#include <quantocouponpricer.hpp>

Inheritance diagram for BlackIborQuantoCouponPricer:

Inheritance diagram for BlackIborQuantoCouponPricer: Collaboration diagram for BlackIborQuantoCouponPricer:

Collaboration diagram for BlackIborQuantoCouponPricer:

Protected Member Functions | |

| Rate | adjustedFixing (Rate fixing=Null< Rate >()) const override |

| Protected Member Functions inherited from BlackIborCouponPricer | |

| Real | optionletPrice (Option::Type optionType, Real effStrike) const |

| Real | optionletRate (Option::Type optionType, Real effStrike) const |

| virtual Rate | adjustedFixing (Rate fixing=Null< Rate >()) const |

Private Attributes | |

| Handle< BlackVolTermStructure > | fxRateBlackVolatility_ |

| Handle< Quote > | underlyingFxCorrelation_ |

Additional Inherited Members | |

| Public Types inherited from BlackIborCouponPricer | |

| enum | TimingAdjustment { Black76 , BivariateLognormal } |

| Public Types inherited from Observer | |

| typedef set_type::iterator | iterator |

| Protected Attributes inherited from BlackIborCouponPricer | |

| Real | discount_ |

| Protected Attributes inherited from IborCouponPricer | |

| const IborCoupon * | coupon_ |

| ext::shared_ptr< IborIndex > | index_ |

| Date | fixingDate_ |

| Real | gearing_ |

| Spread | spread_ |

| Time | accrualPeriod_ |

| Date | fixingValueDate_ |

| Date | fixingEndDate_ |

| Date | fixingMaturityDate_ |

| Time | spanningTime_ |

| Time | spanningTimeIndexMaturity_ |

| Handle< OptionletVolatilityStructure > | capletVol_ |

| bool | useIndexedCoupon_ |

Detailed Description

Definition at line 34 of file quantocouponpricer.hpp.

Constructor & Destructor Documentation

◆ BlackIborQuantoCouponPricer()

| BlackIborQuantoCouponPricer | ( | Handle< BlackVolTermStructure > | fxRateBlackVolatility, |

| Handle< Quote > | underlyingFxCorrelation, | ||

| const Handle< OptionletVolatilityStructure > & | capletVolatility | ||

| ) |

Member Function Documentation

◆ adjustedFixing()

Reimplemented from BlackIborCouponPricer.

Definition at line 31 of file quantocouponpricer.cpp.

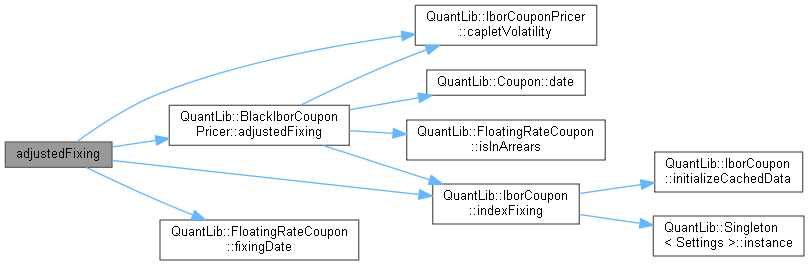

Here is the call graph for this function:

Member Data Documentation

◆ fxRateBlackVolatility_

|

private |

Definition at line 50 of file quantocouponpricer.hpp.

◆ underlyingFxCorrelation_

Definition at line 51 of file quantocouponpricer.hpp.