Pricing engine for irregular swaptions. More...

#include <haganirregularswaptionengine.hpp>

Inheritance diagram for HaganIrregularSwaptionEngine:

Inheritance diagram for HaganIrregularSwaptionEngine: Collaboration diagram for HaganIrregularSwaptionEngine:

Collaboration diagram for HaganIrregularSwaptionEngine:

Classes | |

| class | Basket |

Public Member Functions | |

| HaganIrregularSwaptionEngine (Handle< SwaptionVolatilityStructure >, Handle< YieldTermStructure > termStructure=Handle< YieldTermStructure >()) | |

| void | calculate () const override |

| Real | HKPrice (Basket &basket, ext::shared_ptr< Exercise > &exercise) const |

| Real | LGMPrice (Basket &basket, ext::shared_ptr< Exercise > &exercise) const |

| Public Member Functions inherited from GenericEngine< IrregularSwaption::arguments, IrregularSwaption::results > | |

| PricingEngine::arguments * | getArguments () const override |

| const PricingEngine::results * | getResults () const override |

| void | reset () override |

| void | update () override |

| Public Member Functions inherited from PricingEngine | |

| ~PricingEngine () override=default | |

| virtual arguments * | getArguments () const =0 |

| virtual const results * | getResults () const =0 |

| virtual void | reset ()=0 |

| virtual void | calculate () const =0 |

| Public Member Functions inherited from Observable | |

| Observable ()=default | |

| Observable (const Observable &) | |

| Observable & | operator= (const Observable &) |

| Observable (Observable &&)=delete | |

| Observable & | operator= (Observable &&)=delete |

| virtual | ~Observable ()=default |

| void | notifyObservers () |

| Public Member Functions inherited from Observer | |

| Observer ()=default | |

| Observer (const Observer &) | |

| Observer & | operator= (const Observer &) |

| virtual | ~Observer () |

| std::pair< iterator, bool > | registerWith (const ext::shared_ptr< Observable > &) |

| void | registerWithObservables (const ext::shared_ptr< Observer > &) |

| Size | unregisterWith (const ext::shared_ptr< Observable > &) |

| void | unregisterWithAll () |

| virtual void | update ()=0 |

| virtual void | deepUpdate () |

Private Attributes | |

| Handle< YieldTermStructure > | termStructure_ |

| Handle< SwaptionVolatilityStructure > | volatilityStructure_ |

Additional Inherited Members | |

| Public Types inherited from Observer | |

| typedef set_type::iterator | iterator |

| Protected Attributes inherited from GenericEngine< IrregularSwaption::arguments, IrregularSwaption::results > | |

| IrregularSwaption::arguments | arguments_ |

| IrregularSwaption::results | results_ |

Detailed Description

Pricing engine for irregular swaptions.

References:

- P.S. Hagan: "Methodology for Callable Swaps and Bermudan 'Exercise into Swaptions'"

P.J. Hunt, J.E. Kennedy: "Implied interest rate pricing models", Finance Stochast. 2, 275-293 (1998)

- Warning:

- Currently a spread is not handled correctly; it should be a minor exercise to account for this feature as well;

Definition at line 48 of file haganirregularswaptionengine.hpp.

Constructor & Destructor Documentation

◆ HaganIrregularSwaptionEngine()

|

explicit |

Definition at line 221 of file haganirregularswaptionengine.cpp.

Here is the call graph for this function:

Member Function Documentation

◆ calculate()

|

overridevirtual |

Implements PricingEngine.

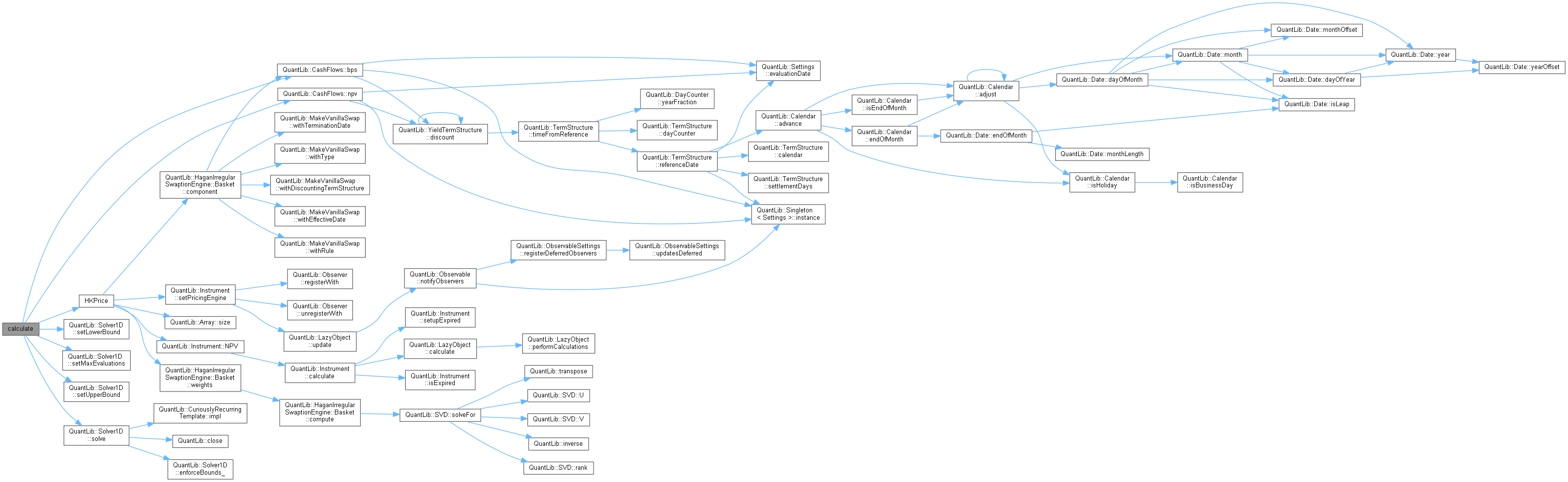

Definition at line 231 of file haganirregularswaptionengine.cpp.

Here is the call graph for this function:

◆ HKPrice()

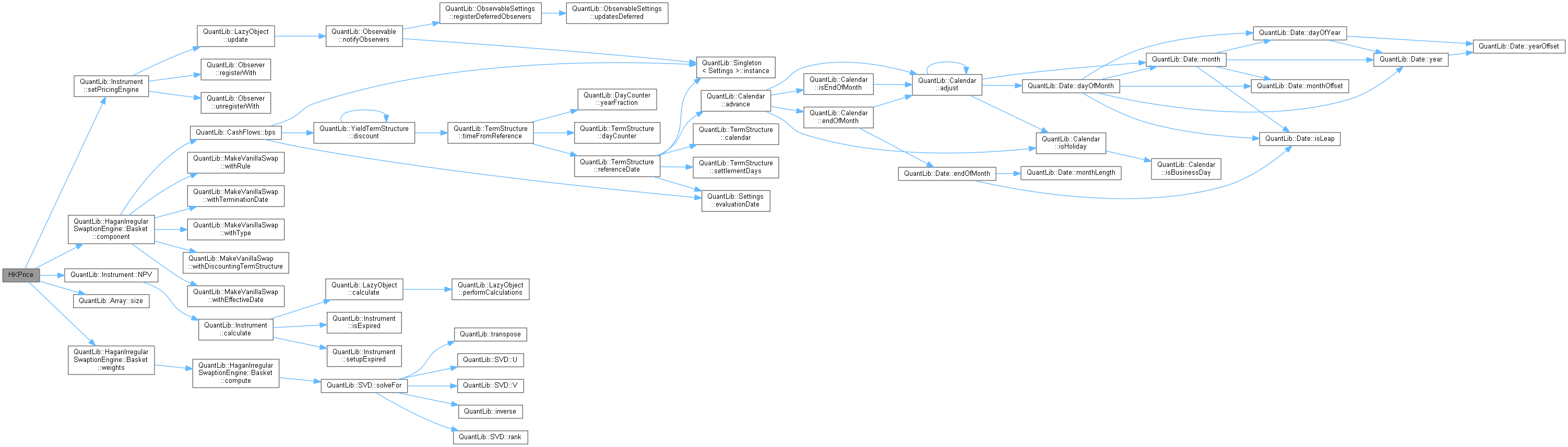

Definition at line 334 of file haganirregularswaptionengine.cpp.

Here is the call graph for this function: Here is the caller graph for this function:

Here is the caller graph for this function:

◆ LGMPrice()

Member Data Documentation

◆ termStructure_

|

private |

Definition at line 92 of file haganirregularswaptionengine.hpp.

◆ volatilityStructure_

|

private |

Definition at line 93 of file haganirregularswaptionengine.hpp.