Forward contract on a bond More...

#include <bondforward.hpp>

Inheritance diagram for BondForward:

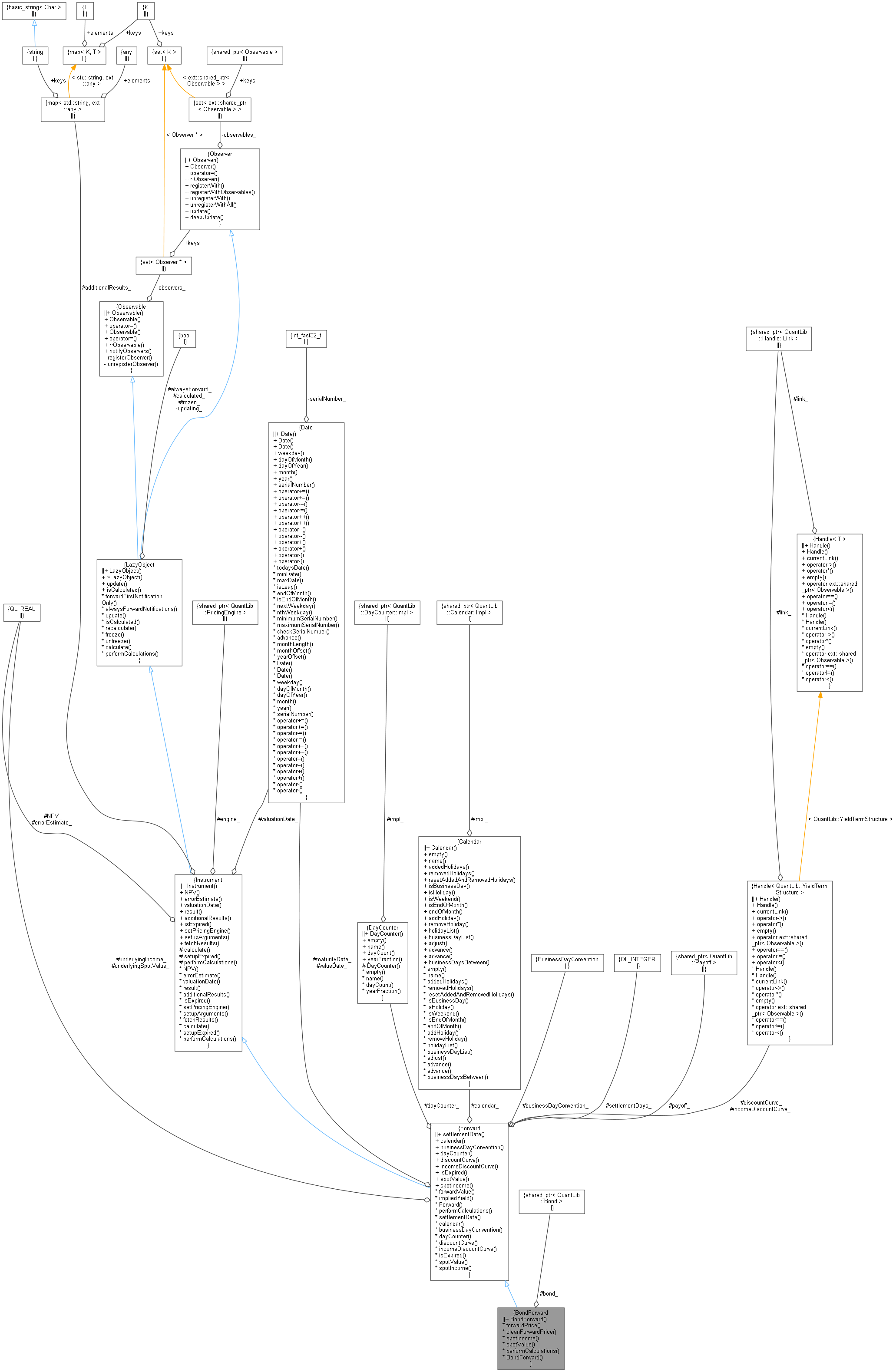

Inheritance diagram for BondForward: Collaboration diagram for BondForward:

Collaboration diagram for BondForward:

Public Member Functions | |

Constructors | |

| BondForward (const Date &valueDate, const Date &maturityDate, Position::Type type, Real strike, Natural settlementDays, const DayCounter &dayCounter, const Calendar &calendar, BusinessDayConvention businessDayConvention, const ext::shared_ptr< Bond > &bond, const Handle< YieldTermStructure > &discountCurve=Handle< YieldTermStructure >(), const Handle< YieldTermStructure > &incomeDiscountCurve=Handle< YieldTermStructure >()) | |

| Public Member Functions inherited from Forward | |

| virtual Date | settlementDate () const |

| const Calendar & | calendar () const |

| BusinessDayConvention | businessDayConvention () const |

| const DayCounter & | dayCounter () const |

| Handle< YieldTermStructure > | discountCurve () const |

| term structure relevant to the contract (e.g. repo curve) More... | |

| Handle< YieldTermStructure > | incomeDiscountCurve () const |

| term structure that discounts the underlying's income cash flows More... | |

| bool | isExpired () const override |

| returns whether the instrument is still tradable. More... | |

| virtual Real | forwardValue () const |

| forward value/price of underlying, discounting income/dividends More... | |

| InterestRate | impliedYield (Real underlyingSpotValue, Real forwardValue, Date settlementDate, Compounding compoundingConvention, const DayCounter &dayCounter) |

| Public Member Functions inherited from Instrument | |

| Instrument () | |

| Real | NPV () const |

| returns the net present value of the instrument. More... | |

| Real | errorEstimate () const |

| returns the error estimate on the NPV when available. More... | |

| const Date & | valuationDate () const |

| returns the date the net present value refers to. More... | |

| template<typename T > | |

| T | result (const std::string &tag) const |

| returns any additional result returned by the pricing engine. More... | |

| const std::map< std::string, ext::any > & | additionalResults () const |

| returns all additional result returned by the pricing engine. More... | |

| void | setPricingEngine (const ext::shared_ptr< PricingEngine > &) |

| set the pricing engine to be used. More... | |

| virtual void | setupArguments (PricingEngine::arguments *) const |

| virtual void | fetchResults (const PricingEngine::results *) const |

| Public Member Functions inherited from LazyObject | |

| LazyObject () | |

| ~LazyObject () override=default | |

| void | update () override |

| bool | isCalculated () const |

| void | forwardFirstNotificationOnly () |

| void | alwaysForwardNotifications () |

| void | recalculate () |

| void | freeze () |

| void | unfreeze () |

| Public Member Functions inherited from Observable | |

| Observable ()=default | |

| Observable (const Observable &) | |

| Observable & | operator= (const Observable &) |

| Observable (Observable &&)=delete | |

| Observable & | operator= (Observable &&)=delete |

| virtual | ~Observable ()=default |

| void | notifyObservers () |

| Public Member Functions inherited from Observer | |

| Observer ()=default | |

| Observer (const Observer &) | |

| Observer & | operator= (const Observer &) |

| virtual | ~Observer () |

| std::pair< iterator, bool > | registerWith (const ext::shared_ptr< Observable > &) |

| void | registerWithObservables (const ext::shared_ptr< Observer > &) |

| Size | unregisterWith (const ext::shared_ptr< Observable > &) |

| void | unregisterWithAll () |

| virtual void | update ()=0 |

| virtual void | deepUpdate () |

Calculations | |

| ext::shared_ptr< Bond > | bond_ |

| Real | forwardPrice () const |

| (dirty) forward bond price More... | |

| Real | cleanForwardPrice () const |

| (dirty) forward bond price minus accrued on bond at delivery More... | |

| Real | spotIncome (const Handle< YieldTermStructure > &incomeDiscountCurve) const override |

| NPV of bond coupons discounted using incomeDiscountCurve. More... | |

| Real | spotValue () const override |

| NPV of underlying bond. More... | |

| void | performCalculations () const override |

Additional Inherited Members | |

| Public Types inherited from Observer | |

| typedef set_type::iterator | iterator |

| Protected Member Functions inherited from Forward | |

| Forward (DayCounter dayCounter, Calendar calendar, BusinessDayConvention businessDayConvention, Natural settlementDays, ext::shared_ptr< Payoff > payoff, const Date &valueDate, const Date &maturityDate, Handle< YieldTermStructure > discountCurve=Handle< YieldTermStructure >()) | |

| void | performCalculations () const override |

| Protected Member Functions inherited from Instrument | |

| void | calculate () const override |

| virtual void | setupExpired () const |

| Protected Member Functions inherited from LazyObject | |

| Protected Attributes inherited from Forward | |

| Real | underlyingIncome_ |

| Real | underlyingSpotValue_ |

| DayCounter | dayCounter_ |

| Calendar | calendar_ |

| BusinessDayConvention | businessDayConvention_ |

| Natural | settlementDays_ |

| ext::shared_ptr< Payoff > | payoff_ |

| Date | valueDate_ |

| Date | maturityDate_ |

| maturityDate of the forward contract or delivery date of underlying More... | |

| Handle< YieldTermStructure > | discountCurve_ |

| Handle< YieldTermStructure > | incomeDiscountCurve_ |

| Protected Attributes inherited from Instrument | |

| Real | NPV_ |

| Real | errorEstimate_ |

| Date | valuationDate_ |

| std::map< std::string, ext::any > | additionalResults_ |

| ext::shared_ptr< PricingEngine > | engine_ |

| Protected Attributes inherited from LazyObject | |

| bool | calculated_ = false |

| bool | frozen_ = false |

| bool | alwaysForward_ |

Detailed Description

Forward contract on a bond

- valueDate refers to the settlement date of the bond forward contract. maturityDate is the delivery (or repurchase) date for the underlying bond (not the bond's maturity date).

Relevant formulas used in the calculations ( \(P\) refers to a price):

a. \( P_{CleanFwd}(t) = P_{DirtyFwd}(t) - AI(t=deliveryDate) \) where \( AI \) refers to the accrued interest on the underlying bond.

b. \( P_{DirtyFwd}(t) = \frac{P_{DirtySpot}(t) - SpotIncome(t)} {discountCurve->discount(t=deliveryDate)} \)

c. \( SpotIncome(t) = \sum_i \left( CF_i \times incomeDiscountCurve->discount(t_i) \right) \) where \( CF_i \) represents the ith bond cash flow (coupon payment) associated with the underlying bond falling between the settlementDate and the deliveryDate. (Note the two different discount curves used in b. and c.)

- Warning:

- This class still needs to be rigorously tested

- Examples

- Repo.cpp.

Definition at line 69 of file bondforward.hpp.

Constructor & Destructor Documentation

◆ BondForward()

| BondForward | ( | const Date & | valueDate, |

| const Date & | maturityDate, | ||

| Position::Type | type, | ||

| Real | strike, | ||

| Natural | settlementDays, | ||

| const DayCounter & | dayCounter, | ||

| const Calendar & | calendar, | ||

| BusinessDayConvention | businessDayConvention, | ||

| const ext::shared_ptr< Bond > & | bond, | ||

| const Handle< YieldTermStructure > & | discountCurve = Handle<YieldTermStructure>(), |

||

| const Handle< YieldTermStructure > & | incomeDiscountCurve = Handle<YieldTermStructure>() |

||

| ) |

If strike is given in the constructor, can calculate the NPV of the contract via NPV().

If strike/forward price is desired, it can be obtained via forwardPrice(). In this case, the strike variable in the constructor is irrelevant and will be ignored.

Definition at line 27 of file bondforward.cpp.

Here is the call graph for this function:

Member Function Documentation

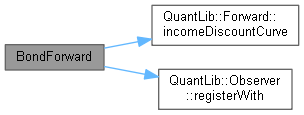

◆ forwardPrice()

| Real forwardPrice | ( | ) | const |

(dirty) forward bond price

- Examples

- Repo.cpp.

Definition at line 54 of file bondforward.cpp.

Here is the call graph for this function:

◆ cleanForwardPrice()

| Real cleanForwardPrice | ( | ) | const |

(dirty) forward bond price minus accrued on bond at delivery

- Examples

- Repo.cpp.

Definition at line 49 of file bondforward.cpp.

Here is the call graph for this function:

◆ spotIncome()

|

overridevirtual |

NPV of bond coupons discounted using incomeDiscountCurve.

Here only coupons between max(evaluation date,settlement date) and maturity date of bond forward contract are considered income.

Implements Forward.

- Examples

- Repo.cpp.

Definition at line 59 of file bondforward.cpp.

Here is the call graph for this function: Here is the caller graph for this function:

Here is the caller graph for this function:

◆ spotValue()

|

overridevirtual |

NPV of underlying bond.

Implements Forward.

Definition at line 86 of file bondforward.cpp.

Here is the caller graph for this function:

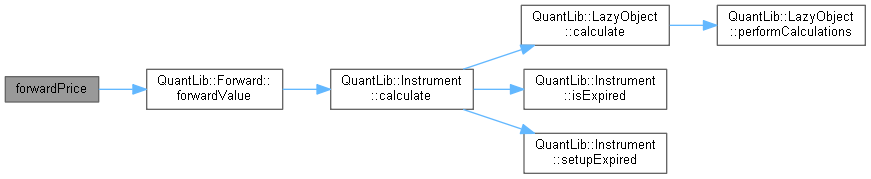

◆ performCalculations()

|

overrideprotectedvirtual |

In case a pricing engine is not used, this method must be overridden to perform the actual calculations and set any needed results. In case a pricing engine is used, the default implementation can be used.

Reimplemented from Instrument.

Definition at line 91 of file bondforward.cpp.

Here is the call graph for this function:

Member Data Documentation

◆ bond_

|

protected |

Definition at line 116 of file bondforward.hpp.