|

| | InterpolatedZeroCurve (const std::vector< Date > &dates, const std::vector< Rate > &yields, const DayCounter &dayCounter, const Calendar &calendar=Calendar(), const std::vector< Handle< Quote > > &jumps={}, const std::vector< Date > &jumpDates={}, const Interpolator &interpolator={}, Compounding compounding=Continuous, Frequency frequency=Annual) |

| |

| | InterpolatedZeroCurve (const std::vector< Date > &dates, const std::vector< Rate > &yields, const DayCounter &dayCounter, const Calendar &calendar, const Interpolator &interpolator, Compounding compounding=Continuous, Frequency frequency=Annual) |

| |

| | InterpolatedZeroCurve (const std::vector< Date > &dates, const std::vector< Rate > &yields, const DayCounter &dayCounter, const Interpolator &interpolator, Compounding compounding=Continuous, Frequency frequency=Annual) |

| |

|

| Date | maxDate () const override |

| | the latest date for which the curve can return values More...

|

| |

| | ZeroYieldStructure (const DayCounter &dc=DayCounter()) |

| |

| | ZeroYieldStructure (const Date &referenceDate, const Calendar &calendar=Calendar(), const DayCounter &dc=DayCounter(), const std::vector< Handle< Quote > > &jumps={}, const std::vector< Date > &jumpDates={}) |

| |

| | ZeroYieldStructure (Natural settlementDays, const Calendar &calendar, const DayCounter &dc=DayCounter(), const std::vector< Handle< Quote > > &jumps={}, const std::vector< Date > &jumpDates={}) |

| |

| | YieldTermStructure (const DayCounter &dc=DayCounter()) |

| |

| | YieldTermStructure (const Date &referenceDate, const Calendar &cal=Calendar(), const DayCounter &dc=DayCounter(), std::vector< Handle< Quote > > jumps={}, const std::vector< Date > &jumpDates={}) |

| |

| | YieldTermStructure (Natural settlementDays, const Calendar &cal, const DayCounter &dc=DayCounter(), std::vector< Handle< Quote > > jumps={}, const std::vector< Date > &jumpDates={}) |

| |

| DiscountFactor | discount (const Date &d, bool extrapolate=false) const |

| |

| DiscountFactor | discount (Time t, bool extrapolate=false) const |

| |

| InterestRate | zeroRate (const Date &d, const DayCounter &resultDayCounter, Compounding comp, Frequency freq=Annual, bool extrapolate=false) const |

| |

| InterestRate | zeroRate (Time t, Compounding comp, Frequency freq=Annual, bool extrapolate=false) const |

| |

| InterestRate | forwardRate (const Date &d1, const Date &d2, const DayCounter &resultDayCounter, Compounding comp, Frequency freq=Annual, bool extrapolate=false) const |

| |

| InterestRate | forwardRate (const Date &d, const Period &p, const DayCounter &resultDayCounter, Compounding comp, Frequency freq=Annual, bool extrapolate=false) const |

| |

| InterestRate | forwardRate (Time t1, Time t2, Compounding comp, Frequency freq=Annual, bool extrapolate=false) const |

| |

| const std::vector< Date > & | jumpDates () const |

| |

| const std::vector< Time > & | jumpTimes () const |

| |

| void | update () override |

| |

| | TermStructure (DayCounter dc=DayCounter()) |

| | default constructor More...

|

| |

| | TermStructure (const Date &referenceDate, Calendar calendar=Calendar(), DayCounter dc=DayCounter()) |

| | initialize with a fixed reference date More...

|

| |

| | TermStructure (Natural settlementDays, Calendar, DayCounter dc=DayCounter()) |

| | calculate the reference date based on the global evaluation date More...

|

| |

| | ~TermStructure () override=default |

| |

| virtual DayCounter | dayCounter () const |

| | the day counter used for date/time conversion More...

|

| |

| Time | timeFromReference (const Date &date) const |

| | date/time conversion More...

|

| |

| virtual Time | maxTime () const |

| | the latest time for which the curve can return values More...

|

| |

| virtual const Date & | referenceDate () const |

| | the date at which discount = 1.0 and/or variance = 0.0 More...

|

| |

| virtual Calendar | calendar () const |

| | the calendar used for reference and/or option date calculation More...

|

| |

| virtual Natural | settlementDays () const |

| | the settlementDays used for reference date calculation More...

|

| |

| | Observer ()=default |

| |

| | Observer (const Observer &) |

| |

| Observer & | operator= (const Observer &) |

| |

| virtual | ~Observer () |

| |

| std::pair< iterator, bool > | registerWith (const ext::shared_ptr< Observable > &) |

| |

| void | registerWithObservables (const ext::shared_ptr< Observer > &) |

| |

| Size | unregisterWith (const ext::shared_ptr< Observable > &) |

| |

| void | unregisterWithAll () |

| |

| virtual void | update ()=0 |

| |

| virtual void | deepUpdate () |

| |

| | Observable ()=default |

| |

| | Observable (const Observable &) |

| |

| Observable & | operator= (const Observable &) |

| |

| | Observable (Observable &&)=delete |

| |

| Observable & | operator= (Observable &&)=delete |

| |

| virtual | ~Observable ()=default |

| |

| void | notifyObservers () |

| |

|

| const std::vector< Time > & | times () const |

| |

| const std::vector< Date > & | dates () const |

| |

| const std::vector< Real > & | data () const |

| |

| const std::vector< Rate > & | zeroRates () const |

| |

| std::vector< std::pair< Date, Real > > | nodes () const |

| |

| | InterpolatedZeroCurve (const DayCounter &, const Interpolator &interpolator={}) |

| |

| | InterpolatedZeroCurve (const Date &referenceDate, const DayCounter &, const std::vector< Handle< Quote > > &jumps={}, const std::vector< Date > &jumpDates={}, const Interpolator &interpolator={}) |

| |

| | InterpolatedZeroCurve (Natural settlementDays, const Calendar &, const DayCounter &, const std::vector< Handle< Quote > > &jumps={}, const std::vector< Date > &jumpDates={}, const Interpolator &interpolator={}) |

| |

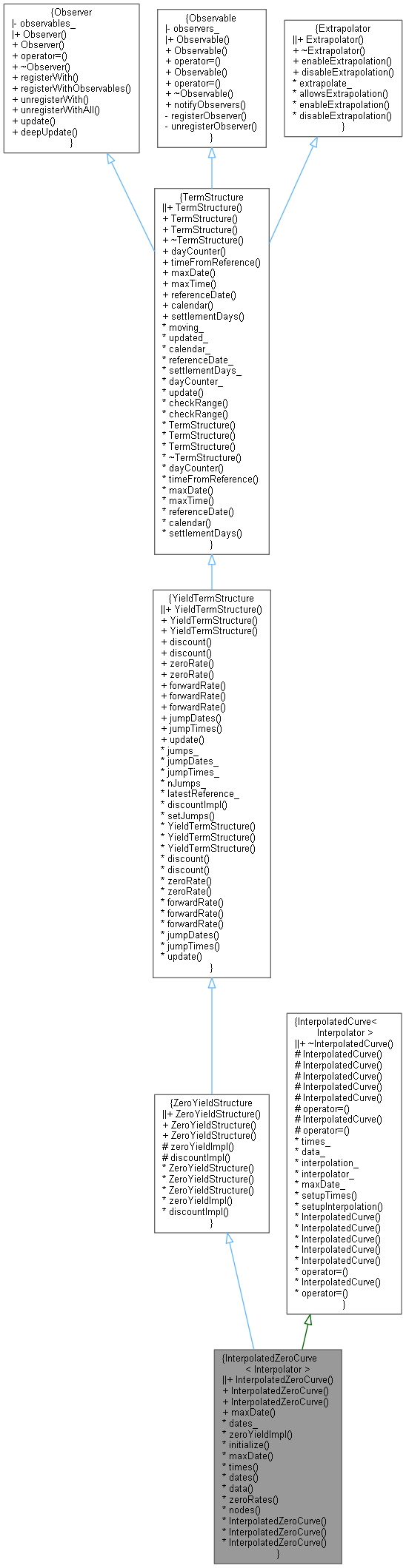

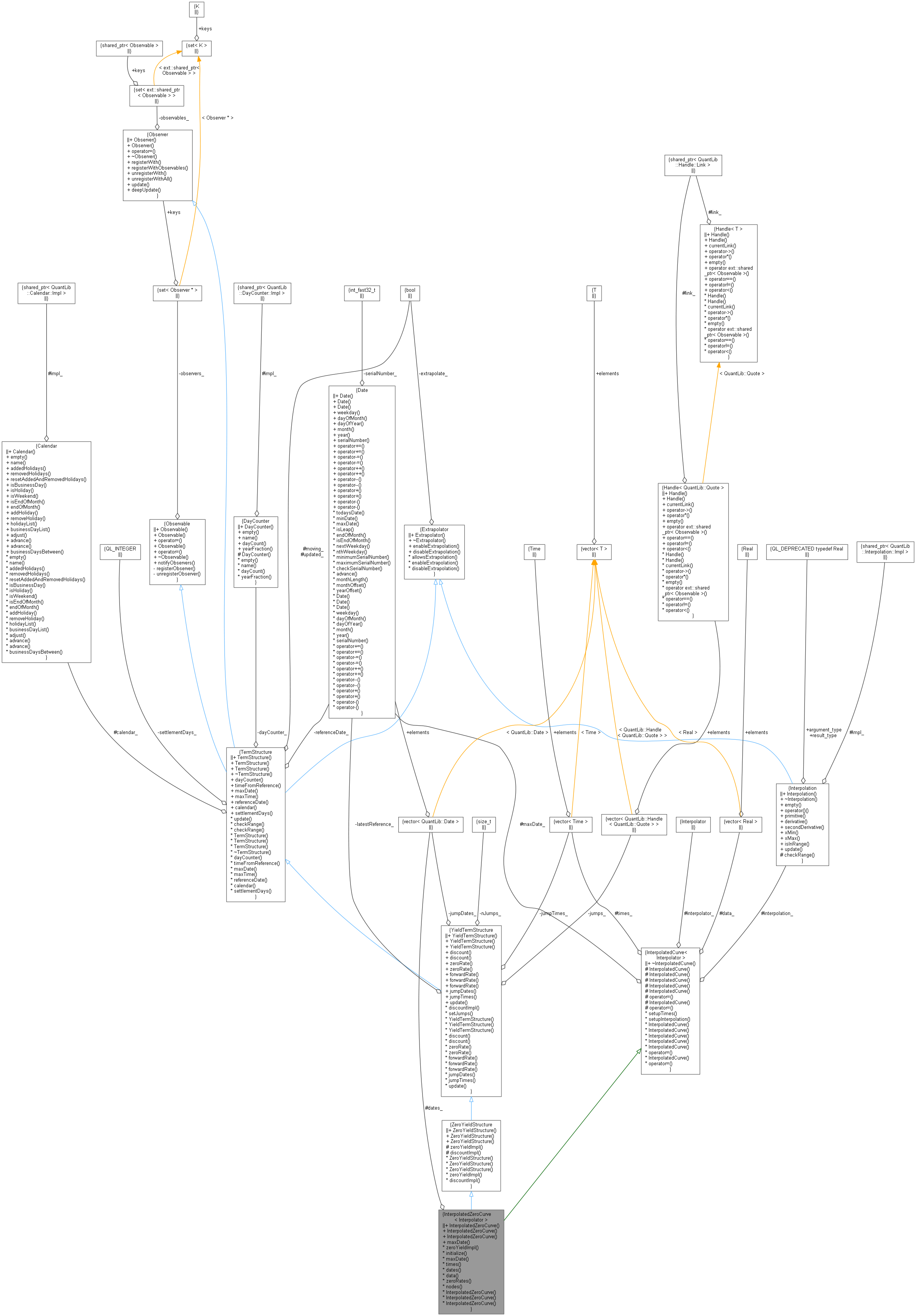

template<class Interpolator>

class QuantLib::InterpolatedZeroCurve< Interpolator >

YieldTermStructure based on interpolation of zero rates.

Definition at line 42 of file zerocurve.hpp.

Inheritance diagram for InterpolatedZeroCurve< Interpolator >:

Inheritance diagram for InterpolatedZeroCurve< Interpolator >: