#include <ql/experimental/swaptions/haganirregularswaptionengine.hpp>

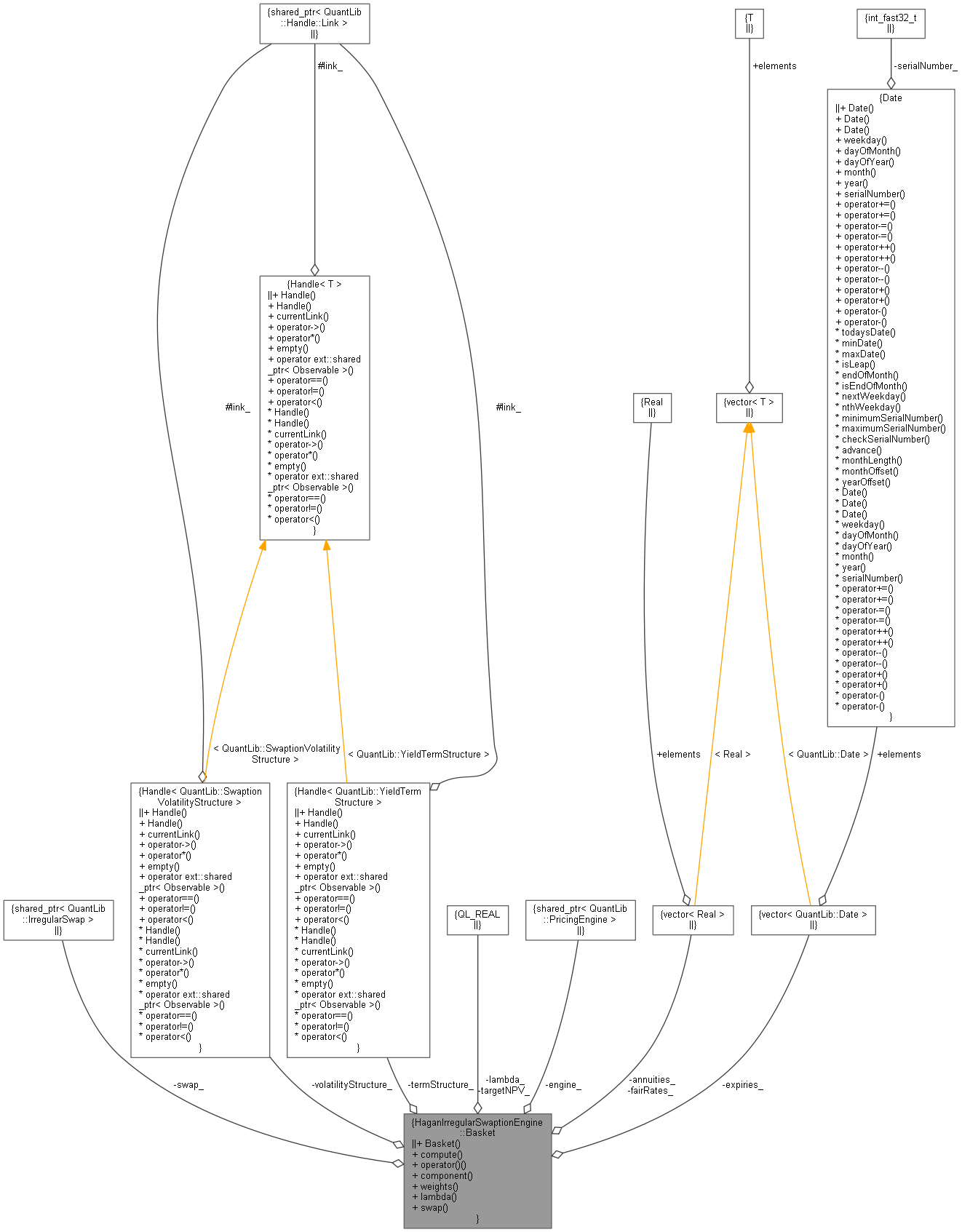

Collaboration diagram for HaganIrregularSwaptionEngine::Basket:

Collaboration diagram for HaganIrregularSwaptionEngine::Basket:

Public Member Functions | |

| Basket (ext::shared_ptr< IrregularSwap > swap, Handle< YieldTermStructure > termStructure, Handle< SwaptionVolatilityStructure > volatilityStructure) | |

| Array | compute (Rate lambda=0.0) const |

| Real | operator() (Rate x) const |

| ext::shared_ptr< VanillaSwap > | component (Size i) const |

| Array | weights () const |

| Real & | lambda () const |

| ext::shared_ptr< IrregularSwap > | swap () const |

Private Attributes | |

| ext::shared_ptr< IrregularSwap > | swap_ |

| Handle< YieldTermStructure > | termStructure_ |

| Handle< SwaptionVolatilityStructure > | volatilityStructure_ |

| Real | targetNPV_ = 0.0 |

| ext::shared_ptr< PricingEngine > | engine_ |

| std::vector< Real > | fairRates_ |

| std::vector< Real > | annuities_ |

| std::vector< Date > | expiries_ |

| Real | lambda_ = 0.0 |

Detailed Description

Definition at line 60 of file haganirregularswaptionengine.hpp.

Constructor & Destructor Documentation

◆ Basket()

| Basket | ( | ext::shared_ptr< IrregularSwap > | swap, |

| Handle< YieldTermStructure > | termStructure, | ||

| Handle< SwaptionVolatilityStructure > | volatilityStructure | ||

| ) |

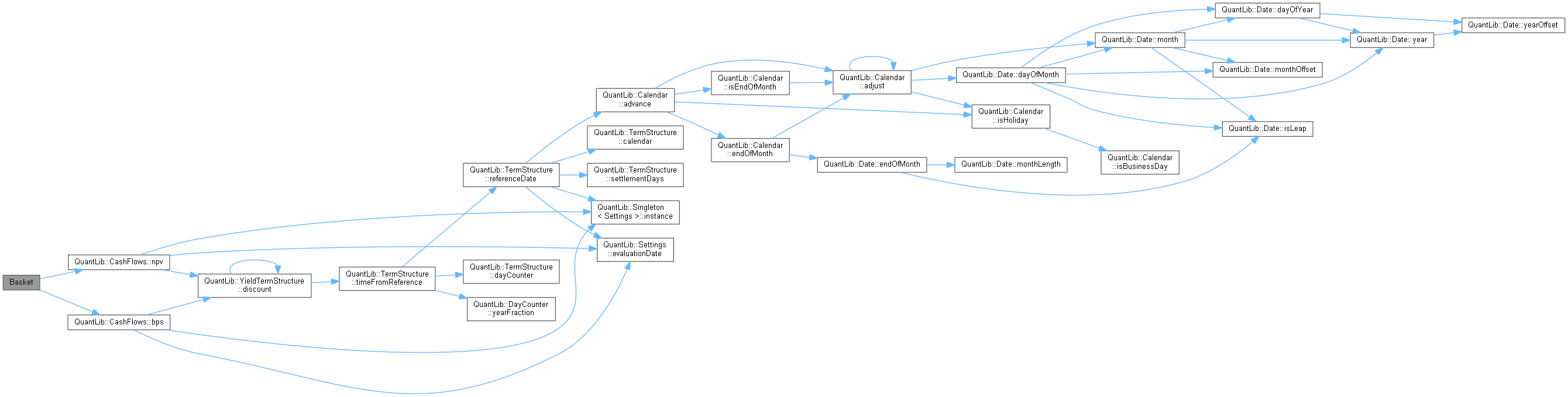

Definition at line 38 of file haganirregularswaptionengine.cpp.

Here is the call graph for this function:

Member Function Documentation

◆ compute()

Definition at line 107 of file haganirregularswaptionengine.cpp.

Here is the call graph for this function: Here is the caller graph for this function:

Here is the caller graph for this function:

◆ operator()()

Definition at line 167 of file haganirregularswaptionengine.cpp.

Here is the call graph for this function:

◆ component()

| ext::shared_ptr< VanillaSwap > component | ( | Size | i | ) | const |

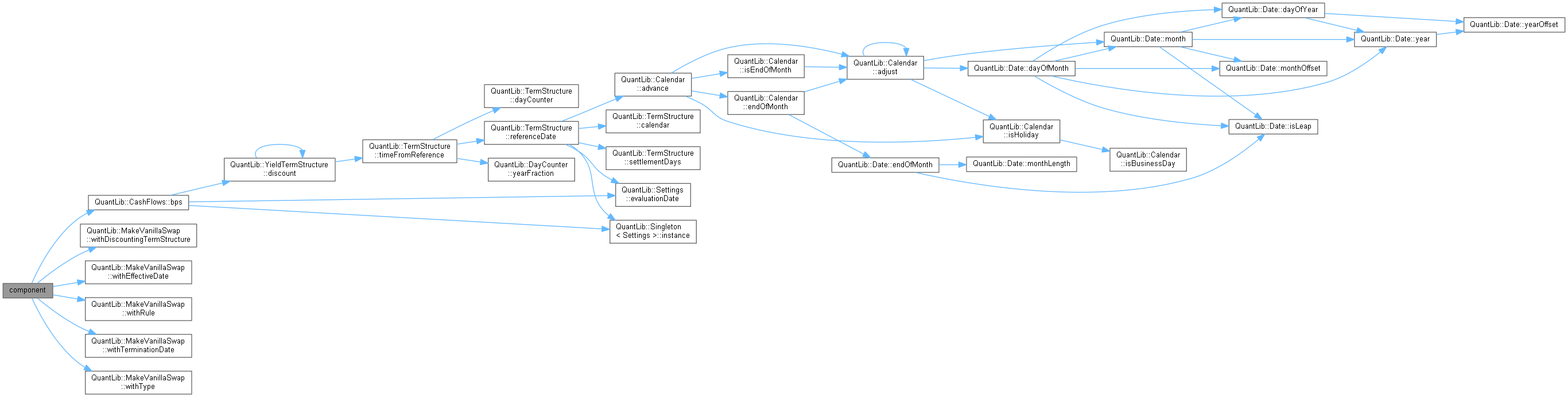

Definition at line 181 of file haganirregularswaptionengine.cpp.

Here is the call graph for this function: Here is the caller graph for this function:

Here is the caller graph for this function:

◆ weights()

| Array weights | ( | ) | const |

Definition at line 68 of file haganirregularswaptionengine.hpp.

Here is the call graph for this function: Here is the caller graph for this function:

Here is the caller graph for this function:

◆ lambda()

| Real & lambda | ( | ) | const |

Definition at line 69 of file haganirregularswaptionengine.hpp.

◆ swap()

| ext::shared_ptr< IrregularSwap > swap | ( | ) | const |

Definition at line 71 of file haganirregularswaptionengine.hpp.

Member Data Documentation

◆ swap_

|

private |

Definition at line 73 of file haganirregularswaptionengine.hpp.

◆ termStructure_

|

private |

Definition at line 74 of file haganirregularswaptionengine.hpp.

◆ volatilityStructure_

|

private |

Definition at line 75 of file haganirregularswaptionengine.hpp.

◆ targetNPV_

|

private |

Definition at line 77 of file haganirregularswaptionengine.hpp.

◆ engine_

|

private |

Definition at line 79 of file haganirregularswaptionengine.hpp.

◆ fairRates_

|

private |

Definition at line 81 of file haganirregularswaptionengine.hpp.

◆ annuities_

|

private |

Definition at line 82 of file haganirregularswaptionengine.hpp.

◆ expiries_

|

private |

Definition at line 83 of file haganirregularswaptionengine.hpp.

◆ lambda_

|

mutableprivate |

Definition at line 85 of file haganirregularswaptionengine.hpp.