Base YoY inflation cap/floor engine. More...

#include <inflationcapfloorengines.hpp>

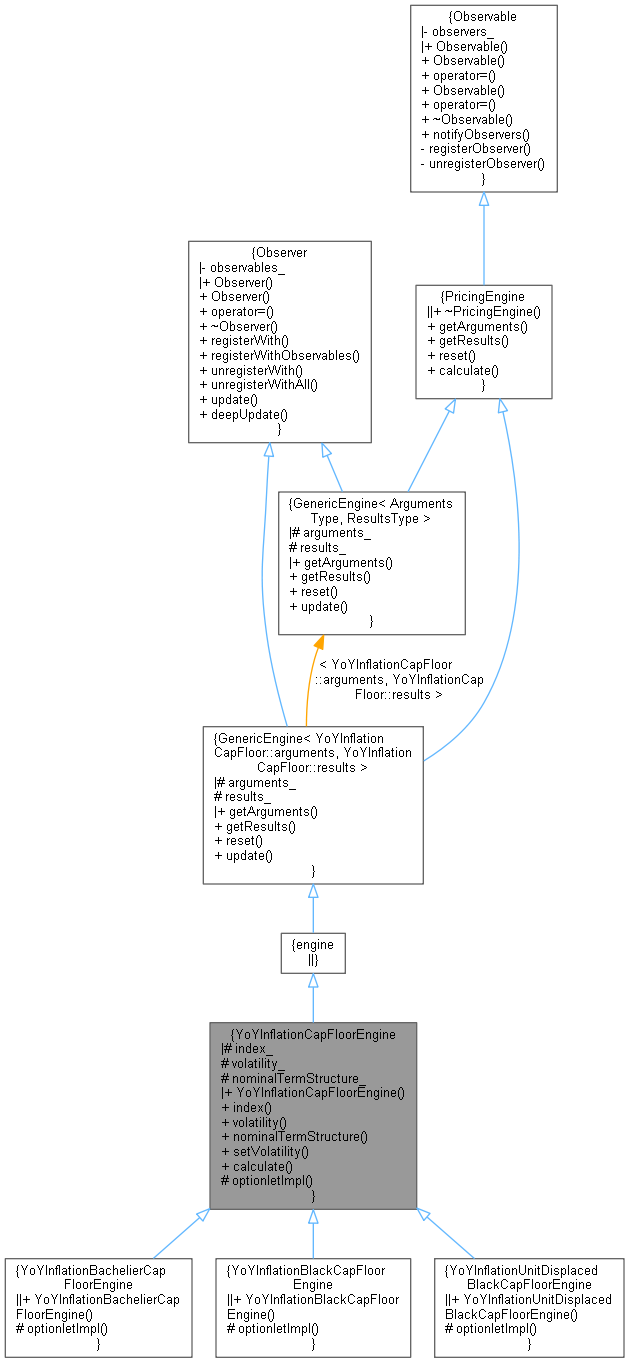

Inheritance diagram for YoYInflationCapFloorEngine:

Inheritance diagram for YoYInflationCapFloorEngine: Collaboration diagram for YoYInflationCapFloorEngine:

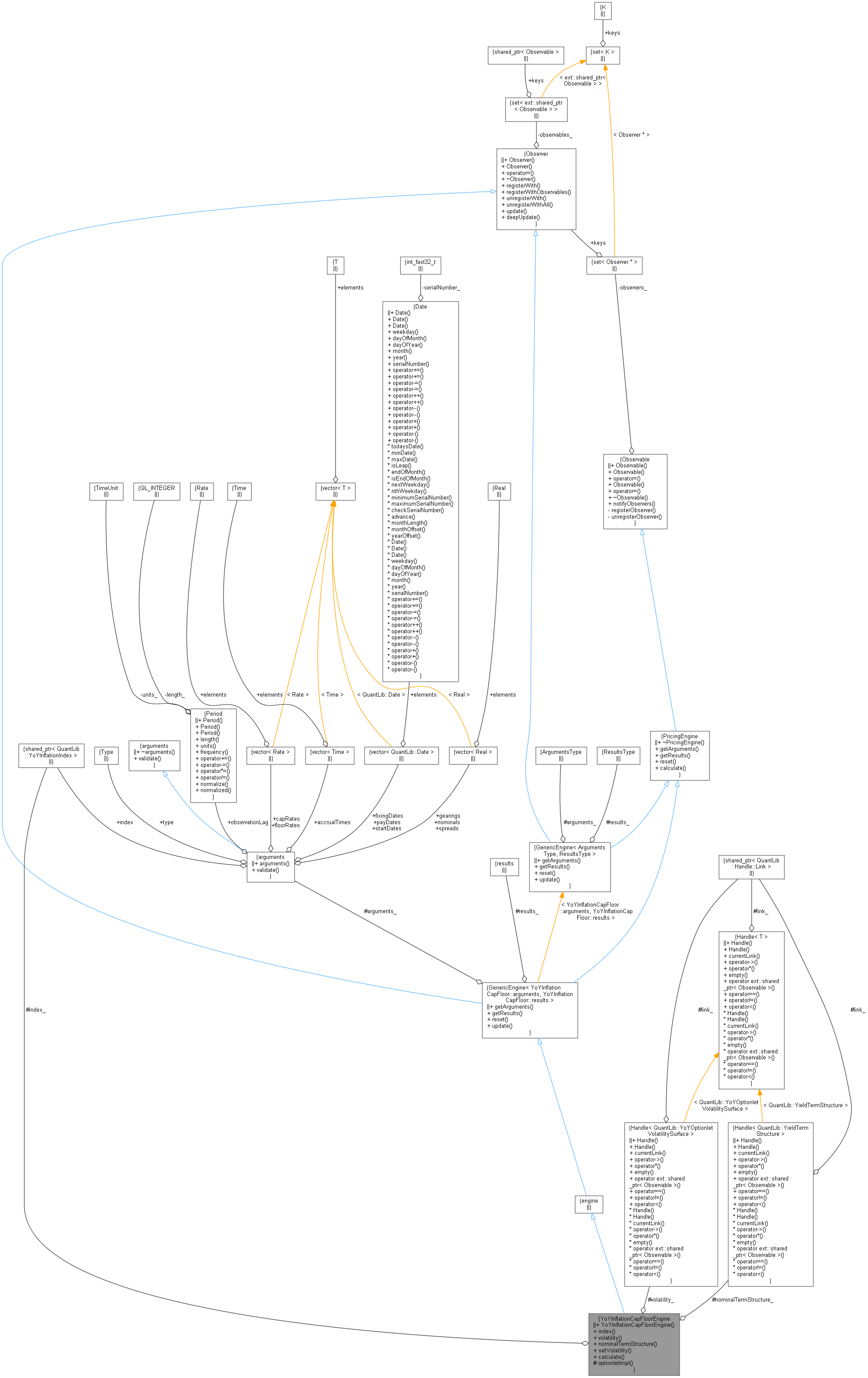

Collaboration diagram for YoYInflationCapFloorEngine:

Protected Member Functions | |

| virtual Real | optionletImpl (Option::Type type, Rate strike, Rate forward, Real stdDev, Real d) const =0 |

| descendents only need to implement this More... | |

Protected Attributes | |

| ext::shared_ptr< YoYInflationIndex > | index_ |

| Handle< YoYOptionletVolatilitySurface > | volatility_ |

| Handle< YieldTermStructure > | nominalTermStructure_ |

| Protected Attributes inherited from GenericEngine< YoYInflationCapFloor::arguments, YoYInflationCapFloor::results > | |

| YoYInflationCapFloor::arguments | arguments_ |

| YoYInflationCapFloor::results | results_ |

Additional Inherited Members | |

| Public Types inherited from Observer | |

| typedef set_type::iterator | iterator |

Detailed Description

Base YoY inflation cap/floor engine.

This class doesn't know yet what sort of vol it is. The inflation index must be linked to a yoy inflation term structure.

Definition at line 44 of file inflationcapfloorengines.hpp.

Constructor & Destructor Documentation

◆ YoYInflationCapFloorEngine()

| YoYInflationCapFloorEngine | ( | ext::shared_ptr< YoYInflationIndex > | index, |

| Handle< YoYOptionletVolatilitySurface > | vol, | ||

| Handle< YieldTermStructure > | nominalTermStructure | ||

| ) |

Definition at line 29 of file inflationcapfloorengines.cpp.

Here is the call graph for this function:

Member Function Documentation

◆ index()

| ext::shared_ptr< YoYInflationIndex > index | ( | ) | const |

Definition at line 50 of file inflationcapfloorengines.hpp.

Here is the caller graph for this function:

◆ volatility()

| Handle< YoYOptionletVolatilitySurface > volatility | ( | ) | const |

Definition at line 51 of file inflationcapfloorengines.hpp.

◆ nominalTermStructure()

| Handle< YieldTermStructure > nominalTermStructure | ( | ) | const |

Definition at line 52 of file inflationcapfloorengines.hpp.

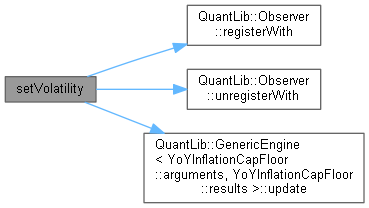

◆ setVolatility()

| void setVolatility | ( | const Handle< YoYOptionletVolatilitySurface > & | vol | ) |

Definition at line 41 of file inflationcapfloorengines.cpp.

Here is the call graph for this function:

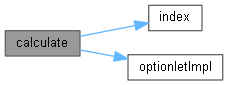

◆ calculate()

|

overridevirtual |

Implements PricingEngine.

Definition at line 51 of file inflationcapfloorengines.cpp.

Here is the call graph for this function:

◆ optionletImpl()

|

protectedpure virtual |

descendents only need to implement this

Implemented in YoYInflationBlackCapFloorEngine, YoYInflationUnitDisplacedBlackCapFloorEngine, and YoYInflationBachelierCapFloorEngine.

Here is the caller graph for this function:

Member Data Documentation

◆ index_

|

protected |

Definition at line 64 of file inflationcapfloorengines.hpp.

◆ volatility_

|

protected |

Definition at line 65 of file inflationcapfloorengines.hpp.

◆ nominalTermStructure_

|

protected |

Definition at line 66 of file inflationcapfloorengines.hpp.