Unit Displaced Black-formula inflation cap/floor engine (standalone, i.e. no coupon pricer) More...

#include <ql/pricingengines/inflation/inflationcapfloorengines.hpp>

Inheritance diagram for YoYInflationBachelierCapFloorEngine:

Inheritance diagram for YoYInflationBachelierCapFloorEngine: Collaboration diagram for YoYInflationBachelierCapFloorEngine:

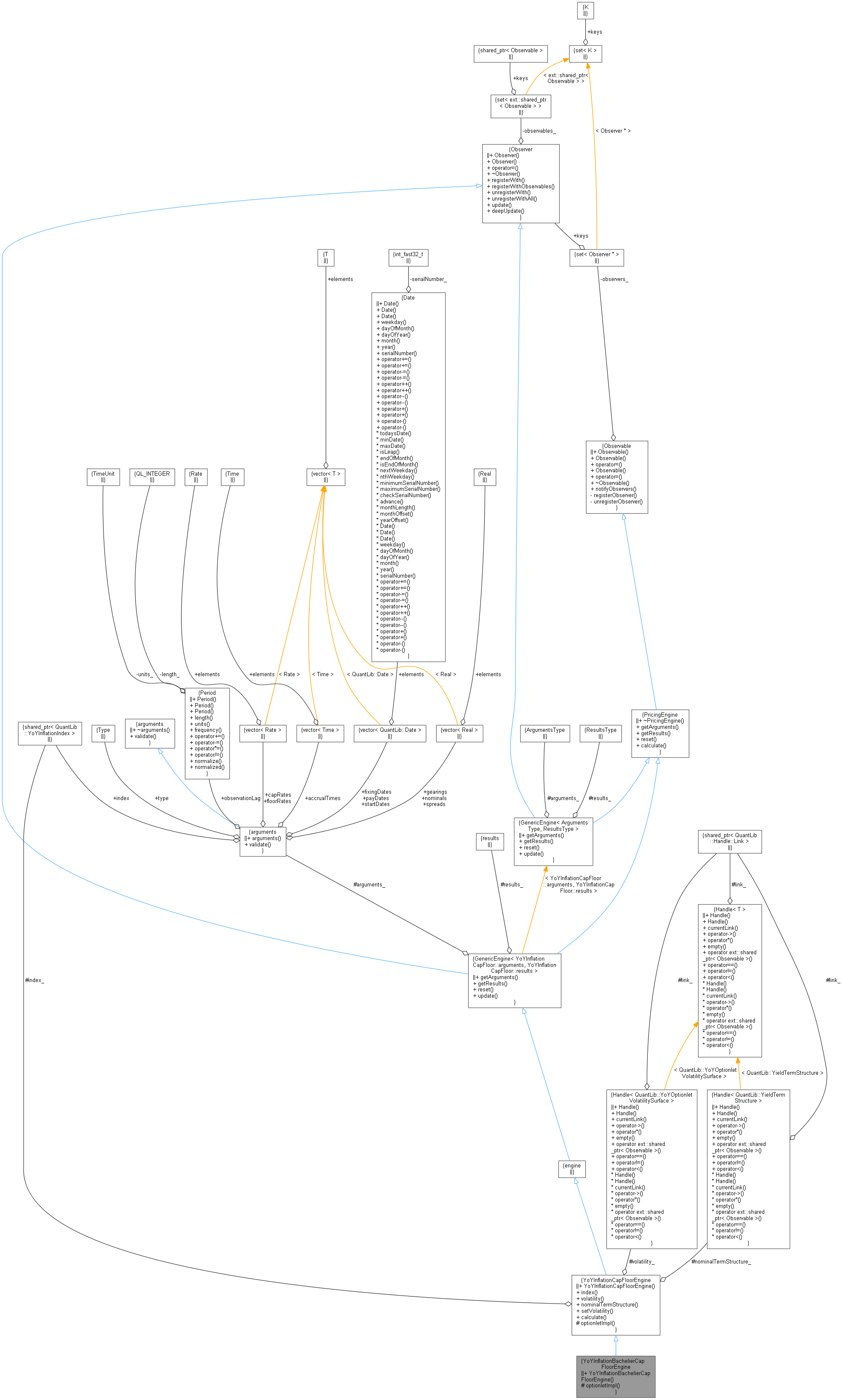

Collaboration diagram for YoYInflationBachelierCapFloorEngine:

Protected Member Functions | |

| Real | optionletImpl (Option::Type, Real strike, Real forward, Real stdDev, Real d) const override |

| descendents only need to implement this More... | |

| virtual Real | optionletImpl (Option::Type type, Rate strike, Rate forward, Real stdDev, Real d) const =0 |

| descendents only need to implement this More... | |

Additional Inherited Members | |

| Public Types inherited from Observer | |

| typedef set_type::iterator | iterator |

| Protected Attributes inherited from YoYInflationCapFloorEngine | |

| ext::shared_ptr< YoYInflationIndex > | index_ |

| Handle< YoYOptionletVolatilitySurface > | volatility_ |

| Handle< YieldTermStructure > | nominalTermStructure_ |

| Protected Attributes inherited from GenericEngine< YoYInflationCapFloor::arguments, YoYInflationCapFloor::results > | |

| YoYInflationCapFloor::arguments | arguments_ |

| YoYInflationCapFloor::results | results_ |

Detailed Description

Unit Displaced Black-formula inflation cap/floor engine (standalone, i.e. no coupon pricer)

Definition at line 99 of file inflationcapfloorengines.hpp.

Constructor & Destructor Documentation

◆ YoYInflationBachelierCapFloorEngine()

| YoYInflationBachelierCapFloorEngine | ( | const ext::shared_ptr< YoYInflationIndex > & | index, |

| const Handle< YoYOptionletVolatilitySurface > & | vol, | ||

| const Handle< YieldTermStructure > & | nominalTermStructure | ||

| ) |

Definition at line 171 of file inflationcapfloorengines.cpp.

Member Function Documentation

◆ optionletImpl()

|

overrideprotectedvirtual |

descendents only need to implement this

Implements YoYInflationCapFloorEngine.

Definition at line 178 of file inflationcapfloorengines.cpp.

Here is the call graph for this function: