Libor forward model More...

#include <liborforwardmodel.hpp>

Inheritance diagram for LiborForwardModel:

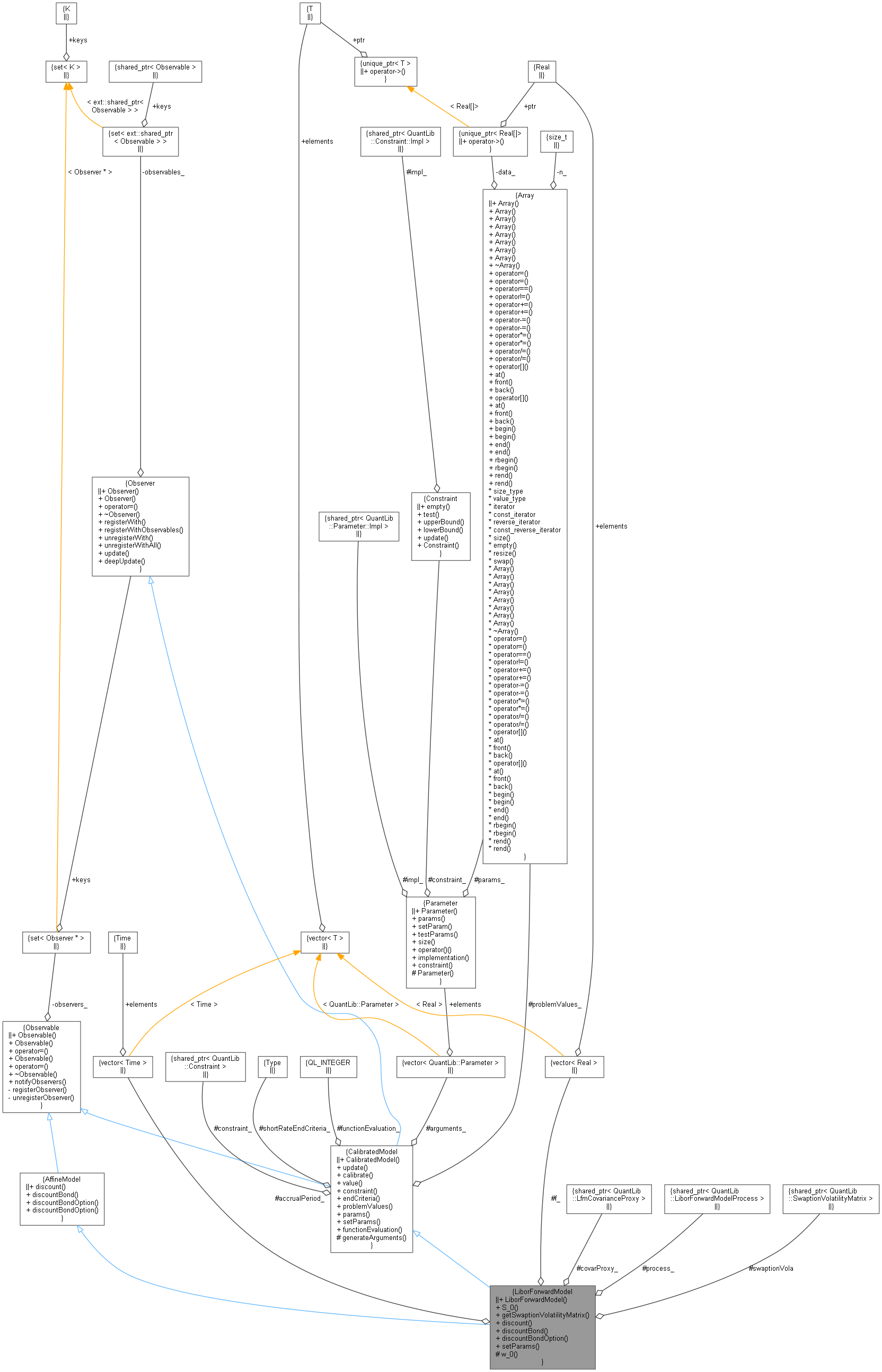

Inheritance diagram for LiborForwardModel: Collaboration diagram for LiborForwardModel:

Collaboration diagram for LiborForwardModel:

Public Member Functions | |

| LiborForwardModel (const ext::shared_ptr< LiborForwardModelProcess > &process, const ext::shared_ptr< LmVolatilityModel > &volaModel, const ext::shared_ptr< LmCorrelationModel > &corrModel) | |

| Rate | S_0 (Size alpha, Size beta) const |

| virtual ext::shared_ptr< SwaptionVolatilityMatrix > | getSwaptionVolatilityMatrix () const |

| DiscountFactor | discount (Time t) const override |

| Implied discount curve. More... | |

| Real | discountBond (Time now, Time maturity, Array factors) const override |

| Real | discountBondOption (Option::Type type, Real strike, Time maturity, Time bondMaturity) const override |

| void | setParams (const Array ¶ms) override |

| Public Member Functions inherited from CalibratedModel | |

| CalibratedModel (Size nArguments) | |

| void | update () override |

| virtual void | calibrate (const std::vector< ext::shared_ptr< CalibrationHelper > > &, OptimizationMethod &method, const EndCriteria &endCriteria, const Constraint &constraint=Constraint(), const std::vector< Real > &weights=std::vector< Real >(), const std::vector< bool > &fixParameters=std::vector< bool >()) |

| Calibrate to a set of market instruments (usually caps/swaptions) More... | |

| Real | value (const Array ¶ms, const std::vector< ext::shared_ptr< CalibrationHelper > > &) |

| const ext::shared_ptr< Constraint > & | constraint () const |

| EndCriteria::Type | endCriteria () const |

| Returns end criteria result. More... | |

| const Array & | problemValues () const |

| Returns the problem values. More... | |

| Array | params () const |

| Returns array of arguments on which calibration is done. More... | |

| virtual void | setParams (const Array ¶ms) |

| Integer | functionEvaluation () const |

| Public Member Functions inherited from Observer | |

| Observer ()=default | |

| Observer (const Observer &) | |

| Observer & | operator= (const Observer &) |

| virtual | ~Observer () |

| std::pair< iterator, bool > | registerWith (const ext::shared_ptr< Observable > &) |

| void | registerWithObservables (const ext::shared_ptr< Observer > &) |

| Size | unregisterWith (const ext::shared_ptr< Observable > &) |

| void | unregisterWithAll () |

| virtual void | update ()=0 |

| virtual void | deepUpdate () |

| Public Member Functions inherited from Observable | |

| Observable ()=default | |

| Observable (const Observable &) | |

| Observable & | operator= (const Observable &) |

| Observable (Observable &&)=delete | |

| Observable & | operator= (Observable &&)=delete |

| virtual | ~Observable ()=default |

| void | notifyObservers () |

| Public Member Functions inherited from AffineModel | |

| virtual DiscountFactor | discount (Time t) const =0 |

| Implied discount curve. More... | |

| virtual Real | discountBond (Time now, Time maturity, Array factors) const =0 |

| virtual Real | discountBondOption (Option::Type type, Real strike, Time maturity, Time bondMaturity) const =0 |

| virtual Real | discountBondOption (Option::Type type, Real strike, Time maturity, Time bondStart, Time bondMaturity) const |

Protected Member Functions | |

| Array | w_0 (Size alpha, Size beta) const |

| Protected Member Functions inherited from CalibratedModel | |

| virtual void | generateArguments () |

Protected Attributes | |

| std::vector< Real > | f_ |

| std::vector< Time > | accrualPeriod_ |

| const ext::shared_ptr< LfmCovarianceProxy > | covarProxy_ |

| const ext::shared_ptr< LiborForwardModelProcess > | process_ |

| ext::shared_ptr< SwaptionVolatilityMatrix > | swaptionVola |

| Protected Attributes inherited from CalibratedModel | |

| std::vector< Parameter > | arguments_ |

| ext::shared_ptr< Constraint > | constraint_ |

| EndCriteria::Type | shortRateEndCriteria_ = EndCriteria::None |

| Array | problemValues_ |

| Integer | functionEvaluation_ |

Additional Inherited Members | |

| Public Types inherited from Observer | |

| typedef set_type::iterator | iterator |

Detailed Description

Libor forward model

References:

Stefan Weber, 2005, Efficient Calibration for Libor Market Models, (http://workshop.mathfinance.de/2005/papers/weber/slides.pdf)

Damiano Brigo, Fabio Mercurio, Massimo Morini, 2003, Different Covariance Parameterizations of Libor Market Model and Joint Caps/Swaptions Calibration, (http://www.business.uts.edu.au/qfrc/conferences/qmf2001/Brigo_D.pdf

- Tests:

- the correctness is tested using Monte-Carlo Simulation to reproduce swaption npvs, model calibration and exact cap pricing

Definition at line 51 of file liborforwardmodel.hpp.

Constructor & Destructor Documentation

◆ LiborForwardModel()

| LiborForwardModel | ( | const ext::shared_ptr< LiborForwardModelProcess > & | process, |

| const ext::shared_ptr< LmVolatilityModel > & | volaModel, | ||

| const ext::shared_ptr< LmCorrelationModel > & | corrModel | ||

| ) |

Definition at line 27 of file liborforwardmodel.cpp.

Member Function Documentation

◆ S_0()

Definition at line 130 of file liborforwardmodel.cpp.

Here is the call graph for this function: Here is the caller graph for this function:

Here is the caller graph for this function:

◆ getSwaptionVolatilityMatrix()

|

virtual |

◆ discount()

|

overridevirtual |

Implied discount curve.

Implements AffineModel.

Definition at line 203 of file liborforwardmodel.cpp.

Here is the caller graph for this function:

◆ discountBond()

Implements AffineModel.

Definition at line 207 of file liborforwardmodel.cpp.

Here is the call graph for this function:

◆ discountBondOption()

|

overridevirtual |

Implements AffineModel.

Definition at line 64 of file liborforwardmodel.cpp.

Here is the call graph for this function:

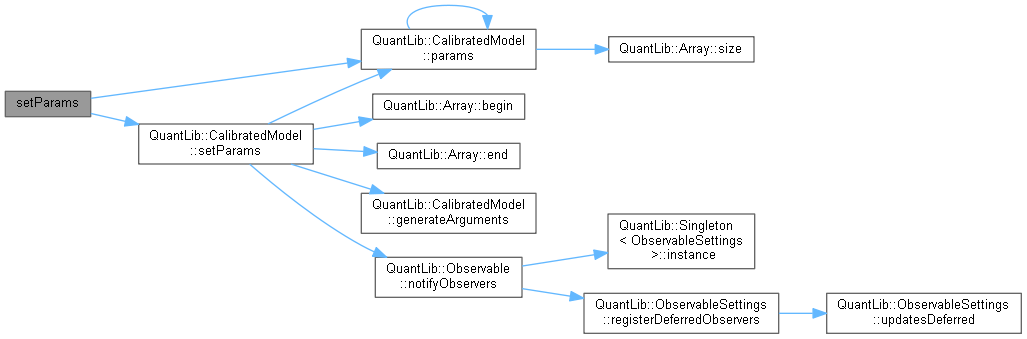

◆ setParams()

|

overridevirtual |

Reimplemented from CalibratedModel.

Definition at line 51 of file liborforwardmodel.cpp.

Here is the call graph for this function:

◆ w_0()

Member Data Documentation

◆ f_

|

protected |

Definition at line 76 of file liborforwardmodel.hpp.

◆ accrualPeriod_

|

protected |

Definition at line 77 of file liborforwardmodel.hpp.

◆ covarProxy_

|

protected |

Definition at line 79 of file liborforwardmodel.hpp.

◆ process_

|

protected |

Definition at line 80 of file liborforwardmodel.hpp.

◆ swaptionVola

|

mutableprotected |

Definition at line 82 of file liborforwardmodel.hpp.