Default loss distribution convolution for finite non homogeneous pool. More...

#include <inhomogeneouspooldef.hpp>

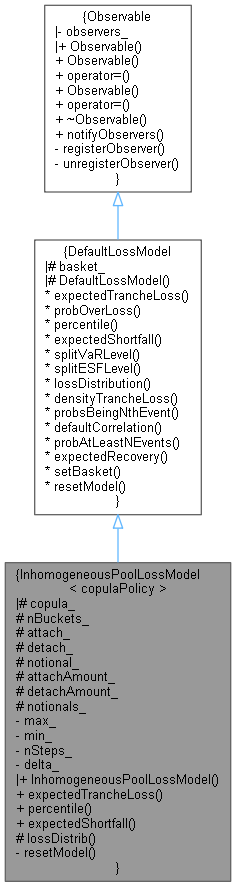

Inheritance diagram for InhomogeneousPoolLossModel< copulaPolicy >:

Inheritance diagram for InhomogeneousPoolLossModel< copulaPolicy >: Collaboration diagram for InhomogeneousPoolLossModel< copulaPolicy >:

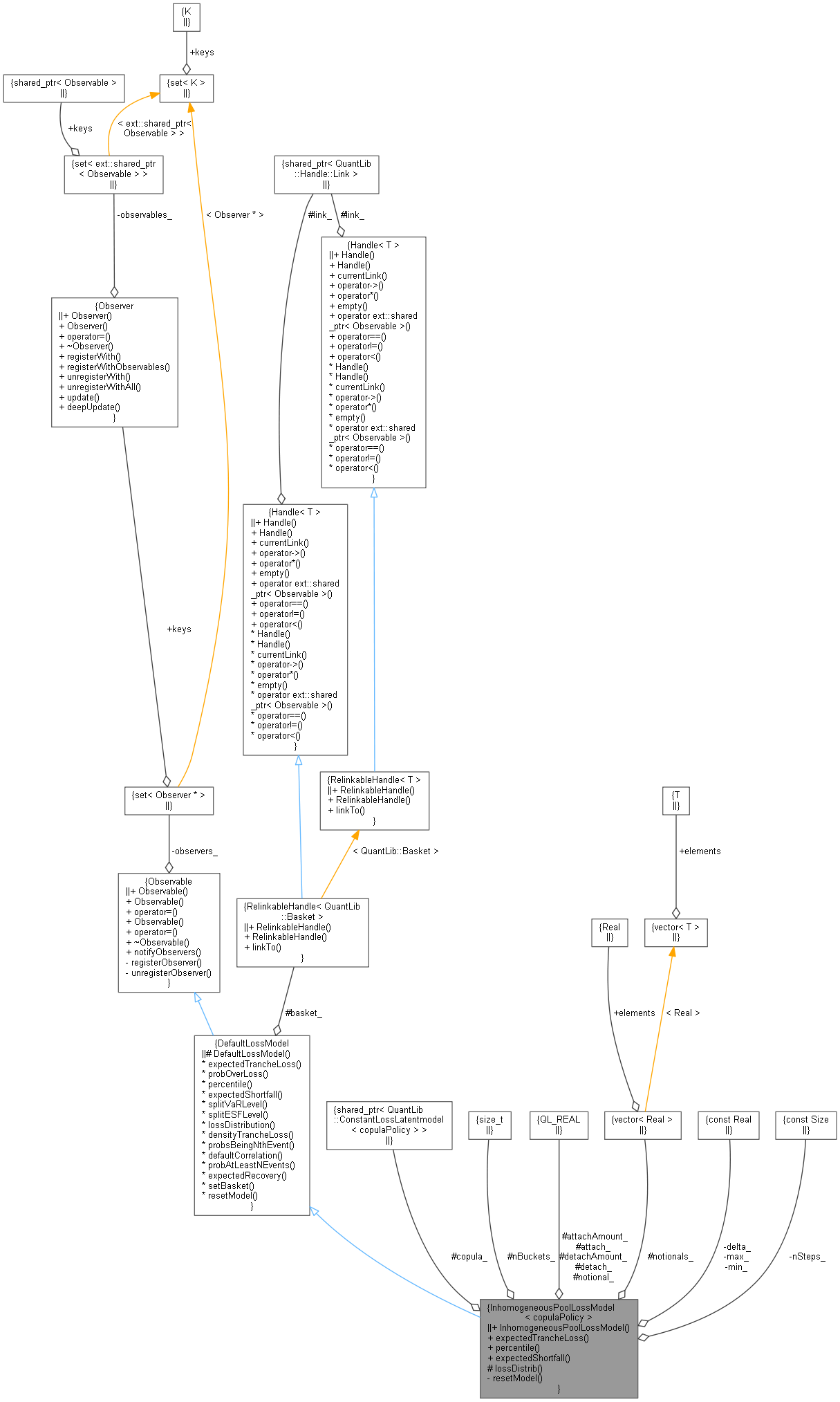

Collaboration diagram for InhomogeneousPoolLossModel< copulaPolicy >:

Public Types | |

| typedef copulaPolicy | copulaType |

Public Member Functions | |

| InhomogeneousPoolLossModel (const ext::shared_ptr< ConstantLossLatentmodel< copulaPolicy > > &copula, Size nBuckets, Real max=5., Real min=-5., Size nSteps=50) | |

| Real | expectedTrancheLoss (const Date &d) const override |

| Real | percentile (const Date &d, Real percentile) const override |

| Value at Risk given a default loss percentile. More... | |

| Real | expectedShortfall (const Date &d, Probability percentile) const override |

| Expected shortfall given a default loss percentile. More... | |

| Public Member Functions inherited from Observable | |

| Observable ()=default | |

| Observable (const Observable &) | |

| Observable & | operator= (const Observable &) |

| Observable (Observable &&)=delete | |

| Observable & | operator= (Observable &&)=delete |

| virtual | ~Observable ()=default |

| void | notifyObservers () |

Protected Member Functions | |

| Distribution | lossDistrib (const Date &d) const |

| Protected Member Functions inherited from DefaultLossModel | |

| DefaultLossModel ()=default | |

| virtual Probability | probOverLoss (const Date &d, Real lossFraction) const |

| virtual std::vector< Real > | splitVaRLevel (const Date &d, Real loss) const |

| Associated VaR fraction to each counterparty. More... | |

| virtual std::vector< Real > | splitESFLevel (const Date &d, Real loss) const |

| Associated ESF fraction to each counterparty. More... | |

| virtual std::map< Real, Probability > | lossDistribution (const Date &) const |

| Full loss distribution. More... | |

| virtual Real | densityTrancheLoss (const Date &d, Real lossFraction) const |

| Probability density of a given loss fraction of the basket notional. More... | |

| virtual std::vector< Probability > | probsBeingNthEvent (Size n, const Date &d) const |

| virtual Real | defaultCorrelation (const Date &d, Size iName, Size jName) const |

| Pearsons' default probability correlation. More... | |

| virtual Probability | probAtLeastNEvents (Size n, const Date &d) const |

| virtual Real | expectedRecovery (const Date &, Size iName, const DefaultProbKey &) const |

Protected Attributes | |

| const ext::shared_ptr< ConstantLossLatentmodel< copulaPolicy > > | copula_ |

| Size | nBuckets_ |

| Real | attach_ |

| Real | detach_ |

| Real | notional_ |

| Real | attachAmount_ |

| Real | detachAmount_ |

| std::vector< Real > | notionals_ |

| Protected Attributes inherited from DefaultLossModel | |

| RelinkableHandle< Basket > | basket_ |

Private Member Functions | |

| void | resetModel () override |

| Concrete models do now any updates/inits they need on basket reset. More... | |

Private Attributes | |

| const Real | max_ |

| const Real | min_ |

| const Size | nSteps_ |

| const Real | delta_ |

Detailed Description

class QuantLib::InhomogeneousPoolLossModel< copulaPolicy >

Default loss distribution convolution for finite non homogeneous pool.

Definition at line 46 of file inhomogeneouspooldef.hpp.

Member Typedef Documentation

◆ copulaType

| typedef copulaPolicy copulaType |

Definition at line 52 of file inhomogeneouspooldef.hpp.

