Base class for yoy inflation cap-like instruments. More...

#include <inflationcapfloor.hpp>

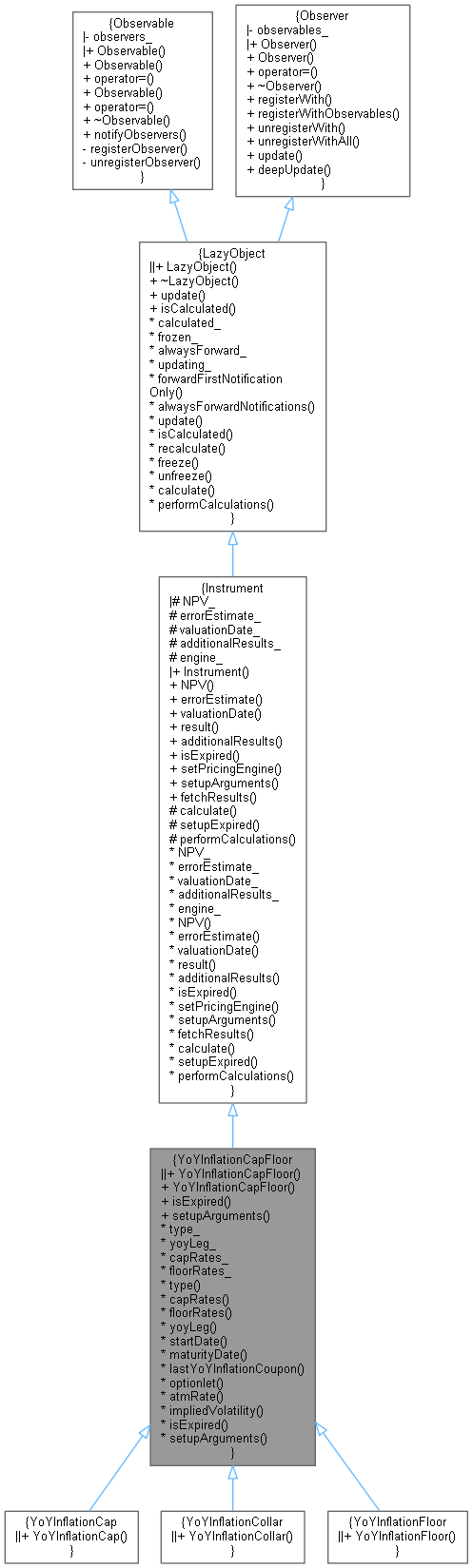

Inheritance diagram for YoYInflationCapFloor:

Inheritance diagram for YoYInflationCapFloor: Collaboration diagram for YoYInflationCapFloor:

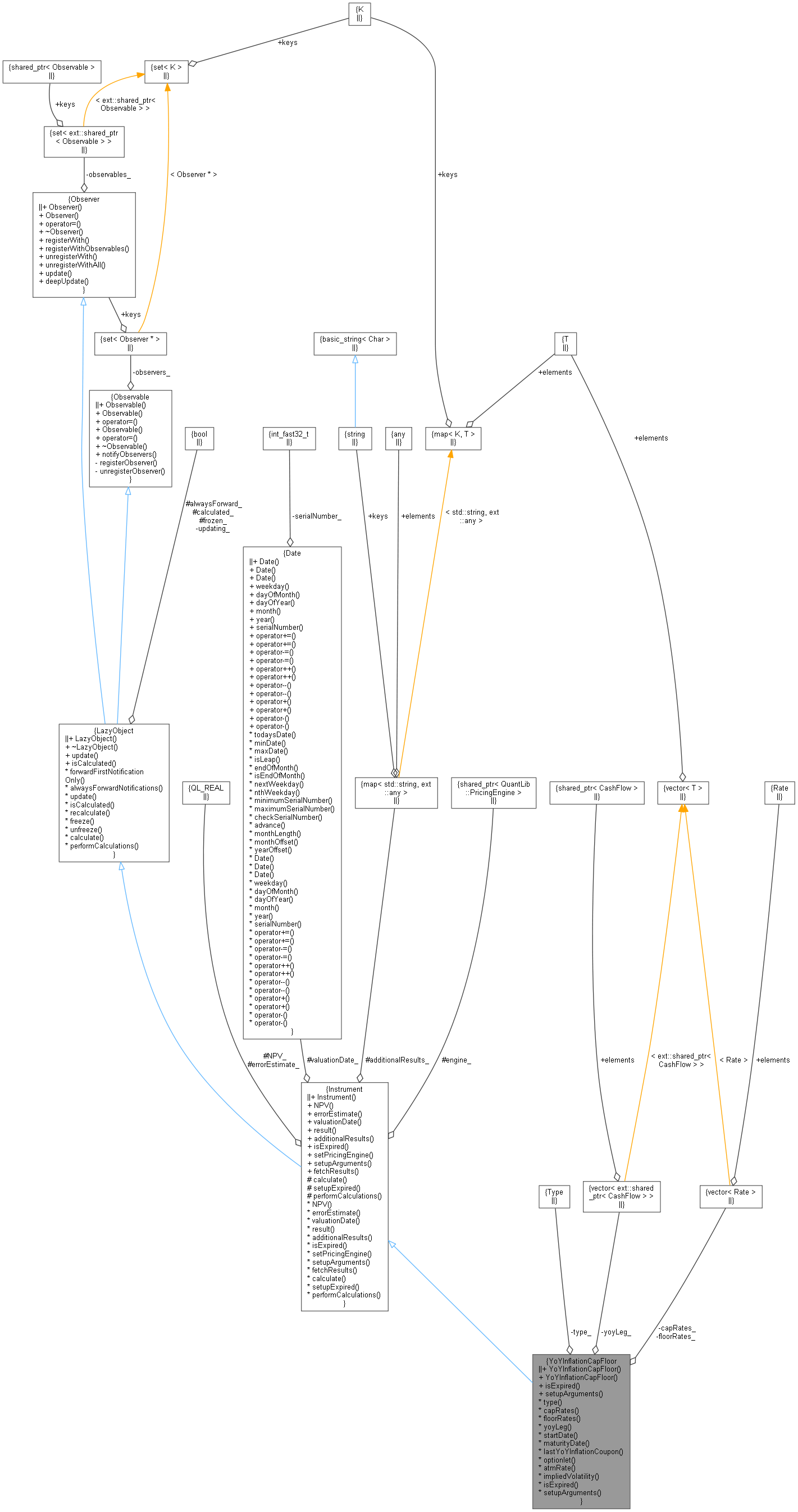

Collaboration diagram for YoYInflationCapFloor:

Classes | |

| class | arguments |

| Arguments for YoY Inflation cap/floor calculation More... | |

| class | engine |

| base class for cap/floor engines More... | |

Public Types | |

| enum | Type { Cap , Floor , Collar } |

| Public Types inherited from Observer | |

| typedef set_type::iterator | iterator |

Public Member Functions | |

| YoYInflationCapFloor (Type type, Leg yoyLeg, std::vector< Rate > capRates, std::vector< Rate > floorRates) | |

| YoYInflationCapFloor (Type type, Leg yoyLeg, const std::vector< Rate > &strikes) | |

Instrument interface | |

| bool | isExpired () const override |

| returns whether the instrument might have value greater than zero. More... | |

| void | setupArguments (PricingEngine::arguments *) const override |

| Public Member Functions inherited from Instrument | |

| Instrument () | |

| Real | NPV () const |

| returns the net present value of the instrument. More... | |

| Real | errorEstimate () const |

| returns the error estimate on the NPV when available. More... | |

| const Date & | valuationDate () const |

| returns the date the net present value refers to. More... | |

| template<typename T > | |

| T | result (const std::string &tag) const |

| returns any additional result returned by the pricing engine. More... | |

| const std::map< std::string, ext::any > & | additionalResults () const |

| returns all additional result returned by the pricing engine. More... | |

| void | setPricingEngine (const ext::shared_ptr< PricingEngine > &) |

| set the pricing engine to be used. More... | |

| virtual void | fetchResults (const PricingEngine::results *) const |

| Public Member Functions inherited from LazyObject | |

| LazyObject () | |

| ~LazyObject () override=default | |

| void | update () override |

| bool | isCalculated () const |

| void | forwardFirstNotificationOnly () |

| void | alwaysForwardNotifications () |

| void | recalculate () |

| void | freeze () |

| void | unfreeze () |

| Public Member Functions inherited from Observable | |

| Observable ()=default | |

| Observable (const Observable &) | |

| Observable & | operator= (const Observable &) |

| Observable (Observable &&)=delete | |

| Observable & | operator= (Observable &&)=delete |

| virtual | ~Observable ()=default |

| void | notifyObservers () |

| Public Member Functions inherited from Observer | |

| Observer ()=default | |

| Observer (const Observer &) | |

| Observer & | operator= (const Observer &) |

| virtual | ~Observer () |

| std::pair< iterator, bool > | registerWith (const ext::shared_ptr< Observable > &) |

| void | registerWithObservables (const ext::shared_ptr< Observer > &) |

| Size | unregisterWith (const ext::shared_ptr< Observable > &) |

| void | unregisterWithAll () |

| virtual void | update ()=0 |

| virtual void | deepUpdate () |

Inspectors | |

| Type | type_ |

| Leg | yoyLeg_ |

| std::vector< Rate > | capRates_ |

| std::vector< Rate > | floorRates_ |

| Type | type () const |

| const std::vector< Rate > & | capRates () const |

| const std::vector< Rate > & | floorRates () const |

| const Leg & | yoyLeg () const |

| Date | startDate () const |

| Date | maturityDate () const |

| ext::shared_ptr< YoYInflationCoupon > | lastYoYInflationCoupon () const |

| ext::shared_ptr< YoYInflationCapFloor > | optionlet (Size n) const |

| Returns the n-th optionlet as a cap/floor with only one cash flow. More... | |

| virtual Rate | atmRate (const YieldTermStructure &discountCurve) const |

| virtual Volatility | impliedVolatility (Real price, const Handle< YoYInflationTermStructure > &yoyCurve, Volatility guess, Real accuracy=1.0e-4, Natural maxEvaluations=100, Volatility minVol=1.0e-7, Volatility maxVol=4.0) const |

| implied term volatility More... | |

Additional Inherited Members | |

| Protected Member Functions inherited from Instrument | |

| void | calculate () const override |

| virtual void | setupExpired () const |

| void | performCalculations () const override |

| Protected Member Functions inherited from LazyObject | |

| Protected Attributes inherited from Instrument | |

| Real | NPV_ |

| Real | errorEstimate_ |

| Date | valuationDate_ |

| std::map< std::string, ext::any > | additionalResults_ |

| ext::shared_ptr< PricingEngine > | engine_ |

| Protected Attributes inherited from LazyObject | |

| bool | calculated_ = false |

| bool | frozen_ = false |

| bool | alwaysForward_ |

Detailed Description

Base class for yoy inflation cap-like instruments.

Note that the standard YoY inflation cap/floor defined here is different from nominal, because in nominal world standard cap/floors do not have the first optionlet. This is because they set in advance so there is no point. However, yoy inflation generally sets (effectively) in arrears, (actually in arrears vs lag of a few months) thus the first optionlet is relevant. Hence we can do a parity test without a special definition of the YoY cap/floor instrument.

- Tests:

- the relationship between the values of caps, floors and the resulting collars is checked.

- the put-call parity between the values of caps, floors and swaps is checked.

- the correctness of the returned value is tested by checking it against a known good value.

Definition at line 55 of file inflationcapfloor.hpp.

Member Enumeration Documentation

◆ Type

| enum Type |

| Enumerator | |

|---|---|

| Cap | |

| Floor | |

| Collar | |

Definition at line 57 of file inflationcapfloor.hpp.

Constructor & Destructor Documentation

◆ YoYInflationCapFloor() [1/2]

| YoYInflationCapFloor | ( | YoYInflationCapFloor::Type | type, |

| Leg | yoyLeg, | ||

| std::vector< Rate > | capRates, | ||

| std::vector< Rate > | floorRates | ||

| ) |

◆ YoYInflationCapFloor() [2/2]

| YoYInflationCapFloor | ( | YoYInflationCapFloor::Type | type, |

| Leg | yoyLeg, | ||

| const std::vector< Rate > & | strikes | ||

| ) |

Member Function Documentation

◆ isExpired()

|

overridevirtual |

returns whether the instrument might have value greater than zero.

Implements Instrument.

Definition at line 94 of file inflationcapfloor.cpp.

◆ setupArguments()

|

overridevirtual |

When a derived argument structure is defined for an instrument, this method should be overridden to fill it. This is mandatory in case a pricing engine is used.

Reimplemented from Instrument.

Definition at line 133 of file inflationcapfloor.cpp.

◆ type()

| Type type | ( | ) | const |

◆ capRates()

| const std::vector< Rate > & capRates | ( | ) | const |

◆ floorRates()

| const std::vector< Rate > & floorRates | ( | ) | const |

◆ yoyLeg()

| const Leg & yoyLeg | ( | ) | const |

◆ startDate()

| Date startDate | ( | ) | const |

◆ maturityDate()

| Date maturityDate | ( | ) | const |

◆ lastYoYInflationCoupon()

| ext::shared_ptr< YoYInflationCoupon > lastYoYInflationCoupon | ( | ) | const |

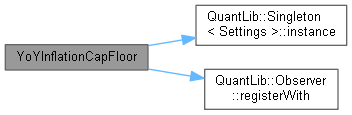

Definition at line 110 of file inflationcapfloor.cpp.

Here is the call graph for this function: Here is the caller graph for this function:

Here is the caller graph for this function:

◆ optionlet()

| ext::shared_ptr< YoYInflationCapFloor > optionlet | ( | Size | n | ) | const |

Returns the n-th optionlet as a cap/floor with only one cash flow.

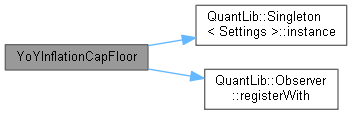

Definition at line 117 of file inflationcapfloor.cpp.

Here is the call graph for this function:

◆ atmRate()

|

virtual |

◆ impliedVolatility()

|

virtual |

implied term volatility

Definition at line 161 of file inflationcapfloor.hpp.

Member Data Documentation

◆ type_

|

private |

Definition at line 94 of file inflationcapfloor.hpp.

◆ yoyLeg_

|

private |

Definition at line 95 of file inflationcapfloor.hpp.

◆ capRates_

|

private |

Definition at line 96 of file inflationcapfloor.hpp.

◆ floorRates_

|

private |

Definition at line 97 of file inflationcapfloor.hpp.