Calibration of a local volatility surface to a sparse grid of options. More...

#include <andreasenhugevolatilityinterpl.hpp>

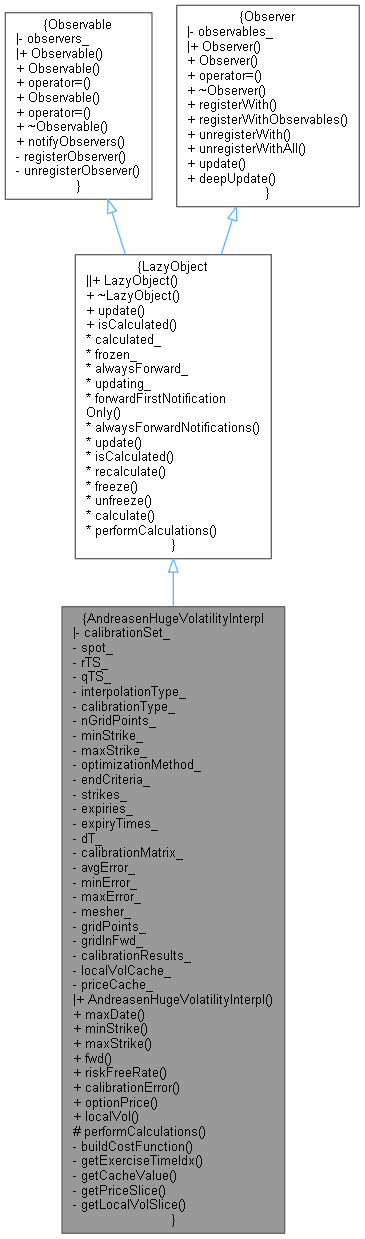

Inheritance diagram for AndreasenHugeVolatilityInterpl:

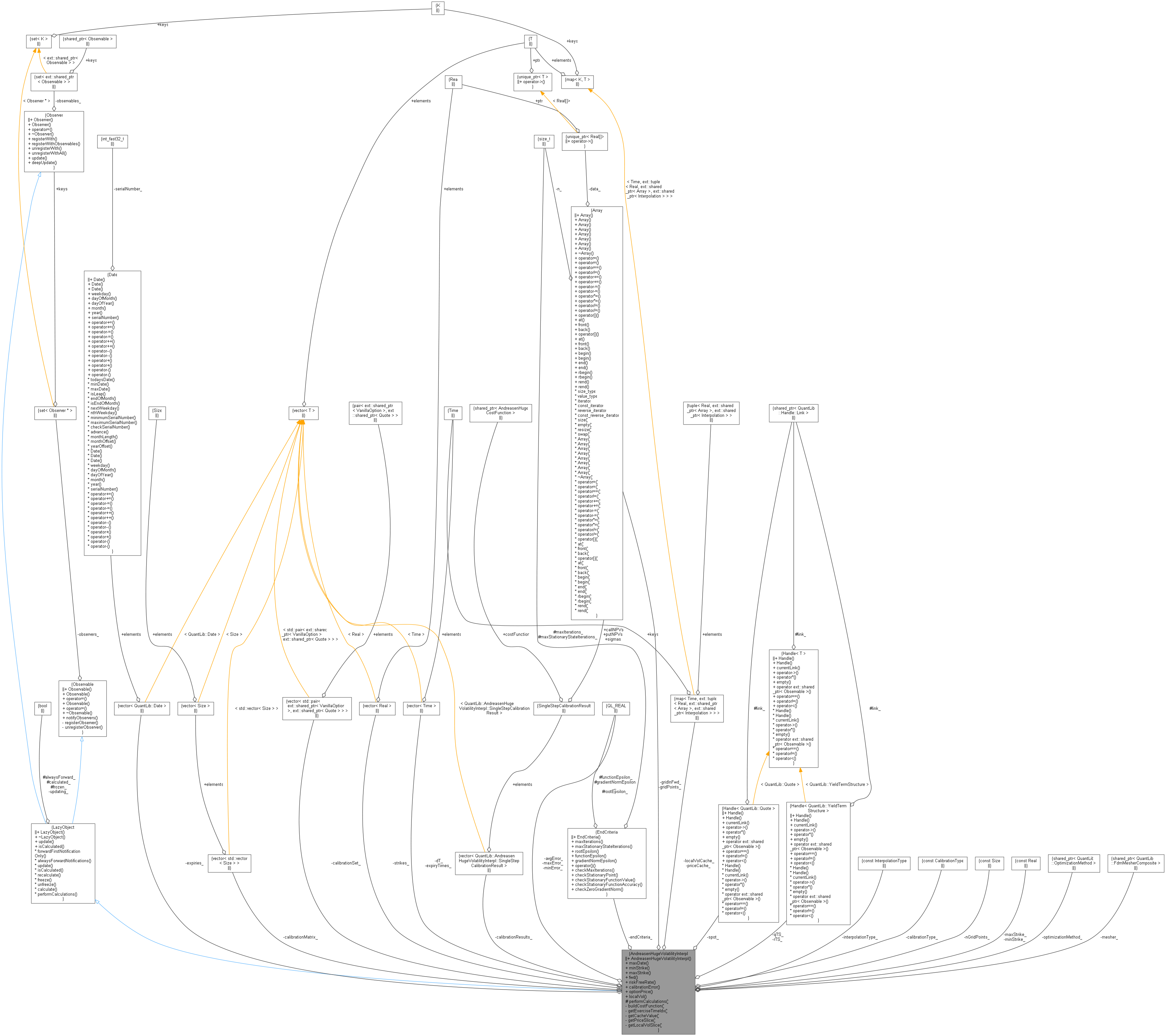

Inheritance diagram for AndreasenHugeVolatilityInterpl: Collaboration diagram for AndreasenHugeVolatilityInterpl:

Collaboration diagram for AndreasenHugeVolatilityInterpl:

Classes | |

| struct | SingleStepCalibrationResult |

Public Types | |

| enum | InterpolationType { PiecewiseConstant , Linear , CubicSpline } |

| enum | CalibrationType { Call = Option::Call , Put = Option::Put , CallPut } |

| typedef std::vector< std::pair< ext::shared_ptr< VanillaOption >, ext::shared_ptr< Quote > > > | CalibrationSet |

| Public Types inherited from Observer | |

| typedef set_type::iterator | iterator |

Public Member Functions | |

| AndreasenHugeVolatilityInterpl (const CalibrationSet &calibrationSet, Handle< Quote > spot, Handle< YieldTermStructure > rTS, Handle< YieldTermStructure > qTS, InterpolationType interpolationType=CubicSpline, CalibrationType calibrationType=Call, Size nGridPoints=500, Real minStrike=Null< Real >(), Real maxStrike=Null< Real >(), ext::shared_ptr< OptimizationMethod > optimizationMethod=ext::shared_ptr< OptimizationMethod >(new LevenbergMarquardt), const EndCriteria &endCriteria=EndCriteria(500, 100, 1e-12, 1e-10, 1e-10)) | |

| Date | maxDate () const |

| Real | minStrike () const |

| Real | maxStrike () const |

| Real | fwd (Time t) const |

| const Handle< YieldTermStructure > & | riskFreeRate () const |

| std::tuple< Real, Real, Real > | calibrationError () const |

| Real | optionPrice (Time t, Real strike, Option::Type optionType) const |

| Volatility | localVol (Time t, Real strike) const |

| Public Member Functions inherited from LazyObject | |

| LazyObject () | |

| ~LazyObject () override=default | |

| void | update () override |

| bool | isCalculated () const |

| void | forwardFirstNotificationOnly () |

| void | alwaysForwardNotifications () |

| void | recalculate () |

| void | freeze () |

| void | unfreeze () |

| Public Member Functions inherited from Observable | |

| Observable ()=default | |

| Observable (const Observable &) | |

| Observable & | operator= (const Observable &) |

| Observable (Observable &&)=delete | |

| Observable & | operator= (Observable &&)=delete |

| virtual | ~Observable ()=default |

| void | notifyObservers () |

| Public Member Functions inherited from Observer | |

| Observer ()=default | |

| Observer (const Observer &) | |

| Observer & | operator= (const Observer &) |

| virtual | ~Observer () |

| std::pair< iterator, bool > | registerWith (const ext::shared_ptr< Observable > &) |

| void | registerWithObservables (const ext::shared_ptr< Observer > &) |

| Size | unregisterWith (const ext::shared_ptr< Observable > &) |

| void | unregisterWithAll () |

| virtual void | update ()=0 |

| virtual void | deepUpdate () |

Protected Member Functions | |

| void | performCalculations () const override |

| Protected Member Functions inherited from LazyObject | |

| virtual void | calculate () const |

Private Types | |

| typedef std::map< Time, std::tuple< Real, ext::shared_ptr< Array >, ext::shared_ptr< Interpolation > > > | TimeValueCacheType |

Private Member Functions | |

| ext::shared_ptr< AndreasenHugeCostFunction > | buildCostFunction (Size iExpiry, Option::Type optionType, const Array &previousNPVs) const |

| Size | getExerciseTimeIdx (Time t) const |

| Real | getCacheValue (Real strike, const TimeValueCacheType::const_iterator &f) const |

| Array | getPriceSlice (Time t, Option::Type optionType) const |

| Array | getLocalVolSlice (Time t, Option::Type optionType) const |

Private Attributes | |

| CalibrationSet | calibrationSet_ |

| const Handle< Quote > | spot_ |

| const Handle< YieldTermStructure > | rTS_ |

| const Handle< YieldTermStructure > | qTS_ |

| const InterpolationType | interpolationType_ |

| const CalibrationType | calibrationType_ |

| const Size | nGridPoints_ |

| const Real | minStrike_ |

| const Real | maxStrike_ |

| const ext::shared_ptr< OptimizationMethod > | optimizationMethod_ |

| const EndCriteria | endCriteria_ |

| std::vector< Real > | strikes_ |

| std::vector< Date > | expiries_ |

| std::vector< Time > | expiryTimes_ |

| std::vector< Time > | dT_ |

| std::vector< std::vector< Size > > | calibrationMatrix_ |

| Real | avgError_ |

| Real | minError_ |

| Real | maxError_ |

| ext::shared_ptr< FdmMesherComposite > | mesher_ |

| Array | gridPoints_ |

| Array | gridInFwd_ |

| std::vector< SingleStepCalibrationResult > | calibrationResults_ |

| TimeValueCacheType | localVolCache_ |

| TimeValueCacheType | priceCache_ |

Additional Inherited Members | |

| Protected Attributes inherited from LazyObject | |

| bool | calculated_ = false |

| bool | frozen_ = false |

| bool | alwaysForward_ |

Detailed Description

Calibration of a local volatility surface to a sparse grid of options.

References:

Andreasen J., Huge B., 2010. Volatility Interpolation https://ssrn.com/abstract=1694972

Definition at line 54 of file andreasenhugevolatilityinterpl.hpp.

Member Typedef Documentation

◆ CalibrationSet

| typedef std::vector<std::pair< ext::shared_ptr<VanillaOption>, ext::shared_ptr<Quote> > > CalibrationSet |

Definition at line 63 of file andreasenhugevolatilityinterpl.hpp.

◆ TimeValueCacheType

|

private |

Definition at line 103 of file andreasenhugevolatilityinterpl.hpp.

Member Enumeration Documentation

◆ InterpolationType

| enum InterpolationType |

| Enumerator | |

|---|---|

| PiecewiseConstant | |

| Linear | |

| CubicSpline | |

Definition at line 57 of file andreasenhugevolatilityinterpl.hpp.

◆ CalibrationType

| enum CalibrationType |

| Enumerator | |

|---|---|

| Call | |

| Put | |

| CallPut | |

Definition at line 58 of file andreasenhugevolatilityinterpl.hpp.

Constructor & Destructor Documentation

◆ AndreasenHugeVolatilityInterpl()

| AndreasenHugeVolatilityInterpl | ( | const CalibrationSet & | calibrationSet, |

| Handle< Quote > | spot, | ||

| Handle< YieldTermStructure > | rTS, | ||

| Handle< YieldTermStructure > | qTS, | ||

| InterpolationType | interpolationType = CubicSpline, |

||

| CalibrationType | calibrationType = Call, |

||

| Size | nGridPoints = 500, |

||

| Real | minStrike = Null<Real>(), |

||

| Real | maxStrike = Null<Real>(), |

||

| ext::shared_ptr< OptimizationMethod > | optimizationMethod = ext::shared_ptr<OptimizationMethod>(new LevenbergMarquardt), |

||

| const EndCriteria & | endCriteria = EndCriteria(500, 100, 1e-12, 1e-10, 1e-10) |

||

| ) |

Definition at line 210 of file andreasenhugevolatilityinterpl.cpp.

Here is the call graph for this function:

Member Function Documentation

◆ maxDate()

| Date maxDate | ( | ) | const |

Definition at line 447 of file andreasenhugevolatilityinterpl.cpp.

◆ minStrike()

| Real minStrike | ( | ) | const |

Definition at line 451 of file andreasenhugevolatilityinterpl.cpp.

Here is the caller graph for this function:

◆ maxStrike()

| Real maxStrike | ( | ) | const |

Definition at line 456 of file andreasenhugevolatilityinterpl.cpp.

Here is the caller graph for this function:

◆ fwd()

Definition at line 461 of file andreasenhugevolatilityinterpl.cpp.

Here is the caller graph for this function:

◆ riskFreeRate()

| const Handle< YieldTermStructure > & riskFreeRate | ( | ) | const |

Definition at line 466 of file andreasenhugevolatilityinterpl.cpp.

◆ calibrationError()

Definition at line 471 of file andreasenhugevolatilityinterpl.cpp.

Here is the call graph for this function:

◆ optionPrice()

| Real optionPrice | ( | Time | t, |

| Real | strike, | ||

| Option::Type | optionType | ||

| ) | const |

Definition at line 508 of file andreasenhugevolatilityinterpl.cpp.

Here is the call graph for this function: Here is the caller graph for this function:

Here is the caller graph for this function:

◆ localVol()

| Volatility localVol | ( | Time | t, |

| Real | strike | ||

| ) | const |

Definition at line 591 of file andreasenhugevolatilityinterpl.cpp.

Here is the call graph for this function: Here is the caller graph for this function:

Here is the caller graph for this function:

◆ performCalculations()

|

overrideprotectedvirtual |

This method must implement any calculations which must be (re)done in order to calculate the desired results.

Implements LazyObject.

Definition at line 342 of file andreasenhugevolatilityinterpl.cpp.

Here is the call graph for this function:

◆ buildCostFunction()

|

private |

Definition at line 287 of file andreasenhugevolatilityinterpl.cpp.

Here is the call graph for this function: Here is the caller graph for this function:

Here is the caller graph for this function:

◆ getExerciseTimeIdx()

Definition at line 477 of file andreasenhugevolatilityinterpl.cpp.

Here is the caller graph for this function:

◆ getCacheValue()

Definition at line 484 of file andreasenhugevolatilityinterpl.cpp.

Here is the call graph for this function: Here is the caller graph for this function:

Here is the caller graph for this function:

◆ getPriceSlice()

|

private |

Definition at line 496 of file andreasenhugevolatilityinterpl.cpp.

Here is the call graph for this function: Here is the caller graph for this function:

Here is the caller graph for this function:

◆ getLocalVolSlice()

|

private |

Definition at line 558 of file andreasenhugevolatilityinterpl.cpp.

Here is the call graph for this function: Here is the caller graph for this function:

Here is the caller graph for this function:

Member Data Documentation

◆ calibrationSet_

|

private |

Definition at line 123 of file andreasenhugevolatilityinterpl.hpp.

◆ spot_

Definition at line 124 of file andreasenhugevolatilityinterpl.hpp.

◆ rTS_

|

private |

Definition at line 125 of file andreasenhugevolatilityinterpl.hpp.

◆ qTS_

|

private |

Definition at line 126 of file andreasenhugevolatilityinterpl.hpp.

◆ interpolationType_

|

private |

Definition at line 127 of file andreasenhugevolatilityinterpl.hpp.

◆ calibrationType_

|

private |

Definition at line 128 of file andreasenhugevolatilityinterpl.hpp.

◆ nGridPoints_

|

private |

Definition at line 130 of file andreasenhugevolatilityinterpl.hpp.

◆ minStrike_

|

private |

Definition at line 131 of file andreasenhugevolatilityinterpl.hpp.

◆ maxStrike_

|

private |

Definition at line 131 of file andreasenhugevolatilityinterpl.hpp.

◆ optimizationMethod_

|

private |

Definition at line 133 of file andreasenhugevolatilityinterpl.hpp.

◆ endCriteria_

|

private |

Definition at line 134 of file andreasenhugevolatilityinterpl.hpp.

◆ strikes_

|

private |

Definition at line 136 of file andreasenhugevolatilityinterpl.hpp.

◆ expiries_

|

private |

Definition at line 137 of file andreasenhugevolatilityinterpl.hpp.

◆ expiryTimes_

|

mutableprivate |

Definition at line 138 of file andreasenhugevolatilityinterpl.hpp.

◆ dT_

|

private |

Definition at line 138 of file andreasenhugevolatilityinterpl.hpp.

◆ calibrationMatrix_

|

private |

Definition at line 140 of file andreasenhugevolatilityinterpl.hpp.

◆ avgError_

|

mutableprivate |

Definition at line 141 of file andreasenhugevolatilityinterpl.hpp.

◆ minError_

|

private |

Definition at line 141 of file andreasenhugevolatilityinterpl.hpp.

◆ maxError_

|

private |

Definition at line 141 of file andreasenhugevolatilityinterpl.hpp.

◆ mesher_

|

mutableprivate |

Definition at line 143 of file andreasenhugevolatilityinterpl.hpp.

◆ gridPoints_

|

mutableprivate |

Definition at line 144 of file andreasenhugevolatilityinterpl.hpp.

◆ gridInFwd_

|

private |

Definition at line 144 of file andreasenhugevolatilityinterpl.hpp.

◆ calibrationResults_

|

mutableprivate |

Definition at line 146 of file andreasenhugevolatilityinterpl.hpp.

◆ localVolCache_

|

mutableprivate |

Definition at line 148 of file andreasenhugevolatilityinterpl.hpp.

◆ priceCache_

|

private |

Definition at line 148 of file andreasenhugevolatilityinterpl.hpp.