Constructor & Destructor Documentation

◆ InhomogeneousPoolLossModel()

| InhomogeneousPoolLossModel | ( | const ext::shared_ptr< ConstantLossLatentmodel< copulaPolicy > > & | copula, |

| Size | nBuckets, | ||

| Real | max = 5., |

||

| Real | min = -5., |

||

| Size | nSteps = 50 |

||

| ) |

Definition at line 54 of file inhomogeneouspooldef.hpp.

Member Function Documentation

◆ resetModel()

|

overrideprivatevirtual |

Concrete models do now any updates/inits they need on basket reset.

Implements DefaultLossModel.

Definition at line 114 of file inhomogeneouspooldef.hpp.

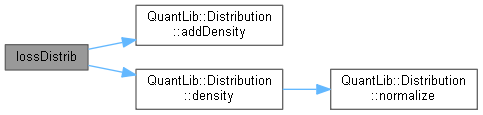

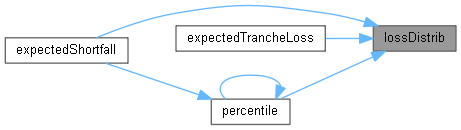

◆ lossDistrib()

|

protected |

Definition at line 131 of file inhomogeneouspooldef.hpp.

Here is the call graph for this function: Here is the caller graph for this function:

Here is the caller graph for this function:

◆ expectedTrancheLoss()

Reimplemented from DefaultLossModel.

Definition at line 73 of file inhomogeneouspooldef.hpp.

Here is the call graph for this function:

◆ percentile()

Value at Risk given a default loss percentile.

Reimplemented from DefaultLossModel.

Definition at line 82 of file inhomogeneouspooldef.hpp.

Here is the call graph for this function: Here is the caller graph for this function:

Here is the caller graph for this function:

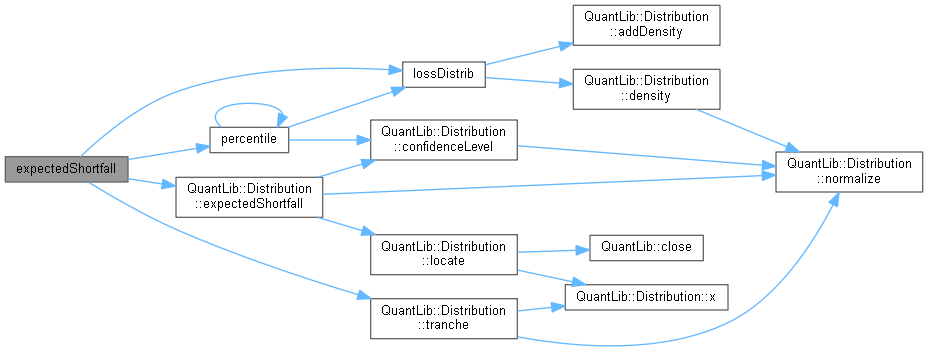

◆ expectedShortfall()

|

overridevirtual |

Expected shortfall given a default loss percentile.

Reimplemented from DefaultLossModel.

Definition at line 86 of file inhomogeneouspooldef.hpp.

Here is the call graph for this function:

Member Data Documentation

◆ copula_

|

protected |

Definition at line 93 of file inhomogeneouspooldef.hpp.

◆ nBuckets_

|

protected |

Definition at line 94 of file inhomogeneouspooldef.hpp.

◆ attach_

|

mutableprotected |

Definition at line 95 of file inhomogeneouspooldef.hpp.

◆ detach_

|

protected |

Definition at line 95 of file inhomogeneouspooldef.hpp.

◆ notional_

|

protected |

Definition at line 95 of file inhomogeneouspooldef.hpp.

◆ attachAmount_

|

protected |

Definition at line 95 of file inhomogeneouspooldef.hpp.

◆ detachAmount_

|

protected |

Definition at line 95 of file inhomogeneouspooldef.hpp.

◆ notionals_

|

mutableprotected |

Definition at line 96 of file inhomogeneouspooldef.hpp.

◆ max_

|

private |

Definition at line 101 of file inhomogeneouspooldef.hpp.

◆ min_

|

private |

Definition at line 102 of file inhomogeneouspooldef.hpp.

◆ nSteps_

|

private |

Definition at line 103 of file inhomogeneouspooldef.hpp.

◆ delta_

|

private |

Definition at line 104 of file inhomogeneouspooldef.hpp.