Abstract base class for option payoffs. More...

#include <payoff.hpp>

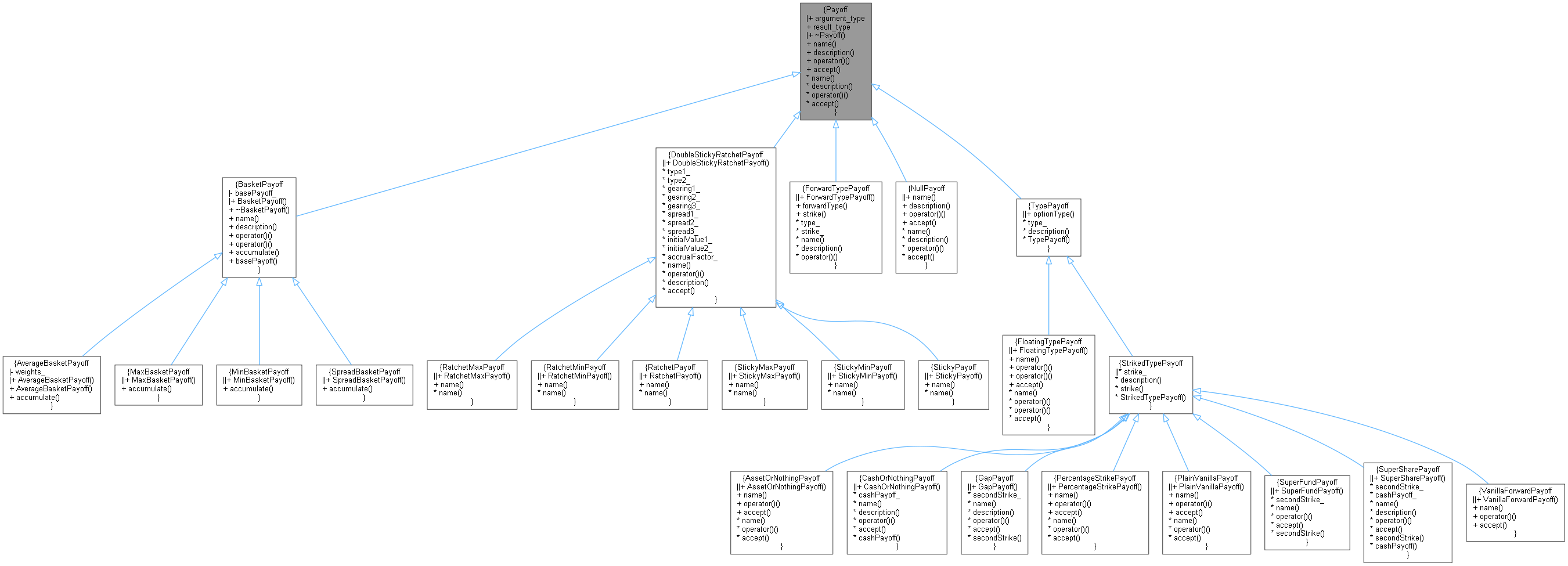

Inheritance diagram for Payoff:

Inheritance diagram for Payoff: Collaboration diagram for Payoff:

Collaboration diagram for Payoff:

Public Member Functions | |

| virtual | ~Payoff ()=default |

Payoff interface | |

| virtual std::string | name () const =0 |

| virtual std::string | description () const =0 |

| virtual Real | operator() (Real price) const =0 |

Visitability | |

| virtual void | accept (AcyclicVisitor &) |

Detailed Description

Abstract base class for option payoffs.

Definition at line 36 of file payoff.hpp.

Constructor & Destructor Documentation

◆ ~Payoff()

|

virtualdefault |

Member Function Documentation

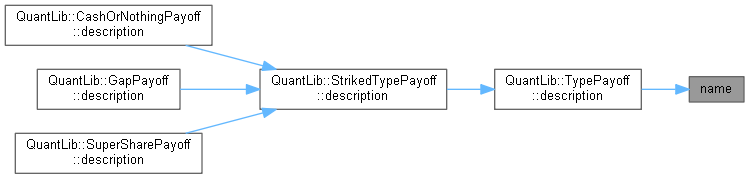

◆ name()

|

pure virtual |

- Warning:

- This method is used for output and comparison between payoffs. It is not meant to be used for writing switch-on-type code.

Implemented in BasketPayoff, ForwardTypePayoff, NullPayoff, FloatingTypePayoff, PlainVanillaPayoff, PercentageStrikePayoff, AssetOrNothingPayoff, CashOrNothingPayoff, GapPayoff, SuperFundPayoff, SuperSharePayoff, DoubleStickyRatchetPayoff, RatchetPayoff, StickyPayoff, RatchetMaxPayoff, RatchetMinPayoff, StickyMaxPayoff, StickyMinPayoff, and VanillaForwardPayoff.

Here is the caller graph for this function:

◆ description()

|

pure virtual |

Implemented in BasketPayoff, ForwardTypePayoff, NullPayoff, TypePayoff, StrikedTypePayoff, CashOrNothingPayoff, GapPayoff, SuperSharePayoff, and DoubleStickyRatchetPayoff.

◆ operator()()

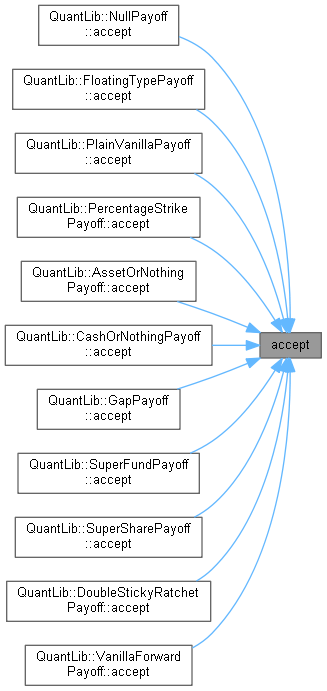

◆ accept()

|

virtual |

Reimplemented in NullPayoff, FloatingTypePayoff, PlainVanillaPayoff, PercentageStrikePayoff, AssetOrNothingPayoff, CashOrNothingPayoff, GapPayoff, SuperFundPayoff, SuperSharePayoff, DoubleStickyRatchetPayoff, and VanillaForwardPayoff.

Definition at line 58 of file payoff.hpp.

Here is the call graph for this function: Here is the caller graph for this function:

Here is the caller graph for this function: