libor-forward-model process More...

#include <lfmprocess.hpp>

Inheritance diagram for LiborForwardModelProcess:

Inheritance diagram for LiborForwardModelProcess: Collaboration diagram for LiborForwardModelProcess:

Collaboration diagram for LiborForwardModelProcess:

Public Member Functions | |

| LiborForwardModelProcess (Size size, ext::shared_ptr< IborIndex > index) | |

| Array | initialValues () const override |

| returns the initial values of the state variables More... | |

| Array | drift (Time t, const Array &x) const override |

| returns the drift part of the equation, i.e., \( \mu(t, \mathrm{x}_t) \) More... | |

| Matrix | diffusion (Time t, const Array &x) const override |

| returns the diffusion part of the equation, i.e. \( \sigma(t, \mathrm{x}_t) \) More... | |

| Matrix | covariance (Time t0, const Array &x0, Time dt) const override |

| Array | apply (const Array &x0, const Array &dx) const override |

| Array | evolve (Time t0, const Array &x0, Time dt, const Array &dw) const override |

| Size | size () const override |

| returns the number of dimensions of the stochastic process More... | |

| Size | factors () const override |

| returns the number of independent factors of the process More... | |

| ext::shared_ptr< IborIndex > | index () const |

| Leg | cashFlows (Real amount=1.0) const |

| void | setCovarParam (const ext::shared_ptr< LfmCovarianceParameterization > ¶m) |

| ext::shared_ptr< LfmCovarianceParameterization > | covarParam () const |

| Size | nextIndexReset (Time t) const |

| const std::vector< Time > & | fixingTimes () const |

| const std::vector< Date > & | fixingDates () const |

| const std::vector< Time > & | accrualStartTimes () const |

| const std::vector< Time > & | accrualEndTimes () const |

| std::vector< DiscountFactor > | discountBond (const std::vector< Rate > &rates) const |

| Public Member Functions inherited from StochasticProcess | |

| ~StochasticProcess () override=default | |

| virtual Array | expectation (Time t0, const Array &x0, Time dt) const |

| virtual Matrix | stdDeviation (Time t0, const Array &x0, Time dt) const |

| virtual Time | time (const Date &) const |

| void | update () override |

| Public Member Functions inherited from Observer | |

| Observer ()=default | |

| Observer (const Observer &) | |

| Observer & | operator= (const Observer &) |

| virtual | ~Observer () |

| std::pair< iterator, bool > | registerWith (const ext::shared_ptr< Observable > &) |

| void | registerWithObservables (const ext::shared_ptr< Observer > &) |

| Size | unregisterWith (const ext::shared_ptr< Observable > &) |

| void | unregisterWithAll () |

| virtual void | update ()=0 |

| virtual void | deepUpdate () |

| Public Member Functions inherited from Observable | |

| Observable ()=default | |

| Observable (const Observable &) | |

| Observable & | operator= (const Observable &) |

| Observable (Observable &&)=delete | |

| Observable & | operator= (Observable &&)=delete |

| virtual | ~Observable ()=default |

| void | notifyObservers () |

Private Attributes | |

| Size | size_ |

| const ext::shared_ptr< IborIndex > | index_ |

| ext::shared_ptr< LfmCovarianceParameterization > | lfmParam_ |

| Array | initialValues_ |

| std::vector< Time > | fixingTimes_ |

| std::vector< Date > | fixingDates_ |

| std::vector< Time > | accrualStartTimes_ |

| std::vector< Time > | accrualEndTimes_ |

| std::vector< Time > | accrualPeriod_ |

| Array | m1 |

| Array | m2 |

Additional Inherited Members | |

| Public Types inherited from Observer | |

| typedef set_type::iterator | iterator |

| Protected Member Functions inherited from StochasticProcess | |

| StochasticProcess ()=default | |

| StochasticProcess (ext::shared_ptr< discretization >) | |

| Protected Attributes inherited from StochasticProcess | |

| ext::shared_ptr< discretization > | discretization_ |

Detailed Description

libor-forward-model process

stochastic process of a libor forward model using the rolling forward measure incl. predictor-corrector step

References:

Glasserman, Paul, 2004, Monte Carlo Methods in Financial Engineering, Springer, Section 3.7

Antoon Pelsser, 2000, Efficient Methods for Valuing Interest Rate Derivatives, Springer, 8

Hull, John, White, Alan, 1999, Forward Rate Volatilities, Swap Rate Volatilities and the Implementation of the Libor Market Model (http://www.rotman.utoronto.ca/~amackay/fin/libormktmodel2.pdf)

- Tests:

- the correctness is tested by Monte-Carlo reproduction of caplet & ratchet NPVs and comparison with Black pricing.

- Warning:

- this class does not work correctly with Visual C++ 6.

Definition at line 58 of file lfmprocess.hpp.

Constructor & Destructor Documentation

◆ LiborForwardModelProcess()

| LiborForwardModelProcess | ( | Size | size, |

| ext::shared_ptr< IborIndex > | index | ||

| ) |

Member Function Documentation

◆ initialValues()

|

overridevirtual |

returns the initial values of the state variables

Implements StochasticProcess.

Definition at line 147 of file lfmprocess.cpp.

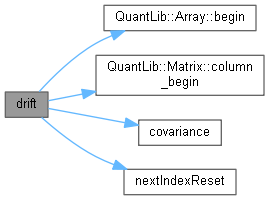

◆ drift()

returns the drift part of the equation, i.e., \( \mu(t, \mathrm{x}_t) \)

Implements StochasticProcess.

Definition at line 68 of file lfmprocess.cpp.

Here is the call graph for this function:

◆ diffusion()

returns the diffusion part of the equation, i.e. \( \sigma(t, \mathrm{x}_t) \)

Implements StochasticProcess.

Definition at line 85 of file lfmprocess.cpp.

◆ covariance()

returns the covariance \( V(\mathrm{x}_{t_0 + \Delta t} | \mathrm{x}_{t_0} = \mathrm{x}_0) \) of the process after a time interval \( \Delta t \) according to the given discretization. This method can be overridden in derived classes which want to hard-code a particular discretization.

Reimplemented from StochasticProcess.

Definition at line 89 of file lfmprocess.cpp.

Here is the caller graph for this function:

◆ apply()

applies a change to the asset value. By default, it returns \( \mathrm{x} + \Delta \mathrm{x} \).

Reimplemented from StochasticProcess.

Definition at line 93 of file lfmprocess.cpp.

◆ evolve()

returns the asset value after a time interval \( \Delta t \) according to the given discretization. By default, it returns

\[ E(\mathrm{x}_0,t_0,\Delta t) + S(\mathrm{x}_0,t_0,\Delta t) \cdot \Delta \mathrm{w} \]

where \( E \) is the expectation and \( S \) the standard deviation.

Reimplemented from StochasticProcess.

Definition at line 103 of file lfmprocess.cpp.

Here is the call graph for this function:

◆ size()

|

overridevirtual |

returns the number of dimensions of the stochastic process

Implements StochasticProcess.

Definition at line 183 of file lfmprocess.cpp.

◆ factors()

|

overridevirtual |

returns the number of independent factors of the process

Reimplemented from StochasticProcess.

Definition at line 187 of file lfmprocess.cpp.

◆ index()

| ext::shared_ptr< IborIndex > index | ( | ) | const |

Definition at line 162 of file lfmprocess.cpp.

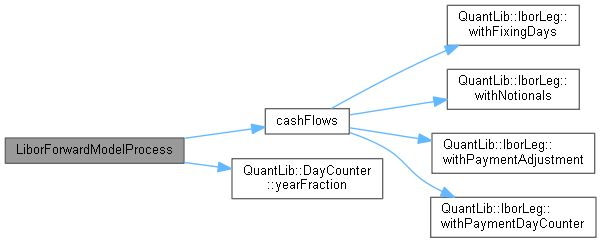

◆ cashFlows()

Definition at line 167 of file lfmprocess.cpp.

Here is the call graph for this function: Here is the caller graph for this function:

Here is the caller graph for this function:

◆ setCovarParam()

| void setCovarParam | ( | const ext::shared_ptr< LfmCovarianceParameterization > & | param | ) |

Definition at line 151 of file lfmprocess.cpp.

◆ covarParam()

| ext::shared_ptr< LfmCovarianceParameterization > covarParam | ( | ) | const |

Definition at line 157 of file lfmprocess.cpp.

◆ nextIndexReset()

◆ fixingTimes()

| const std::vector< Time > & fixingTimes | ( | ) | const |

Definition at line 191 of file lfmprocess.cpp.

◆ fixingDates()

| const std::vector< Date > & fixingDates | ( | ) | const |

Definition at line 195 of file lfmprocess.cpp.

◆ accrualStartTimes()

| const std::vector< Time > & accrualStartTimes | ( | ) | const |

Definition at line 200 of file lfmprocess.cpp.

◆ accrualEndTimes()

| const std::vector< Time > & accrualEndTimes | ( | ) | const |

Definition at line 205 of file lfmprocess.cpp.

◆ discountBond()

| std::vector< DiscountFactor > discountBond | ( | const std::vector< Rate > & | rates | ) | const |

Definition at line 214 of file lfmprocess.cpp.

Member Data Documentation

◆ size_

|

private |

Definition at line 93 of file lfmprocess.hpp.

◆ index_

|

private |

Definition at line 95 of file lfmprocess.hpp.

◆ lfmParam_

|

private |

Definition at line 96 of file lfmprocess.hpp.

◆ initialValues_

|

private |

Definition at line 98 of file lfmprocess.hpp.

◆ fixingTimes_

|

private |

Definition at line 100 of file lfmprocess.hpp.

◆ fixingDates_

|

private |

Definition at line 101 of file lfmprocess.hpp.

◆ accrualStartTimes_

|

private |

Definition at line 102 of file lfmprocess.hpp.

◆ accrualEndTimes_

|

private |

Definition at line 103 of file lfmprocess.hpp.

◆ accrualPeriod_

|

private |

Definition at line 104 of file lfmprocess.hpp.

◆ m1

|

mutableprivate |

Definition at line 106 of file lfmprocess.hpp.

◆ m2

|

private |

Definition at line 106 of file lfmprocess.hpp.