a consistent state when the expiration condition is met.

Reimplemented from Instrument.

Definition at line 84 of file forwardrateagreement.cpp.

Here is the call graph for this function:

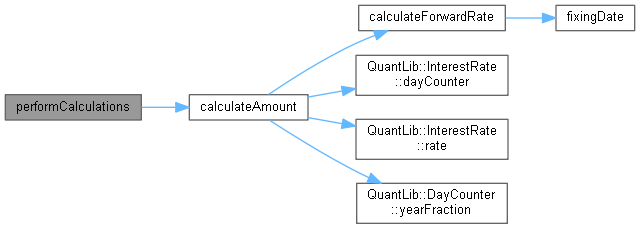

◆ performCalculations()

|

overrideprotectedvirtual |

In case a pricing engine is not used, this method must be overridden to perform the actual calculations and set any needed results. In case a pricing engine is used, the default implementation can be used.

Reimplemented from Instrument.

Definition at line 89 of file forwardrateagreement.cpp.

Here is the call graph for this function:

◆ calculateForwardRate()

|

private |

Definition at line 96 of file forwardrateagreement.cpp.

Here is the call graph for this function: Here is the caller graph for this function:

Here is the caller graph for this function:

◆ calculateAmount()

|

private |

Definition at line 110 of file forwardrateagreement.cpp.

Here is the call graph for this function: Here is the caller graph for this function:

Here is the caller graph for this function:

Member Data Documentation

◆ fraType_

|

protected |

Definition at line 117 of file forwardrateagreement.hpp.

◆ forwardRate_

|

mutableprotected |

aka FRA rate (the market forward rate)

Definition at line 119 of file forwardrateagreement.hpp.

◆ strikeForwardRate_

|

protected |

aka FRA fixing rate, contract rate

Definition at line 121 of file forwardrateagreement.hpp.

◆ notionalAmount_

|

protected |

Definition at line 122 of file forwardrateagreement.hpp.

◆ index_

|

protected |

Definition at line 123 of file forwardrateagreement.hpp.

◆ useIndexedCoupon_

|

protected |

Definition at line 124 of file forwardrateagreement.hpp.

◆ dayCounter_

|

protected |

Definition at line 126 of file forwardrateagreement.hpp.

◆ calendar_

|

protected |

Definition at line 127 of file forwardrateagreement.hpp.

◆ businessDayConvention_

|

protected |

Definition at line 128 of file forwardrateagreement.hpp.

◆ valueDate_

|

protected |

the valueDate is the date the underlying index starts accruing and the FRA is settled.

Definition at line 131 of file forwardrateagreement.hpp.

◆ maturityDate_

|

protected |

maturityDate of the underlying index; not the date the FRA is settled.

Definition at line 133 of file forwardrateagreement.hpp.

◆ discountCurve_

|

protected |

Definition at line 134 of file forwardrateagreement.hpp.

◆ amount_

|

mutableprivate |

Definition at line 139 of file forwardrateagreement.hpp.