|

| | ConstantLossLatentmodel (const std::vector< std::vector< Real > > &factorWeights, const std::vector< Real > &recoveries, LatentModelIntegrationType::LatentModelIntegrationType integralType, const initTraits &ini=initTraits()) |

| |

| | ConstantLossLatentmodel (const Handle< Quote > &mktCorrel, const std::vector< Real > &recoveries, LatentModelIntegrationType::LatentModelIntegrationType integralType, Size nVariables, const initTraits &ini=initTraits()) |

| |

| Real | conditionalRecovery (const Date &d, Size iName, const std::vector< Real > &mktFactors) const |

| |

| Real | conditionalRecovery (Probability uncondDefP, Size iName, const std::vector< Real > &mktFactors) const |

| |

| Real | conditionalRecoveryInvP (Real invUncondDefP, Size iName, const std::vector< Real > &mktFactors) const |

| |

| Real | conditionalRecovery (Real latentVarSample, Size iName, const Date &d) const |

| |

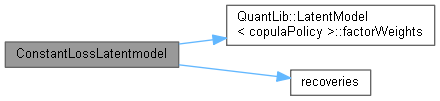

| const std::vector< Real > & | recoveries () const |

| |

| Real | expectedRecovery (const Date &d, Size iName, const DefaultProbKey &defKeys) const |

| |

| | DefaultLatentModel (const std::vector< std::vector< Real > > &factorWeights, LatentModelIntegrationType::LatentModelIntegrationType integralType, const initTraits &ini=initTraits()) |

| |

| | DefaultLatentModel (const Handle< Quote > &mktCorrel, Size nVariables, LatentModelIntegrationType::LatentModelIntegrationType integralType, const initTraits &ini=initTraits()) |

| |

| void | resetBasket (const ext::shared_ptr< Basket > &basket) const |

| |

| Probability | conditionalDefaultProbability (Probability prob, Size iName, const std::vector< Real > &mktFactors) const |

| |

| Probability | conditionalDefaultProbabilityInvP (Real invCumYProb, Size iName, const std::vector< Real > &m) const |

| |

| Probability | probOfDefault (Size iName, const Date &d) const |

| |

| Real | defaultCorrelation (const Date &d, Size iNamei, Size iNamej) const |

| |

| Probability | probAtLeastNEvents (Size n, const Date &date) const |

| |

| void | update () override |

| |

| Size | size () const |

| |

| Size | numFactors () const |

| | Number of systemic factors. More...

|

| |

| Size | numTotalFactors () const |

| | Number of total free random factors; systemic and idiosyncratic. More...

|

| |

| | LatentModel (const std::vector< std::vector< Real > > &factorsWeights, const typename copulaType::initTraits &ini=typename copulaType::initTraits()) |

| |

| | LatentModel (const std::vector< Real > &factorsWeight, const typename copulaType::initTraits &ini=typename copulaType::initTraits()) |

| |

| | LatentModel (Real correlSqr, Size nVariables, const typename copulaType::initTraits &ini=typename copulaType::initTraits()) |

| |

| | LatentModel (const Handle< Quote > &singleFactorCorrel, Size nVariables, const typename copulaType::initTraits &ini=typename copulaType::initTraits()) |

| |

| const std::vector< std::vector< Real > > & | factorWeights () const |

| | Provides values of the factors \( a_{i,k} \). More...

|

| |

| const std::vector< Real > & | idiosyncFctrs () const |

| | Provides values of the normalized idiosyncratic factors \( Z_i \). More...

|

| |

| Real | latentVariableCorrel (Size iVar1, Size iVar2) const |

| | Latent variable correlations: More...

|

| |

| Probability | cumulativeY (Real val, Size iVariable) const |

| |

| Probability | cumulativeZ (Real z) const |

| | Cumulative distribution of Z, the idiosyncratic/error factors. More...

|

| |

| Probability | density (const std::vector< Real > &m) const |

| | Density function of M, the market/systemic factors. More...

|

| |

| Real | inverseCumulativeDensity (Probability p, Size iFactor) const |

| | Inverse cumulative distribution of the systemic factor iFactor. More...

|

| |

| Real | inverseCumulativeY (Probability p, Size iVariable) const |

| |

| Real | inverseCumulativeZ (Probability p) const |

| |

| std::vector< Real > | allFactorCumulInverter (const std::vector< Real > &probs) const |

| |

| Real | latentVarValue (const std::vector< Real > &allFactors, Size iVar) const |

| |

| const copulaType & | copula () const |

| |

| Real | integratedExpectedValue (const std::function< Real(const std::vector< Real > &v1)> &f) const |

| |

| std::vector< Real > | integratedExpectedValueV (const std::function< std::vector< Real >(const std::vector< Real > &v1)> &f) const |

| |

| | Observer ()=default |

| |

| | Observer (const Observer &) |

| |

| Observer & | operator= (const Observer &) |

| |

| virtual | ~Observer () |

| |

| std::pair< iterator, bool > | registerWith (const ext::shared_ptr< Observable > &) |

| |

| void | registerWithObservables (const ext::shared_ptr< Observer > &) |

| |

| Size | unregisterWith (const ext::shared_ptr< Observable > &) |

| |

| void | unregisterWithAll () |

| |

| virtual void | update ()=0 |

| |

| virtual void | deepUpdate () |

| |

| | Observable ()=default |

| |

| | Observable (const Observable &) |

| |

| Observable & | operator= (const Observable &) |

| |

| | Observable (Observable &&)=delete |

| |

| Observable & | operator= (Observable &&)=delete |

| |

| virtual | ~Observable ()=default |

| |

| void | notifyObservers () |

| |

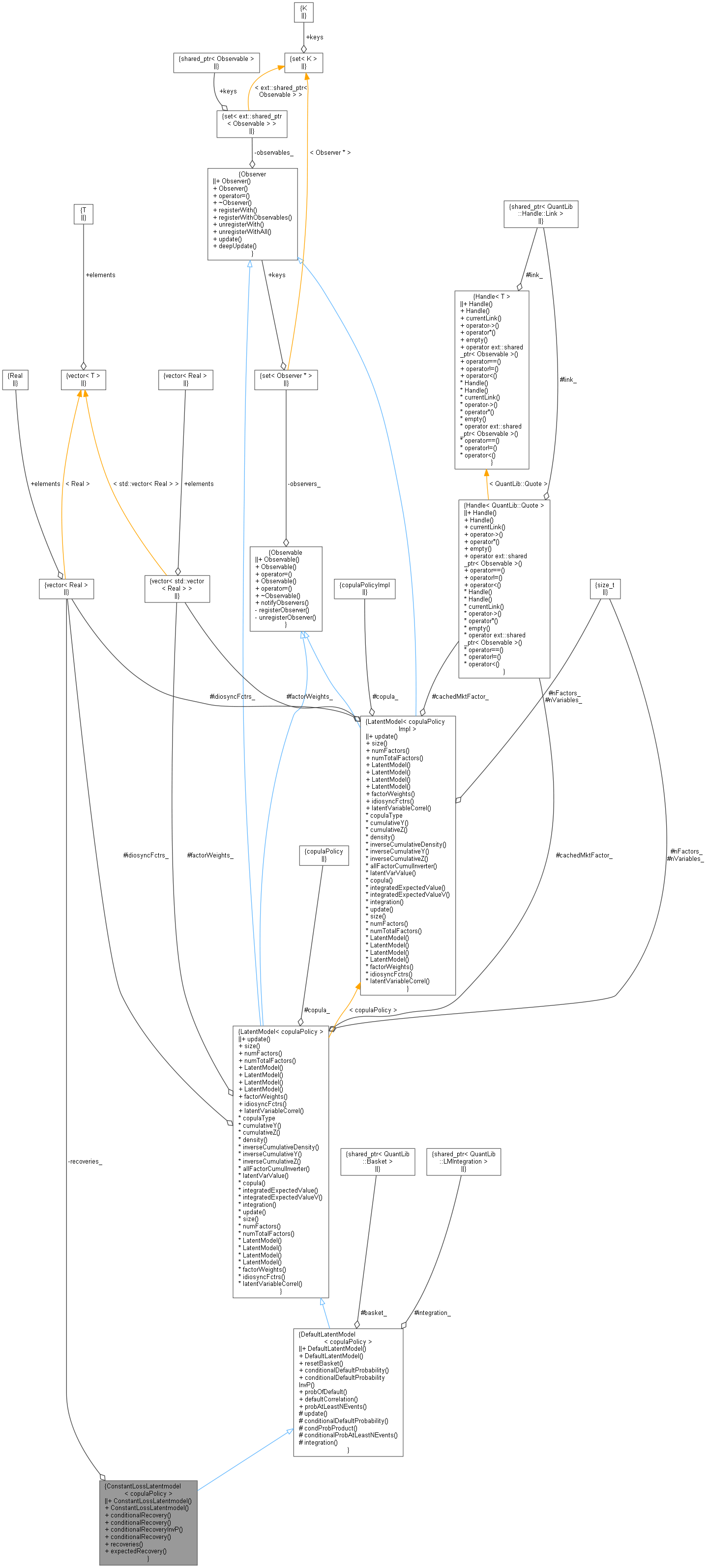

template<class

copulaPolicy>

class QuantLib::ConstantLossLatentmodel< copulaPolicy >

Constant deterministic loss amount default latent model. Integrable implementation.

Definition at line 38 of file constantlosslatentmodel.hpp.

Inheritance diagram for ConstantLossLatentmodel< copulaPolicy >:

Inheritance diagram for ConstantLossLatentmodel< copulaPolicy >: