Affine model class. More...

#include <model.hpp>

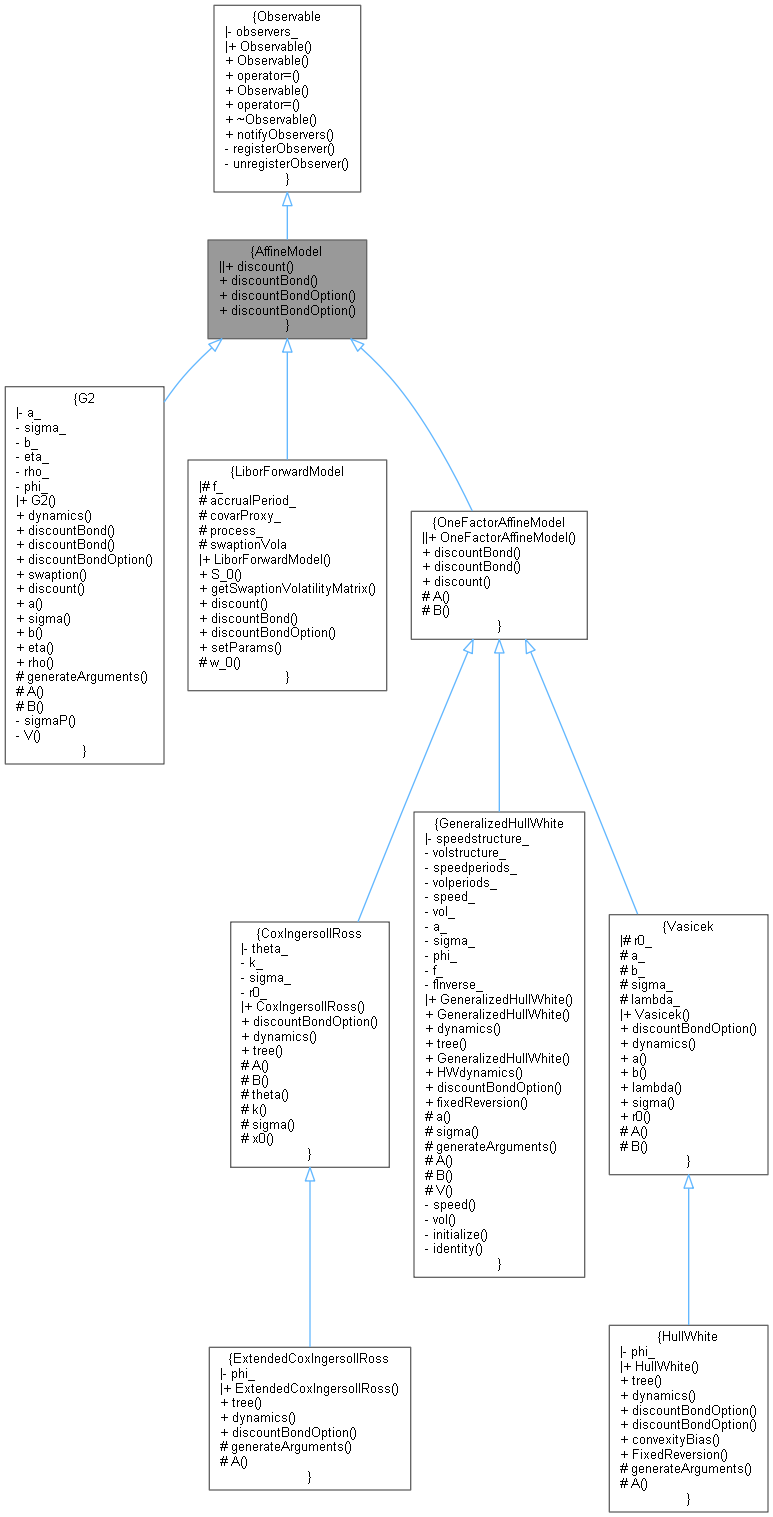

Inheritance diagram for AffineModel:

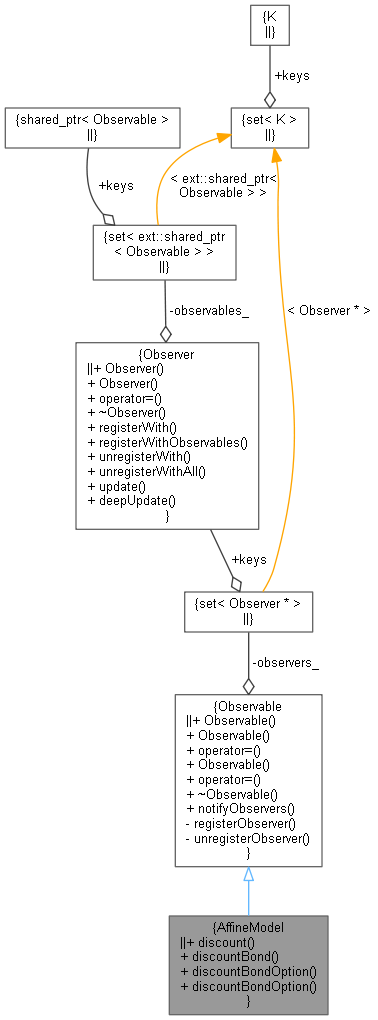

Inheritance diagram for AffineModel: Collaboration diagram for AffineModel:

Collaboration diagram for AffineModel:

Public Member Functions | |

| virtual DiscountFactor | discount (Time t) const =0 |

| Implied discount curve. More... | |

| virtual Real | discountBond (Time now, Time maturity, Array factors) const =0 |

| virtual Real | discountBondOption (Option::Type type, Real strike, Time maturity, Time bondMaturity) const =0 |

| virtual Real | discountBondOption (Option::Type type, Real strike, Time maturity, Time bondStart, Time bondMaturity) const |

| Public Member Functions inherited from Observable | |

| Observable ()=default | |

| Observable (const Observable &) | |

| Observable & | operator= (const Observable &) |

| Observable (Observable &&)=delete | |

| Observable & | operator= (Observable &&)=delete |

| virtual | ~Observable ()=default |

| void | notifyObservers () |

Detailed Description

Affine model class.

Base class for analytically tractable models.

Member Function Documentation

◆ discount()

|

pure virtual |

Implied discount curve.

Implemented in LiborForwardModel, OneFactorAffineModel, and G2.

◆ discountBond()

Implemented in LiborForwardModel, OneFactorAffineModel, and G2.

◆ discountBondOption() [1/2]

|

pure virtual |

Implemented in GeneralizedHullWhite, LiborForwardModel, CoxIngersollRoss, ExtendedCoxIngersollRoss, HullWhite, Vasicek, and G2.

Here is the caller graph for this function: